Car Rental Q&A: How Can I Lower My Vehicle Liability Insurance Premium?

Q: The automobile liability insurance premium for my rental cars is costly. It is our location’s biggest expense after my employee costs. Some of my associates in other states pay much less per car, per month than I do. What can I do to minimize this expense?

Q: The automobile liability insurance premium for my rental cars is costly. It is our location’s biggest expense after my employee costs. Some of my associates in other states pay much less per car, per month than I do. What can I do to minimize this expense?

— Richard Eramian - CLS Auto Rental, Richmond, Va.

A: It is true, automobile insurance premiums for rental cars can be expensive. There are many reasons that different rental car companies pay higher or lower “per car, per month” (pcpm) rates than others.

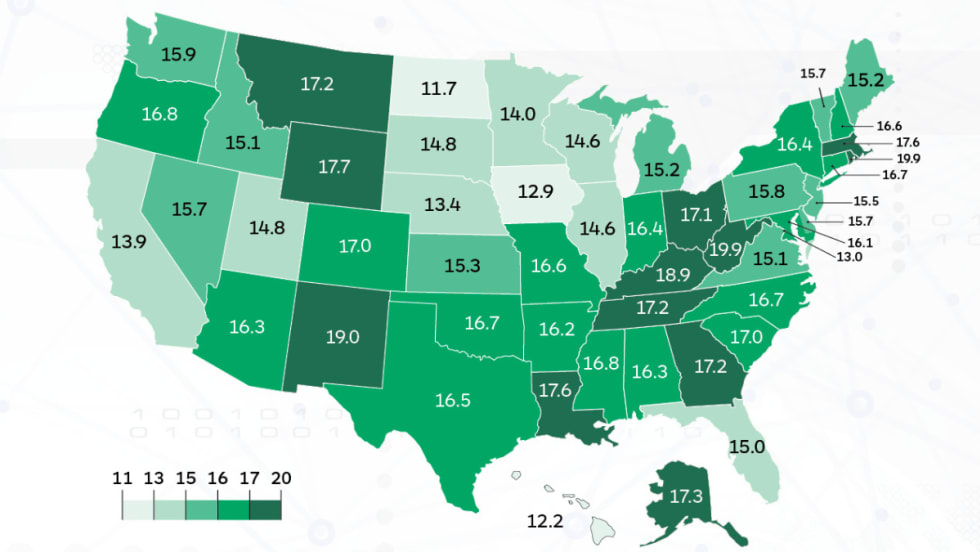

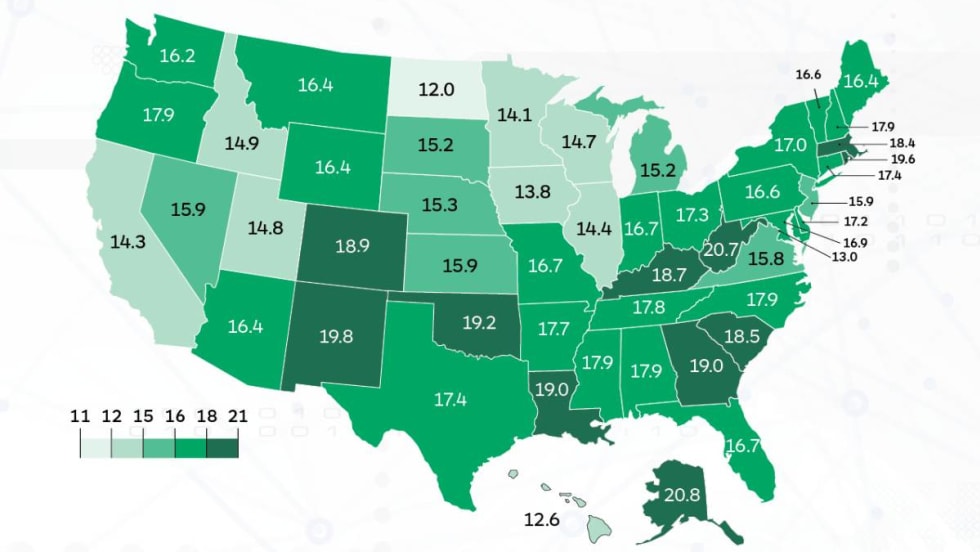

One reason is that premiums can vary widely by state jurisdiction. For example, if your operation is in Michigan, your fleet liability coverage is primary for the renter, with financial responsibility limits of $20,000/$40,000 and no-fault medical is required for passengers. You may pay significantly more than in, say, California, where the rental car company is only obligated to give the renter (on a secondary basis) state financial responsibility limits of $15,000/$30,000 and no medical coverage.

It isn’t likely that you can pick up and move across the country to a state with a more favorable legal climate. Let’s focus on some things that you can control that may help to minimize losses and your ultimate premium costs.

Tighten up your counter procedures and stick to them.

Whatever your qualifications are — if the potential customer cannot meet your criteria, then do NOT let this person rent your car. Having a credit card or insurance on a personal vehicle are signals that the individual is demonstrating responsibility. This means that the person will drive safer and take better care of your car.

Marginal renters create claims. It is better to have a car sitting on the lot than compromise your standards and have a loss that will cost you time, money and headaches.

Avoid fraudulent or escalating claim costs.

When your car comes back damaged or your renter reports an accident, take the time at that moment to document. Preserve a record of the damage to the vehicle by taking pictures. Get the facts of the incident, the names and contact information of all involved (including the passengers of your car) and secure a signed accident statement from the driver.

Too often, long after the claim is filed, third parties allege more serious damage or more injured parties. Your detailed first report of loss is your best defense.

Prevent negligent entrustment accusations by third parties.

Properly maintain and service your vehicles. It is most important to track all service records including: oil changes, fluid levels, brake changes, tire rotation/replacement and windshield repairs. Proof of a well maintained vehicle virtually eliminates allegations such as “the brakes failed.”

Verify that your renters have their own coverage. If you have counter products available, you should sell supplemental liability insurance (SLI) to your renters. If an injured claimant has a deep pocket of liability limits provided by someone else’s insurance, this renter is less likely to pursue trying to bring the rental car company into a lawsuit.

These are the most critical items within your control that lead to minimizing losses and insurer claim payouts.

Insurance companies look at your record — the frequency of losses that your location has and the severity or total amount paid as a result of claims from your location.

The less that an insurance company has to pay on your behalf, the lower your loss ratio will be. The better your loss ratio is, the better opportunity you have for a lower premium. It may not be as low as your buddy’s in another state, but at least you’ll know that you’ve taken positive steps to contain your rental fleet liability insurance costs.

What's Your Question?

Email your car rental operation-related questions to Auto Rental News by emailing chris.brown@bobit.com.

Rental insurance experts from Sonoran National Insurance Group are happy to answer your insurance and risk management questions to help you better protect your operations and maximize your coverage. Feel free to contact them directly at inquiry@sonorannational.com.

More features can be found here from the March/April issue of Auto Rental News.

More Fleet Insurance

Using AI to Create Clarity, Not Conflict, in Rental Car Damage

Rental companies still need people, policy, judgment, and thoughtful implementation, with operators remaining in control of the customer experience.

Read More →

Go Rentals, Repair Provider Partner To Ease Insurance Claims Experience

The arrangement helps reduce the stress of collision repair for vehicle owners by connecting them to reliable, timely rental cars.

Read More →

U.S. Collision-Related Rental Length of Rental Declined Modestly in Q4 2025

While LOR continues to decrease from post-pandemic highs, ongoing market and economic conditions could impact future results.

Read More →

Beyond The Rental Desk: Inside Car Rental’s Push To Simplify

Greater transparency, simplified digital access, and connected fleets will be the key factors in determining who comes out on top over the next 10 years.

Read More →

Tripiamo Brings Certified Driving Confidence Training For Car Renters

Driving abroad is one of the leading causes of death among international travelers, who are not used to new traffic patterns.

Read More →

AI in Car Rental Should Be the Customer’s Advocate, Not Accuser

Opinion/Editorial: What happens when AI randomly overcharges car renters outrageous fees and penalties?

Read More →

TSD Mobility, Canopy Connect Partner to Ease Insurance Verification

The new integration brings streamlined functionality to rental agents and dealerships.

Read More →

Length of Rental Could Be Finding a New Normal of More Days

The industry may not be returning to the lower LORs of 2019 and 2020 as two years of declining repair shop backlogs appear to flatline.

Read More →

Gallagher Insurance Hires Broker Focused on Rental Car Operations

The former rental fleet executive informs his insurance practices with the everyday realities of managing rented vehicles.

Read More →

4 Global Trends in Carsharing for 2025

Despite operational challenges and questions, the global car-sharing market continues growing and will likely double during the next decade.

Read More →