Dollar Thrifty Reports $131.2 Million Net Income for 2010

Dollar Thrifty Automotive Group increased net income from $45 million in 2009. The company noted that rental revenue was flat on a year-over-year basis and also discussed the status of a potential merger with Avis Budget Group.

Dollar Thrifty Automotive Group, Inc. reported results for the fourth quarter and year ended December 31, 2010. Net income for the 2010 fourth quarter was $12.5 million, or $0.41 per diluted share, compared to net income of $11.5 million, or $0.42 per diluted share, in the fourth quarter of 2009. Net income for both the fourth quarter of 2010 and 2009 included a net favorable impact on income of $0.14 per diluted share, related to changes in fair value of derivatives and impairments of long-lived assets.

Non-GAAP net income for the 2010 fourth quarter was $8.3 million, or $0.27 per diluted share, compared to non-GAAP net income of $7.7 million, or $0.28 per diluted share, for the 2009 fourth quarter. Non-GAAP net income excludes the (increase) decrease in fair value of derivatives and non-cash charges related to impairments of long-lived assets, net of related tax impact. The company noted that both its GAAP and non-GAAP earnings were negatively impacted by $2.1 million in merger-related expenses incurred during the fourth quarter of 2010. Additionally, the company noted that on a comparative basis, gains on risk vehicle sales declined in the fourth quarter of 2010 by $16.3 million as compared to same period last year.

The company reported Corporate Adjusted EBITDA for the fourth quarter of 2010 of $30.2 million, compared to $26.2 million in the fourth quarter of 2009. Corporate Adjusted EBITDA in the fourth quarter of 2010 was negatively impacted by the $2.1 million of merger-related expenses, and on a comparative basis, reflected a reduction of $16.3 million in gains on risk vehicle sales as discussed above.

"This quarter marks our eighth consecutive quarter of year-over-year double-digit growth in Corporate Adjusted EBITDA. Additionally, excluding the impact of merger-related expenses, 2010 full year results represent an approximate $100 million improvement in Corporate Adjusted EBITDA compared to the previous best year in the company's history," according to Scott L. Thompson, president and chief executive officer. "We are proud of the company's financial performance despite the lethargic economic environment in 2010. We appreciate our employees' contributions to the company's success and their ongoing focus on providing outstanding service to our value-oriented customers."

For the quarter ended December 31, 2010, the company's total revenue was $349.1 million, as compared to $345.3 million for the comparable 2009 period. Vehicle rental revenues for the quarter were up 1.6 percent, driven primarily by a 2.8 percent increase in transaction days that was partially offset by a 1.2 percent decrease in revenue per day. The average fleet for the quarter was up 1.6 percent, while utilization for the quarter increased 90 basis points from last year's fourth quarter.

"Revenue for the quarter was in line with our expectations, as overall transaction volumes continued to reflect an improving travel market. We experienced a minor decline in fourth quarter revenue per day as we faced a slightly more competitive market and a very difficult comparison, having achieved a 12 percent increase in revenue per day in the fourth quarter of 2009," according to Thompson.

Per vehicle depreciation cost of $308 per month in the fourth quarter of 2010 is in line with our expectations for 2011, although it represented an increase from the 2009 level of $274 per month. The increase in per vehicle depreciation cost resulted from a decrease in gains on disposition of risk vehicles of $16.3 million compared to the prior year period. This decrease was attributable to approximately 11,000 fewer vehicles disposed of on a year-over-year basis, and gains on sales of risk vehicles normalizing in the fourth quarter of 2010 from the record levels in 2009. Vehicle utilization for the fourth quarter of 2010 was 79.7 percent, up from 78.8 percent during last year's fourth quarter.

In spite of an increase in rental revenues for the fourth quarter of 2010, direct vehicle and operating expenses and selling, general and administrative expenses declined on a total dollar basis. Additionally, these expenses declined to 61.5 percent of revenues for the fourth quarter of 2010, compared to 65.1 percent of revenues in the fourth quarter of 2009. The decrease in expenses was primarily a result of lower vehicle-related insurance costs, in addition to the ongoing benefits of company-wide cost reduction efforts and productivity initiatives.

Full Year Results

For the year ended December 31, 2010, net income was $131.2 million, or $4.34 per diluted share, compared to $45 million or $1.88 per diluted share for the year ended December 31, 2009, in spite of an increase in diluted shares outstanding of approximately 25 percent as a result of the company's equity offering in November 2009. Net income in 2010 included a net positive impact of $0.54 per diluted share related to favorable changes in fair value of derivatives and long-lived asset impairments, compared to a net positive impact on income of $0.65 per diluted share in 2009.

The company noted that net income for the full year of 2010 was negatively impacted by approximately $13.2 million of after-tax merger-related expenses, or $0.44 per diluted share, while no such charges were incurred in 2009. The company also noted that rental revenue was flat on a year-over-year basis, driven by a 90 basis point decrease in transaction days that was offset by a 90 basis point increase in revenue per day.

Non-GAAP net income for the year ended December 31, 2010 was $115.0 million, or $3.80 per diluted share, compared to non-GAAP net income of $29.6 million, or $1.24 per diluted share for the same period in 2009. Non-GAAP net income excludes the (increase) decrease in fair value of derivatives and non-cash charges related to the impairment of long-lived assets, net of related tax impact. Excluding the impact of merger-related expenses mentioned above, non-GAAP net income for the full year of 2010 would have been $4.24 per diluted share, compared to $1.24 per diluted share in the prior year period.

Corporate Adjusted EBITDA for the year ended December 31, 2010, excluding the merger-related expenses mentioned above, was $258.3 million, an increase of approximately 160 percent, or $158.9 million, compared to the full year of 2009.

"For Dollar Thrifty, 2010 was a transition year, a year in which we moved effectively from a turnaround strategy to one focused on maximizing profitability. We capitalized on our long-established value brands, numerous profit enhancement initiatives and our significantly improved financial strength. I am pleased to report the Company successfully navigated the transition, resulting in the most profitable year in the company's history by a wide margin. I am even more pleased to report that we also improved our customer satisfaction scores, evidencing our balancing of long-term and short-term objectives," according to Thompson.

Liquidity and Capital Resources

During 2010, the company further strengthened its liquidity by adding $950 million in new fleet financing capacity, while further reducing outstanding debt levels by more than $300 million from year-end 2009 levels and approximately $1.1 billion from year-end 2008 levels.

As of December 31, 2010, the company had $563 million in cash and cash equivalents, and an additional $277 million in restricted cash and investments primarily available for the purchase of vehicles and/or repayment of vehicle financing obligations. The company's tangible net worth at December 31, 2010 was $515 million.

FTC Update

As previously reported, the company and Avis Budget Group, Inc. ("Avis Budget") have been cooperating to pursue antitrust regulatory clearance of a potential acquisition of the company's common stock by Avis Budget.

The company believes substantial progress has been made in the discussions with the United States Federal Trade Commission (the "FTC"); nevertheless, the FTC's position with respect to the competitive issues remains uncertain. The company submitted its certification of substantial compliance with the Second Request on February 23, 2011. In addition, Avis Budget submitted its certification of substantial compliance with the Second Request on February 4, 2011. Based on the timing of these submissions, the company expects to have greater clarity around the FTC's official position in the near future.

"The FTC is performing an extensive review as it appropriately considers the proposed transaction. The process began in May of 2010, and we are eager to bring clarity to this matter for our shareholders and employees," according to Thompson.

2011 Outlook

The company noted that it expects further recovery in travel activity as the economy continues to improve. The company expects the revenue per day environment to be competitive, resulting in flat pricing for 2011 compared to 2010. The company also disclosed that its guidance is based on a slightly less robust used vehicle market in 2011 as compared to 2010. The company noted that Corporate Adjusted EBITDA in 2010 benefitted from approximately $63 million in gains on disposition of risk vehicles that were partially a consequence of the rapid recovery in the used vehicle market from historic lows in 2009, and the company's guidance reflects a depreciation and residual value environment more in line with historical norms.

Based on the above expectations and the additional information outlined below, the company is targeting Corporate Adjusted EBITDA for the full year of 2011 to be within a range of $175 million to $200 million. This estimate does not reflect the impact of merger-related expenses in 2011.

The company provided the following additional information with respect to its full year guidance:

Vehicle rental revenues are projected to be up 2 - 4 percent compared to 2010, with such increases occurring primarily in the second through fourth quarters. This revenue growth is projected to result primarily from low single-digit increases in transaction days, driven by a rebound in travel demand as a result of a slightly improving economy.

Vehicle depreciation costs for the full year of 2011 are expected to be within the company's previously announced range of $300 to $310 per vehicle per month.

Interest expense is expected to decline significantly in 2011 compared to 2010, primarily as a result of a reduction in the overall level of vehicle debt outstanding, combined with lower overall interest cost on the company's recently completed fleet financing facilities as compared to the fixed rates paid on maturing fleet debt facilities.

"We are excited about the company's competitive position going into 2011. We have two long-established value brands, broad distribution of our products, competitive operating costs, significant and growing world-wide franchisee base business, minimal corporate leverage combined with significant tangible net worth, and, lastly and most importantly, a very talented workforce. Consistent with 2010, our primary objective will be to maximize return on assets for our shareholders, and we will consider all potential options to achieve that objective," said Thompson.

To view the original press release, click here.

More Rental Operations

Green Motion And U-Save Open Rental Operations In Guatemala

The brands will open their first rental car outlets in the country at La Aurora International Airport in Guatemala City.

Read More →

U.S. Business Travel Drives $623 Billion+ in Economic Impact as Spending Reaches $538 Billion

The data also underscores the industry’s strong multiplier effect across the U.S. economy, revealing that each dollar invested in business travel in 2024 generated $1.16 in GDP.

Read More →

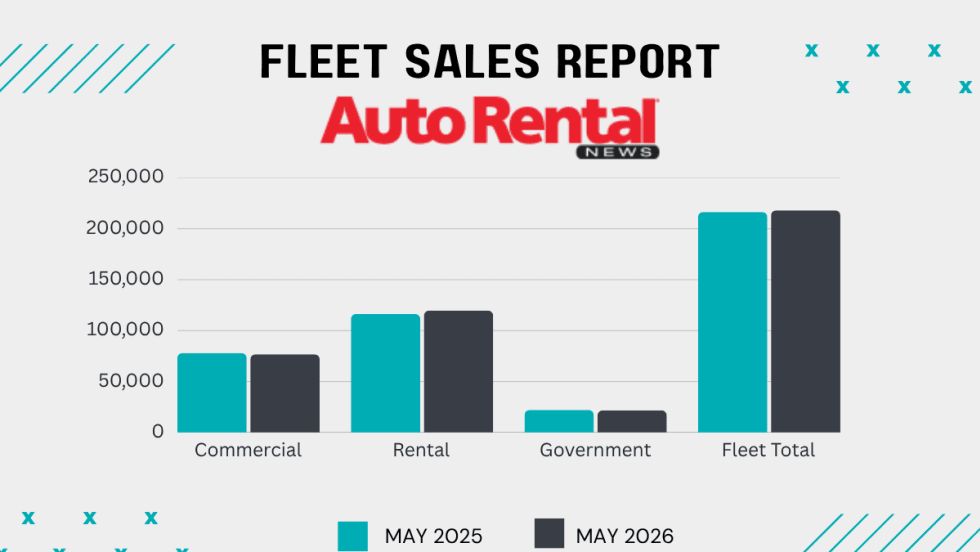

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Grow Your Rental Business Beyond Cars

Rental fleet operations are facing numerous evolving challenges and opportunities from AI technology to rate and revenue management, to customer service and business growth.

Read More →

Using AI to Create Clarity, Not Conflict, in Rental Car Damage

Rental companies still need people, policy, judgment, and thoughtful implementation, with operators remaining in control of the customer experience.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Southwest Airlines Selects CarTrawler For Its Car Rental Booking Platform

The platform is designed to allow customers to compare and book rental vehicles more easily during the travel booking process.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

Government Affairs Executive Wins Leading Rental Car Industry Award

Robert Muhs started in the car rental industry with Avis Budget Group two years before the first International Car Rental Show.

Read More →

Green Motion Expands Its African Presence with Mozambique Launch

This new rental car outlet reflects the growing demand for reliable transportation and the emphasis on sustainable travel across the continent.

Read More →