Black Book: All 24 Segments Decline, Again

In Ricky Begg’s weekly “Beggs on the Used Car Market” column, Beggs points out that for the second week in a row, all 24 vehicle segments have declined. Compact Cars declined the least at only -$14, while Prestige Luxury Cars declined the most at -$87.

Ricky Beggs, managing editor of Black Book, presents this edition of "Beggs on the Used Car Market."

What a week it has been in the used market. We had some slightly different comments from the auction arenas across the country this past week. There continued to be the typical comments from dealers and auctioneers like "many no sales" and the "under $10,000 vehicles are still selling". This past week some of the dealers' thoughts were on a broader perspective as the comments referenced the stock market, questioning the overall economy, and even thinking further ahead, questioning the possible aggressiveness to get new cars sold in the upcoming final few months of 2011, and how this might affect the values in the used market. I think we are already seeing the reaction to some of these thoughts as we have seen a higher level of no sales on the used 2010s and 2011s.

The activity and trends in the market this past week brought the most necessary vehicles adjusted to almost 2900 per day. Thus the total number adjusted for the week was also a record volume. We have been tracking daily changes since February 2008 and have never reached this level.

Within these adjustments there were fewer increases at only 15%, since the 11% from the week ending November 19, 2010. This past week was also the largest dollar decline of the adjustments since the same week last November. This week's decline of the adjustments was at -$119. Last November it was -$122. The change this week was a 60% increase in the overall change from the previous week.

Last week we mentioned that it was the first week where all 24 segment types we track had declined for the week. Well now there are two weeks of this change pattern. We now have 6 consecutive weeks where the average change within the car segments has declined a greater amount, this week coming in at -$43. The best segment retention for the week was the Compact Cars (SCC) at only -$14. The segment declining the most this past week was the Prestige Luxury Cars (PLC) at -$87. This segment has declined the most within the cars for each of the past 3 weeks. The Entry Mid-size Cars (EMC) and the Entry Level Cars (ELC) also required some larger adjustments for the past week at -$61 and -$58 respectively.

Within the truck segments for the 4th consecutive week all 14 segments have declined. With the trucks still being soft in the market the overall average change continues to jump all around falling $15 more this week than the previous week and the largest overall average change at -$53 for the past 4 weeks. The Full-size Pickups (FPT) and the Luxury SUVs (LSU,) with significant declines of -$151 and -$147 respectively, overshadowed the -$13 with the Compact Pickups (CPT), the -$22 of the Full-size SUVs (FSU) and the -$30 with the Full-size Crossovers (FXU).

I mentioned earlier the tough sell for the 2010s and 2011s. Even with these challenges we still were able to get enough market data to include used values on 14 additional 2011 models.

With the volume of necessary adjustments and the current volatility of the various segments, the Daily adjustments we provide can be an edge to you in your purchasing efforts. Another thought is that in spite of the tough economy 15% of the adjustments were still increases to the previously published values and that average increase was just over $111.

I am looking forward to being part of the IARA Summer Roundtable this week celebrating the 10th Anniversary of this group of leading industry remarketers with discussions on the market, issues that affect the industry and the IARA being the voice of the remarketing industry. I will share some insights from the roundtable next week when we get together for this blog.

Until then, I hope you have a great week.

Ricky Beggs

More Rental Operations

U.S. Business Travel Drives $623 Billion+ in Economic Impact as Spending Reaches $538 Billion

The data also underscores the industry’s strong multiplier effect across the U.S. economy, revealing that each dollar invested in business travel in 2024 generated $1.16 in GDP.

Read More →

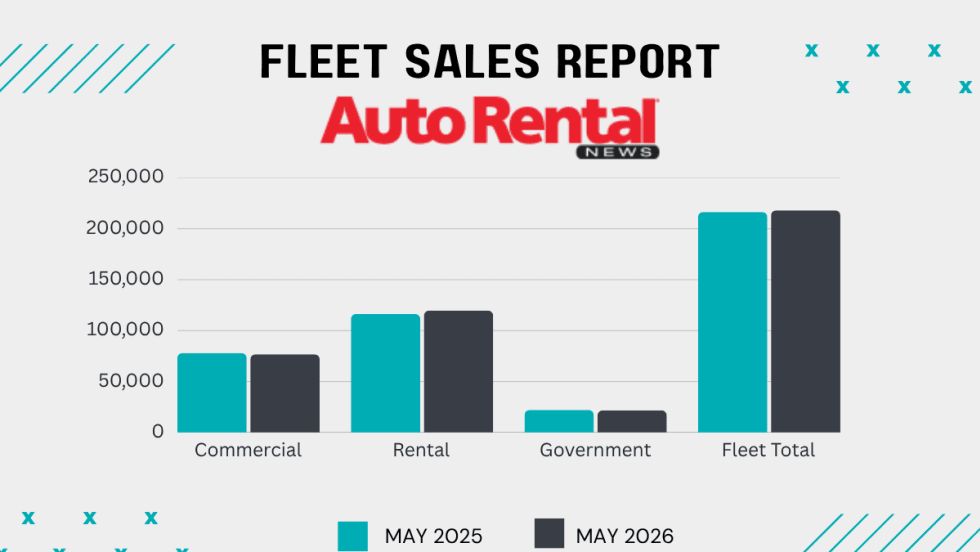

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Grow Your Rental Business Beyond Cars

Rental fleet operations are facing numerous evolving challenges and opportunities from AI technology to rate and revenue management, to customer service and business growth.

Read More →

Using AI to Create Clarity, Not Conflict, in Rental Car Damage

Rental companies still need people, policy, judgment, and thoughtful implementation, with operators remaining in control of the customer experience.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Southwest Airlines Selects CarTrawler For Its Car Rental Booking Platform

The platform is designed to allow customers to compare and book rental vehicles more easily during the travel booking process.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

Government Affairs Executive Wins Leading Rental Car Industry Award

Robert Muhs started in the car rental industry with Avis Budget Group two years before the first International Car Rental Show.

Read More →

Green Motion Expands Its African Presence with Mozambique Launch

This new rental car outlet reflects the growing demand for reliable transportation and the emphasis on sustainable travel across the continent.

Read More →

RentalMatics, GeoInt Partner On Rental Car Speed Tracking Tech

Rental operators can now detect and act on speeding while vehicles are still on rent, thereby reducing fines, admin workload, vehicle wear, and safety risks.

Read More →