Dollar Thrifty Reports Record Quarterly Net Income

The company noted that its GAAP and non-GAAP earnings as well as its corporate adjusted EBITDA for the third quarter of 2010 were negatively impacted by $11.9 million of merger-related expenses, while the third quarter of 2011 was not impacted by such expenses.

Dollar Thrifty Automotive Group Inc. (DTG) reported results on Nov. 1 for the third quarter that ended Sept. 30. Net income for the 2011 third quarter was $66.6 million, or $2.13 per diluted share, compared to a net income of $49.2 million, or $1.62 per diluted share, for the third quarter of 2010.

Net income for the third quarter of 2011 included a charge of $0.01 per diluted share related to a decrease in fair value of derivatives, compared to income of $0.13 per diluted share for the third quarter of 2010 related to an increase in fair value of derivatives.

Non-GAAP net income for the 2011 third quarter was $66.9 million, or $2.14 per diluted share, compared to non-GAAP net income of $45.8 million, or $1.51 per diluted share, for the 2010 third quarter. Non-GAAP net income excludes the (increase) decrease in fair value of derivatives and the non-cash charges related to the impairment of long-lived assets, net of related tax impact.

DTG reported corporate adjusted EBITDA for the third quarter of 2011 of $117.6 million, compared to $81.8 million in the third quarter of 2010.

The company noted that its GAAP and non-GAAP earnings as well as its corporate adjusted EBITDA for the third quarter of 2010 were negatively impacted by $11.9 million of merger-related expenses, while the third quarter of 2011 was not impacted by such expenses.

"We are pleased that the company is reporting the highest quarterly profit in its history,” said Scott L. Thompson, DTG president and CEO. “We remain keenly focused on profitable revenue growth, productivity initiatives, cost control and disciplined fleet management."

For this third quarter, DTG’s total revenue was $451.7 million, as compared to $443.5 million for the comparable 2010 period. Vehicle rental revenue for the quarter was up 2.4 percent, driven by a 4.1 percent increase in rental days, partially offset by a 1.7 percent decrease in revenue per day.

The average fleet for the quarter was up 4.3 percent compared to the prior year period. Vehicle utilization in the third quarter of 2011 was 83.9 percent, compared to 84.0 percent in the third quarter of 2010.

Fleet cost per vehicle was $186 per month in the third quarter of 2011, compared to $262 per month in the third quarter of 2010. The company's base depreciation rate continued to benefit from the overall strength of the used vehicle market and the resulting favorable impact on residual values.

DTG noted that gains on sales of risk vehicles, a component of vehicle depreciation, totaled $17.4 million in the third quarter of 2011, up from $10.0 million in the third quarter of 2010. The average gain per vehicle sold during the third quarter of 2011 was $1,125 per unit, compared to $632 per unit in the third quarter of 2010.

Direct vehicle and operating expenses and selling, general and administrative expenses totaled $262.4 million in the third quarter of 2011, compared to $263.6 million in the third quarter of 2010. The decrease in operating expenses primarily resulted from a reduction in merger-related expenses of $11.9 million, partially offset by an increase in direct costs attributable to the overall increase in fleet size and increased ancillary revenues.

Excluding merger-related expenses, operating expenses totaled 58.1 percent of revenues for the third quarter of 2011, compared to 56.7 percent of revenues for the third quarter of 2010.

DTG noted that although the operating expense percentage increased, the increase was attributable to direct costs associated with increased sales penetration of certain ancillary products, such as pre-paid fuel and toll road products. The company noted that the increased expense associated with incremental ancillary sales was more than fully recovered through rental revenues.

"We are pleased with the rental day growth achieved this quarter and the strength of our forward bookings,” Thompson said. “Although the pricing environment was a headwind this quarter, we continue to benefit from a favorable used vehicle market and our efficient, low-cost operating structure.”[PAGEBREAK]

Nine-Month Results

For the nine months ended Sept. 30, net income was $125.6 million, or $4.03 per diluted share, compared to net income of $118.7 million, or $3.93 per diluted share for the comparable period in 2010. Net income for the nine months included income of $0.06 per diluted share, compared to income of $0.41 per diluted share for the nine months in 2010.

Non-GAAP net income for the nine months was $123.7 million, or $3.96 per diluted share, compared to non-GAAP net income of $106.8 million, or $3.53 per diluted share, for the same period in 2010. Non-GAAP net income excludes the (increase) decrease in fair value of derivatives and the non-cash charges related to the impairment of long-lived assets, net of related tax impact.

DTG noted that both its GAAP and non-GAAP earnings for the nine months in 2011 and 2010 were negatively impacted by merger-related expenses of $4.6 million and $20.5 million, respectively. Additionally, the Company noted that gains on risk vehicle sales totaled $43.1 million for the nine months, down from $63.2 in the same period for 2010, primarily due to approximately 18,500 fewer vehicles sold in 2011 compared to 2010.

The company reported corporate adjusted EBITDA for the nine months at $235.1 million, compared to $205.5 million for the nine months in 2010.

Liquidity and Capital Resources

As of Sept. 30, DTG had $499 million in cash and cash equivalents, and an additional $201 million in restricted cash and investments primarily available for the purchase of vehicles and/or repayment of vehicle financing obligations.

During the second quarter of 2011, the company fully repaid and terminated its Canadian fleet financing facility. Additionally, during the third quarter, the company repaid all of its outstanding corporate debt totaling $143 million. These actions are expected to reduce DTG’s interest expense by approximately $9 million annually.

As previously announced, the company has completed three fleet financing facilities since July of this year, including the issuance of $500 million of Series 2011-1 medium-term notes, the renewal of its Series 2010-3 variable funding notes in an aggregate principal amount of $600 million, and the issuance of $400 million of Series 2011-2 medium-term notes.

DTG noted that it has now effectively pre-funded all its upcoming debt maturities for 2012, and has significantly extended its fleet financing maturity profile into 2013 and beyond. The cost of funds on the new series of notes is lower than the majority of the company's fleet financing sources that the new notes will replace, which will be favorable for future years' interest expense.

Additionally, the advance rates on the notes increased to 69 percent, compared to 65 percent on the company's variable funding notes issued in 2010, thereby lowering the overall amount of collateral enhancement required to be provided by DTG.

As of Sept. 30, the company's tangible net worth was $647 million and the company had no corporate debt.

Share Repurchase Program Initiated – Click here for more details about this plan that was announced when DTG took itself out of the merger solicitation process on Oct. 11.

2011 Outlook - Fourth Quarter Update

DTG noted it expects 1 to 2 percent rental revenue growth in the fourth quarter with growth in days offsetting a slight decline in revenue per day. The company further noted that its fleet cost outlook for the full year of 2011 of $215 - $225 per vehicle per month remains unchanged.

Based on the factors outlined above, the Company is currently targeting corporate adjusted EBITDA for the full year of 2011 to be within a range of $270 million to $290 million. This estimate excludes the impact of merger-related expenses incurred to date and that may be incurred during the remainder of 2011.

More Rental Operations

Car Rental Rates Forecast to Rise 3.6% in 2026 Before Easing in 2027

Car rental rates are projected to rise less than airfares and hotel rates in 2026, then become the only major travel category forecast to decline in 2027, according to projections from GBTA and ALTOUR.

Read More →

Avis Cuts Fleet as Summer Demand Trails Expectations

Avis Budget Group increased second-quarter earnings despite lower Americas revenue and softer-than-expected summer demand. The company also expanded Avis First and advanced its autonomous fleet operations with Waymo.

Read More →

Why Bookings Are Only the Start of the Rental Day

A reservation captures demand. The operating test is whether the business can keep the customer, vehicle, commercial terms, and next action aligned until the rental is closed.

Read More →

This Is the Oldest Car Rental Advertisement You’ll Ever See

This ad for Saunders Drive it Yourself, believed to be the first car rental company in the U.S., was found in an Omaha phone book from 1926.

Read More →

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

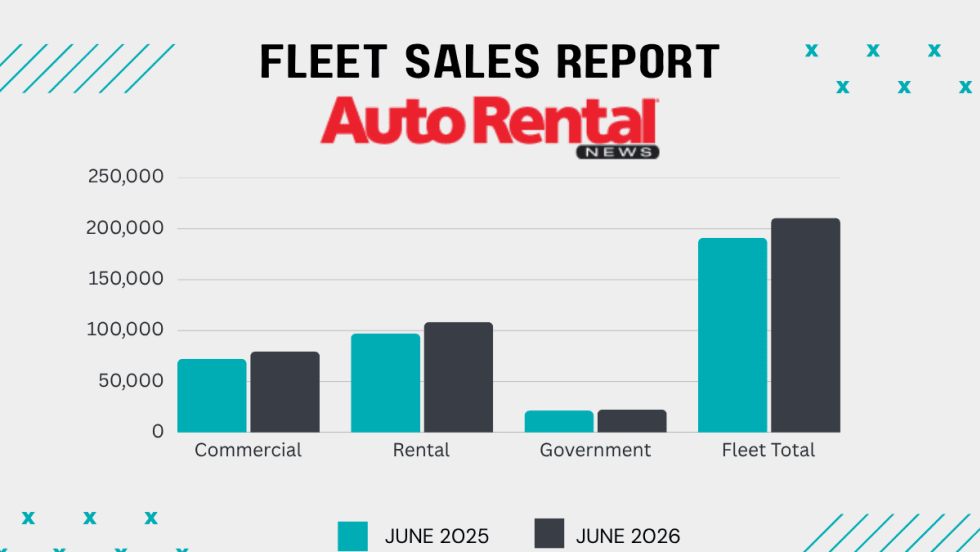

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →