KBB: Residual Values to Dip in 2010

According to Kelley Blue Book, in 2009, the average vehicle maintained 34.2 percent of its original value after five years in contrast to 2010 models, which are projected to maintain an average of 32.6 percent of their original MSRP.

The following is Kelley Blue Book's December 2009 Residual Analysis, which compares 2009 and 2010 residual forecasts for all major brands.

The fourth quarter of 2008 saw used-vehicle values fall at unprecedented levels with values depreciating 3.0 percent and 3.9 percent for November and December, respectively. This depreciation occurred at a time when there was uncertainty not only in the minds of dealers, but in the automotive industry and overall economy. Some of the key economic and social factors contributing to the depreciation in late 2008 were a quickly eroding new-vehicle market, rising unemployment, and highly volatile gas prices. These factors played a key role in eroding demand for both new and used vehicles to a point that vehicles depreciated well beyond what was considered typical seasonal depreciation for the fourth quarter.

While the market had been returning to more normal patterns through the last few months, used vehicles depreciated more in the last month (4.1 percent) than during any other period this year, proving that volatility is still at play in the used-car market. While depreciation during this time of year is considered typical, values dropped 1.1 percent more in November of 2009 than what was considered one of the worst periods of sales ever, November of 2008. According to Kelley Blue Book’s analysts, the additional drop in values can be attributed to soft demand from dealers as a result of weakened economic conditions, dealers waiting to restock inventory until the New Year as well as slight increases in the supply of used vehicles.

“The decline in November went well beyond traditional seasonal trends and we have already seen depreciation that is outpacing the aggressive drops of late 2008,” said Juan Flores, director of vehicle valuation for Kelley Blue Book. “We expect softening in the market to continue all the way into the first quarter of 2010.”

Another factor pushing values downward is an increase in trade-ins from the higher than expected new-vehicle sales in October, thus reducing the need for dealers to attend auctions and replenish their used-vehicle inventory. While dealers typically hold off on replenishing their used-vehicle inventory until the first of the year, the increased trade-ins from better than expected new-vehicle sales has only exacerbated the already weak demand conditions expected for this time of year.

New-Vehicle Sales Improve

While seasonally adjusted new-vehicle sales have been consistently trending below a SAAR of 10 million for most of 2009, October new-car sales improved to an annualized rate of 11.2 million. November then came in a bit lower than October with an annualized rate of 10.5 million, but even that figure is an improvement relative to earlier in the year. The improvement in sales during the fourth quarter has come as a surprise, as the economy has been hit by a rising unemployment rate currently pegged at 10 percent, gas prices that continue to rise month after month, and a report from the Wall Street Journal indicating that 1-in-4 homeowners with a mortgage owes more than the value of their home.

Kelley Blue Book’s analysts predict that with so many variables applying downward pressure to demand, any sustained improvement in new-vehicle sales will need to be supplemented by generous incentive support from manufacturers to keep prices affordable.

Cars

Values for cars dropped 3.9 percent on average with the most aggressive depreciation coming from subcompact cars and compact cars, which dropped 6.0 percent and 5.0 percent, respectively. The cars leading the depreciation in these segments were the Chevrolet Aveo (- 9.7 percent), the Scion xA (-7.9 percent), the Kia Spectra (-8.3 percent) and the Hyundai Tiburon (-7.8 percent). While these drops are certainly more aggressive than in previous periods, we must keep in mind that the average dollar drop for these segments is generally less dramatic than for many other segments. With an average market drop of $623, the average drops of $519 and $459 for subcompact and compact cars don’t seem so pronounced. Any weakness in these segments may be short lived, especially if gas prices continue to trend upward. December may be another down month for subcompact and compact cars, but we are not predicting long-term weakness in these segments.

Trucks

Although truck values have been uncharacteristically strong through most of 2009, they were not spared from the aggressive depreciation in November. The segments hit hardest were full-size trucks and SUVs which depreciated 6.6 percent and 7.2 percent respectively. The Dodge Ram 1500 (-8.6 percent), Chevrolet Silverado 1500 (-8.3 percent), and Chevrolet Tahoe (-11.5 percent) led the depreciation in these hard hit segments. The depreciation can be attributed to a modest rise in gas prices, a slight correction to the substantial increases in auction prices and overall weakness in used values during this time of year.

<'img src=/fc_resources/ARN News 123009 chart 4.jpg border=1'>

2010 Q1 Outlook

Rising fuel prices, soft demand, and limited credit availability have all factored into Kelley Blue Book’s projections for the first quarter of 2010. Company analysts expect that the aggressive depreciation heading into the end of 2009 is expected to continue into the first quarter of 2010 for truck segments, while fuel-sipping subcompact cars can expect to appreciate. Through the first quarter of 2010, full-size trucks are expected to drop 2.6 percent while full-size SUVs are expected to drop 3.8 percent, while subcompact cars should rebound 3.3 percent, coinciding with an uptick in demand for these vehicles. These shifts in the New Year are based on our expectation for a slight shift in demand from full-size trucks and SUVs towards compact and hybrid cars, similar to what we observed during the summer of 2008. Bucking the trend, mid-size crossovers are only expected to drop 0.2 percent through the same period, indicating that values in these segments should be relatively stable.

Rising gas prices will play a significant role in this trend in addition to lackluster demand resulting from continuing weak conditions and a limited access to credit. With unemployment currently at 10 percent and a quarter of home mortgages currently underwater, consumers may begin to shy away from buying expensive, fuel-thirsty trucks and SUVs and once again move toward relatively affordable subcompact and hybrid cars.

According to Experian, 83 percent of all new-car buyers and 53 percent of all used-car buyers possess prime plus credit scores. These are just the latest figures that are coming about as a result of financial institutions continually tightening their lending standards. As financial institutions continue to restrict lending to only those with impeccable credit scores, demand for new and used vehicles will likely suffer. In addition, rising delinquency rates for auto loans only stand to further reduce the availability of credit, adding to the already significant downward pressure on demand.

A Look at 2009 and 2010 Residual Forecasts

- Eric Ibara, director of residual valuation consulting, Kelley Blue Book

For the last several years, the average vehicle has maintained close to 35 percent of its original value after five years. The downturn in the economy has hit the automotive sector hard in the last year. Consumers are feeling the pinch not just in the depreciation of their home, but also in the value of their vehicle, as Kelley Blue Book is seeing residual values of new cars suffer compared to last year. In 2009, the average vehicle maintained 34.2 percent of its original value after five years in contrast to 2010 models, which are projected to maintain an average of 32.6 percent of their original MSRP.

The last 18 months have been extremely volatile from both a sales and valuation perspective. However, based on Kelley Blue Book’s latest valuation methodology and forecasting abilities, the company’s analysts project that the New Year should mark a return to more normal depreciation patterns. Additionally, it is expected that the lower rental volume will contribute to a more limited supply of used cars, which may result in rising values in some segments in the coming years.

While the government took its time declaring the nationwide recession, it has been quick to announce that economically, we have turned the corner. As data shows a healthier economy in 2010, Kelley Blue Book analysts expect that recovery in the auto industry will be gradual and prolonged. One factor helping the industry is stabilizing gas prices. Kelley Blue Book is forecasting that gas prices will be stable through the next three to five years with per-gallon prices remaining between $2.66 and $3.50. This predicted long-term stability in fuel prices reduces market variability and allows financial institutions to better manage their lease portfolio.

Best Resale Value Brands

This year’s 2010 overall Best Resale Value: Brand award goes to Toyota. For the first time, Kelley Blue Book also named a Best Resale Value: Luxury Brand, and that prestigious honor is awarded to Toyota’s upscale sibling, Lexus. On average, 2010 vehicles under the Toyota nameplate are expected to maintain 38.8 percent of their MSRP after five years, and Lexus vehicles are projected to maintain 39.3 percent.

For 2010, the brands projected to best maintain their value should be congratulated for making it though a volatile marketplace defined by economic uncertainty and significant drops in fuel prices. On the 2010 list, the gap between the brands at the top and the rest of the pack is closing. Overall, products are getting better in quality and in value, driving greater competitiveness and slower depreciation.

Criteria for Kelley Blue Book’s Best Resale Value Awards require a brand to have a minimum of four nameplates in its portfolio, a factor that eliminates the highest-ranking brand performer year-after-year, MINI, which carries an average five-year residual percentage of 45.9 percent for its 2010 models.

Below is a look at some of the brand ranking changes over the last year:

Despite lower residual estimates for the fuel-efficient segments and a drop in overall brand value of 3.9 percentage points from 2009, Toyota still takes the 2010 award for Best Resale Value: Brand.

“Values in the compact, fuel-efficient segment dropped severely, which hit Toyota, known for fuel efficiency, quite hard,” said Eric Ibara, director of residual consulting for Kelley Blue Book. “While he Yaris, Corolla and Matrix residuals are down double digits from 2009, the brand was given a boost by its versatile line-up—residuals in the truck segment were up 2 to 3 percentage points year-over-year, helping the brand to maintain value leadership.”

Domestics

Residual values of vehicles produced by the domestic automakers saw an uptick versus last year. With several new-model launches from the domestics and the strength in the truck market compared to last year, each of the Detroit Three have vehicles with exceptional resale value.

Ford Motor Company

Ford, the only domestic auto manufacturer not to partake in bailout funds from the Federal government, seems to be in a good position from both a cash-flow perspective and now positive projected resale values. On the strength of the truck and SUV market, the Ford brand gained 2.4 points from last year reaching a 32.8 percent brand average. Ford went from being ranked 25th in resale value among all brands last year to 12th this year. The Blue Oval also saw a lift due to redesigns of popular products such as the Mustang and the Taurus.

Other Ford brands including Lincoln and Mercury did little to lift the Ford brands’ future values. A rise in both of Lincoln’s SUVs, Navigator and MKX, helped to offset the heavy downward pull of the Town Car value, ending mostly flat year-over-year with a brand average of 27.1 percent. Mercury dropped 4.1 percentage points to a 28.1 percent projected residual average for 2010. The Mercury brand’s decrease was due in part to the aging Mercury Marquis.

General Motors

General Motors went from nine brands to four in just the last five years. Despite the last tumultuous year, General Motors increased its combined residual average of the four remaining brands to 31.3 percent, up 1.8 percentage points from last year.

The now-defunct brands, Hummer, Saab, Pontiac and Saturn, were at 32.4 percent last year. Those brands have a 2010 average residual value of 27.7 percent, an immediate year-over-year drop of 4.7 percentage points.

Chrysler

After emerging from bankruptcy, Chrysler struck a deal with Fiat and introduced the possibility of bringing some of Fiat’s smaller European designs to the United States under the Chrysler group. However, the uncertainty of those future product plans and vehicle designs have cast a shadow over the future values of new Chrysler products. With no new redesigned Chrysler products for 2010, and an uncertain product future, the company’s overall residual average for 2010 comes in at 29.5 percent.

Bankruptcy/Defunct Brands

Kelley Blue Book reports that the bankruptcy filings themselves had little impact on residual and used car values. In fact, kbb.com observed an increase in Web site traffic for General Motors and Chrysler vehicles during the bankruptcy filings, finding consumers primarily interested in finding a good deal and not necessarily resale value, servicing or warranties down the road. Bankruptcy has left two brands in its wake so far; Pontiac and Saturn. Both of these brands are projected to meet different fates. Kelley Blue Book already is seeing other GM dealers buying used Pontiacs at auction, helping the brand to maintain its values. Pontiac’s projected 2010 residual average for remaining products comes in at 25.6 percent.

Kelley Blue Book expects the impact will be more severe for Saturn, whose residual average is down 5 percentage points to 28 percent. Saturn is currently projected slightly higher than Pontiac because its two remaining models, the Outlook and the Vue, compete in the more stable SUV category.

Kelley Blue Book performed an analysis on used-car values for Oldsmobile as a case study for the possible outcomes for both Pontiac and Saturn. This included the impact of mileage, condition, seasonality, market conditions, volume, demand, competition and a number of other factors. The shutdown of Saturn is similar to the shutdown of Oldsmobile, but the two scenarios are still quite different. Oldsmobile shut down over a period of more than three years and continued to introduce new products, including the Bravada, even after the closure announcement. With Saturn, production was halted almost immediately and the sell-down of inventory is expected to occur faster. Like Oldsmobile, the impact will differ by model, where more differentiated vehicles like the Sky can expect less of an impact. The impact of the shut-down for Saturn is expected to be less severe than it was for Oldsmobile.

Market Watch

Below are the results from Kelley Blue Book’s Market Watch, measuring new-car shopper activity on kbb.com.

New-car shopper activity declined slightly in November (down 6 percent), which was consistent with seasonal trends. The latest decline pushed traffic to its lowest level in a four-year period.

Declines occurred across nearly all brands with Jeep being the one exception, up 3 percent month-over-month. New model-year introductions of the Wrangler and Patriot helped offset shopper activity depreciation in other Jeep models. GMC also fared well, down only 3 percent from last month and up a considerable 33 percent year-over-year.

Pontiac traffic continued to wane due to the discontinuation of the brand and suffered a 21 percent decline from October 2009. Buick did not sustain its shopper activity increase from October, falling 17 percent, largely due to a sharp decline in LaCrosse traffic. However, Buick’s year-over-year traffic remained elevated at 62 percent. Mitsubishi experienced a similar month-over-month decline, down 16 percent, driven primarily by double-digit declines in their highest trafficked vehicles, Lancer and Eclipse.

More Fleet Acquisition

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

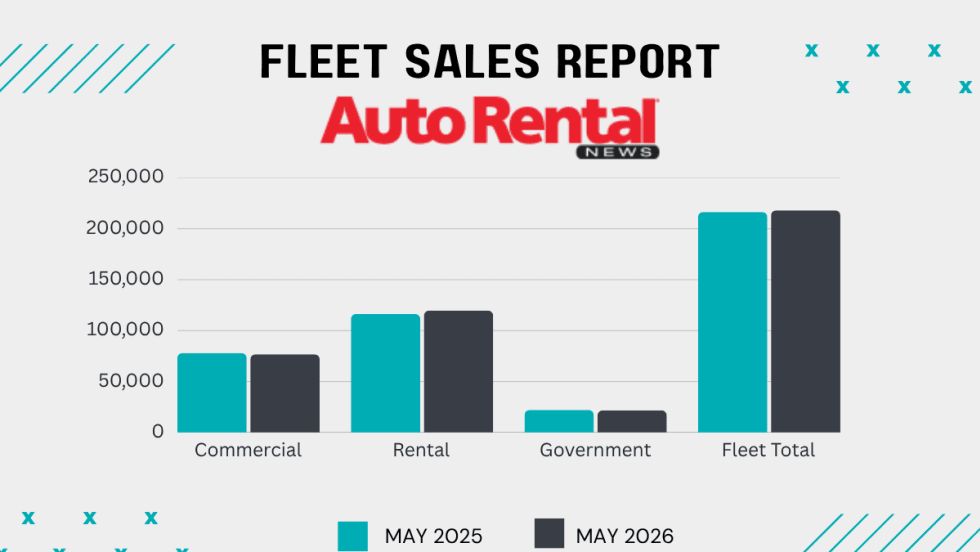

Monthly Rental Fleet Sales Dip Again As YTD Numbers Flatten

Pull-ahead demand for rental cars in the second half of 2025 appears to be slowing purchases so far this year.

Read More →

DriveItAway Transitions To OTCID, Expands To 40 U.S. Markets

The dual milestone propels the company toward its goals of accessing longer-term capital markets and deploying a national platform.

Read More →

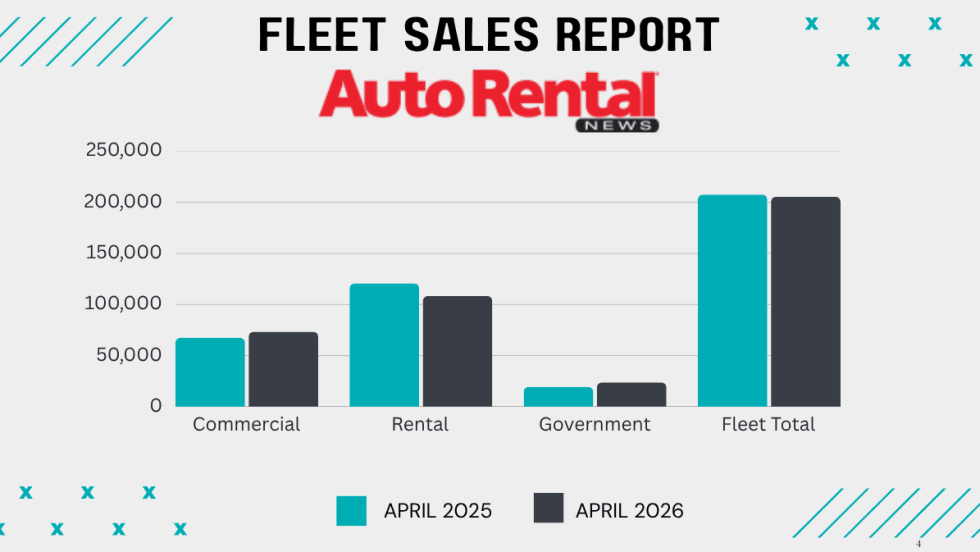

Rental Fleet Sales Stay Ahead In Q1 Despite Monthly Dip

Vehicle sales into commercial fleets are outpacing rental car fleet purchases so far this year.

Read More →

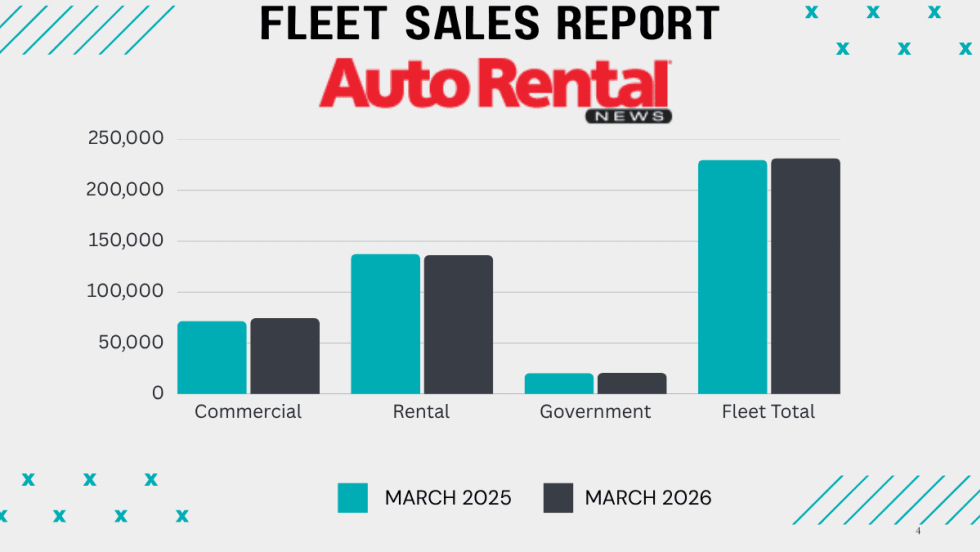

Rental Fleet Sales Slow In February Ending A Strong Streak

Commercial fleets posted the most gains, sustaining increases in monthly and year-to-date fleet sales

Read More →

How It's Still Possible To Run An Electric Rental Fleet

This Season 2 / Episode 4 of Auto Rental News’ Industry Newsmakers series broaches a difficult subject in car rental: How do you make EVs succeed?

Read More →

Avis Budget Group Reports Near $1 Billion Loss Tied To 2025 EV Fleet Write-Down

Following Hertz, the company is the second global car rental conglomerate to sustain sizable losses due to lower customer demand and usage of electric rental cars.

Read More →

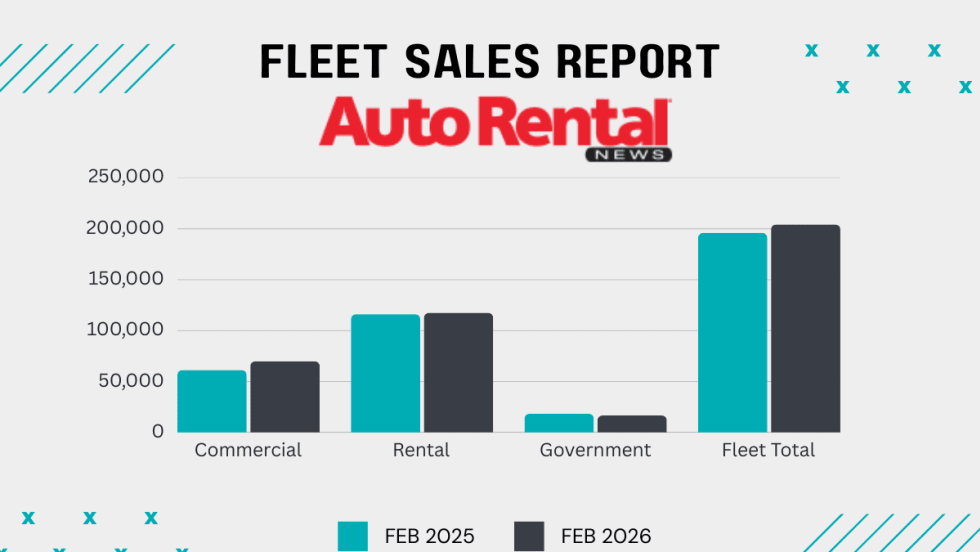

Rental Fleet Sales Shoot Ahead From The Starting Line

Rental car operations continued their 2025 reputation as the top driver of fleet sales.

Read More →