How to Be Your Bank’s Best Customer

Banks want more assurances than ever that your business is healthy. Having an answer to these 10 questions will help keep your credit lines safe.

Who are your best customers? Are they the people who do business with you on a regular basis? Do they have their paperwork up to date and pay on time, or early? Are they easy to deal with and always polite to you and your counter people?

Just like you, your bank is a business. And just like you, it wants to support its best customers. Nowadays, a good relationship with your bank is one of the most important factors promoting the health of your rental business.

So, “Are you one of your bank’s best customers?” If you have a hard time answering that question, then you have some other questions to answer.

Do you have up-to-date financials? With the easy availability of off-the-shelf accounting programs such as QuickBooks, Peachtree, MAS90, Great Plains or Sage, company financial reports are available at the click of a button. Both Bluebird and TSD provide easy-to-use interfaces to these and other standard accounting programs.

(Angelia Margolit of Bluebird says that once you balance your daily business report or DBR, Bluebird’s software automatically creates journal entries for your chart of accounts, providing you have accounting software that can accept external data.)

In this day and age, if your bank or finance company calls and asks for a copy of last quarter’s financial reports and you tell them it will take a couple of weeks, you’ve raised a red flag. With the right software you have no excuses— you can be current everyday.

Underwriters also look at credit scores, so make sure your Dunn & Bradstreet ratings and FICO score are up to date. Also, make sure you have letters in your credit file to explain any past discrepancies.

Do you know what you want from your bank? Do you have a plan?

Has a corporate customer ever said he wanted 50 cars by Friday? It would have been easier if he gave this request three months ago. Your bank is no different. You need to put together a fleet plan for the next 12–24 months.

Remember it is just a plan; it is not etched in stone. However, it should show your bank at what point you’ll need to add cars to the fleet and when you plan to sell or send them back. Can you show your bank how you’d handle a 20 percent decrease in sales? Be prepared.

A simple spreadsheet with a list of vehicle types on one axis and the 12 months of the year on another will help you approximate your funding needs.

Every so often, manufacturers will offer a special discounted price on fleet units for a short time period. Make sure your credit line has enough flexibility to take advantage of these opportunity buys.

What else do you want from your bank? Do you want direct deposits for your employees, corporate credit cards, discounted credit card processing fees, interest bearing business accounts or reduced or no fees on wires and other transactions? Does your bank offer a special loan program for people buying your risk units? If you don’t know, you can’t ask.

Do you know your bank’s current policies? With the changing landscape in the financial industry, banking policies can change weekly. For example, the Fed can issue new requirements as banks buy banks, fold or get taken over, which changes their loan policies.

At Eckhaus, we have a rental customer who was with a bank for more than 20 years. The bank was bought and the customer had to reapply for a credit line under the new bank’s policies. After several weeks and lots of paperwork the client was approved, only to have the new bank bought by an even bigger bank. (Luckily the company had up-to-date financials, or it would have taken even longer.)

At that point the client had to start over with a new bank and more paperwork, while the client had to pay for the cars—not good! We worked with our customer, the bank and the supplier to make everyone happy.

You need to check with the bank on a regular basis about any changes in policy and loan requirements. If you receive a policy change in the mail, read it. If you have a question, call. If you don’t like the change, call.

Does your bank know who you are and what you do?

At one time, banking was a personal business. The banks were local and bankers knew their customers. While decisions were based on sound financial principles, an individual’s hard work and standing in the community counted. Now decisions are often made by computers located thousands of miles from a bank. Still, fostering a personal relationship can open doors normally closed.

You would be surprised how little bankers know about how their customers make money.

When they look at a rental car company, what do they see—a giant mobile liability that is losing value on a daily basis, or a cash-generating machine?

You need to educate them. For example, when you tell them you are buying repurchase/buyback cars, do they really know what that means? Do they understand that their risk is really the monthly depreciation times the minimum term? We’ve heard firsthand that banks require their loan officers to submit a report every time they speak with or visit a customer. They want to make sure the customer has a handle on the business and that it is healthy.

Show your bank that you really understand your business. Offer to take your banker and his or her boss to lunch. Ask if there is anything you could do to make their job easier. Invite them to your office to meet your team. And don’t forget to always send them your updated financials at the end of every quarter.

[PAGEBREAK]

Are you depreciating your cars properly? How you depreciate your cars can give your bank heartburn.

Is your 2-3 percent depreciation a month reasonable? Do you review this every month and adjust upward if the cars are getting more miles on them? Is it just a paper transaction every month or do you really write a check for it?

Just think how much more comfortable your banker would be if you sent him or her a check every month to reduce your outstanding credit line.

Do You Have a Succession Plan? What happens if, God forbid, you die? Do you have competent people in place to continue the business, or will “Crazy Uncle Larry” take over? Do you have Key Man insurance, which pays out in the event of your death? Is there a buy-sell agreement in place that spells out the terms of the transfer of the business to the surviving partners?

You need to explain your plan and introduce your bank to your key people. Make your bank feel comfortable with you as a partner.

Does the bank know how much business you do with them? Do you?

If the bank is handling your merchant account, do they know how much money your company runs through them?

If you have a 200-car fleet, you should be easily running more than $2 million a year through your merchant account. Assuming this is all credit or debit card transactions with a 2 percent transaction fee, your bank is making around $45,000 a year from your company.

Plug in your own numbers. In this scenario, a 0.5 percent reduction in transaction fees would put about $5,500 a year back in your pocket for each group of 100 cars.

If you require your employees to have accounts at your bank for direct deposit, the bank has those accounts because of you. Consider that all of your employees’ salaries for the year are money flowing through your bank. Your employees will also use the bank for personal loans, car loans, mortgages, credit cards and more.

The same can be said for corporate credit cards and loans, and the consumer loan program set up for people buying your risk units. When you add it up, it equals a lot of money. Maybe it is your bank’s turn to spring for lunch.

Does your bank know how great you are doing? Signed a new corporate client? Reached new utilization levels for the quarter?

Sponsored a local charity event? Good news! Let your bank know, let your employees know. Email is your friend!

If you’re with a local bank, let your customers and your bank know how much you buy within the community.

What are you doing to make your bank a good rental customer?

Do you offer discounts to your bank’s employees and their customers? How about a “First National Bank” special? Look at cross-promotional opportunities. If your bank has 20,000 local customers and 1 percent start renting from you, imagine the added revenue.

Can you position yourself so the bank will introduce you to a new corporate customer? If they have a “customer spotlight,” can you be one of the companies they shine the light on?

Now that you have answered all these questions there is one last one:

Is this the right bank for you?

So you have a plan. You know your loan needs for the next 12 months. You know how much business you give your bank and you know what they offer in return. Your financial package is up to date, and you have a process that keeps it up to date. Now is a good time to see what other banks might offer.

But remember, if you have a long-term relationship with your bank, you must weigh carefully whether getting a quarter point lower on your loan rate from a new bank is really worth it. Got a suggestion on how to be your bank’s best customer? Email it to info@autorentalnews.com.

Mark Eckhaus is CEO of Eckhaus Fleet LLC, one of the largest independent fleet distributors to the rental car industry. Mark held management positions with Alamo and Standard Rent A Car and was a partner in multiple Budget locations in California and Maryland. Mark is a principal in several new car dealerships. Mark can be reached at Meckhaus@aol.com.

Tim Yopp is chief technology officer of Eckhaus Fleet LLC. Eckhaus Fleet represents Hyundai, Suzuki, Toyota and other manufacturers to the rental car industry. He can be reached at tim@eckhausfleet.com.

[PAGEBREAK] Joe Opferman of 1st Source Bank has this advice on how to strengthen the relationship with your banker: Given that you are talking to a banker who understands the industry and basic drivers to profitability, your job is to show the banker how your business plan mitigates risk. You need to make the case that your plan can be adjusted with demand:

Do you have cars in your fleet that have not historically depreciated significantly, so they can be sold without a loss?

Can you show a stable market with few peaks and valleys, which allows fleet to run longer, thus not requiring such immediate fleeting up or down?

Do you own a portion of the fleet outright?

Of course, the greater the net worth of your organization and the higher your RPU, the will lower your risk as well. Can you demonstrate these points?

Experience with a lender is very important and can overcome some one-time negative events. The banker who feels comfortable with the operator will be more inclined to lend.

Also, when you tell a banker something, deliver on the promise. Telling a banker one thing and then doing another does not inspire confidence. Bankers expect changes in plans but they want to know why and usually not after the fact.

Tell your banker the good, the bad and the ugly and demonstrate that your organization can withstand a downturn in the market. Show that you are prepared to make the adjustments required to meet demand.

Approach your banker as a partner. Remember, a bank succeeds only if the customer does as well. When a banker has confidence that the operator has a good grasp of his economic drivers and a defensive plan, the banker can then move forward.

More Fleet Acquisition

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →

Rethink The Future To Avert A Race To The Bottom

Rental car operators heard a sobering industry message and a stern challenge at the close of the International Car Rental Show.

Read More →

DriveItAway, Free2move Plan Shared Fleet Program for Independent Rental Fleet Operators

Vehicles would be placed with participating rental operations to support car renter demand and provide additional fleet capacity.

Read More →

Stellantis Recalls 1.3 Million Jeep Vehicles Worldwide Over Fire Risk

Stellantis is recalling more than 1.3 million Jeep Wrangler and Gladiator models worldwide over a fire risk linked to power steering pump wiring.

Read More →

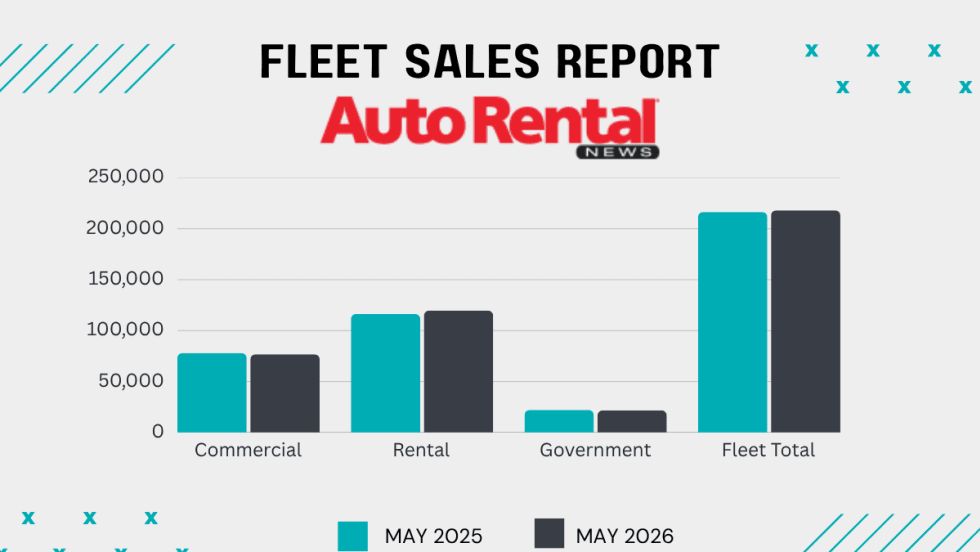

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

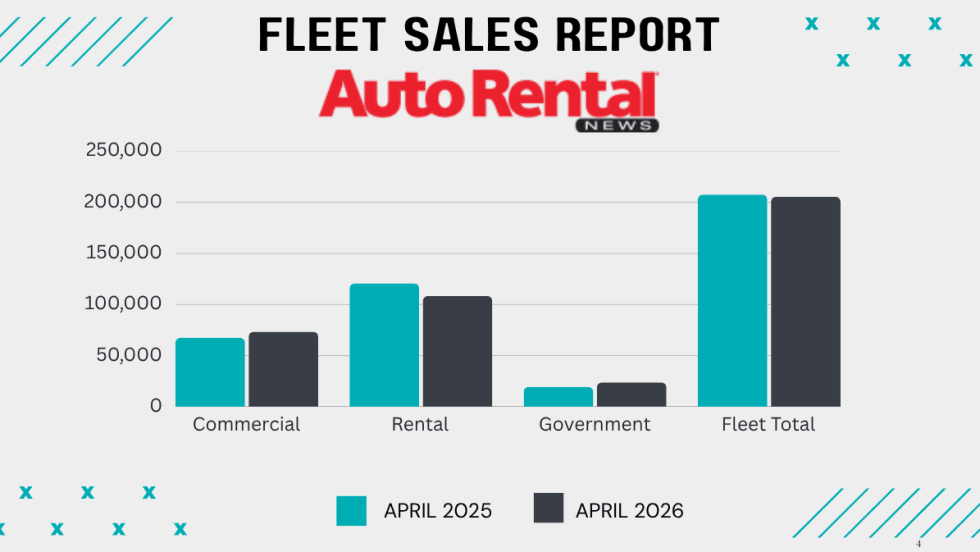

Monthly Rental Fleet Sales Dip Again As YTD Numbers Flatten

Pull-ahead demand for rental cars in the second half of 2025 appears to be slowing purchases so far this year.

Read More →

DriveItAway Transitions To OTCID, Expands To 40 U.S. Markets

The dual milestone propels the company toward its goals of accessing longer-term capital markets and deploying a national platform.

Read More →