![[|CREDIT|]](https://fleetimages.bobitstudios.com/upload/auto-rental-news/content/article/2021-12/610px_car_driving-__-720x516-s.png)

Clear differentiators between car rentals, car subscriptions, and car sharing are disappearing. We previously explored the opportunity for car rental companies to make a small pivot to embrace carsharing; in the article below we explore the current state and opportunities in the growing market of car subscription services.

The Current State of the Car Subscription Markets

Offering car subscription services as an alternative to car ownership is gaining traction across the globe. What started in the US has since made its way to Europe and now also to Africa. Car subscriptions offered by OEMs have been around for multiple years but recently took off with increased customer demand and invested capital. This follows a general trend towards subscription products and services, with car subscription services often being referred to as “Netflix for cars”.

Car subscriptions are seen as an attractive alternative to car financing, cash payment or leasing. Experts predict that car subscription services could make up to 40% of new car sales within the next 10 years. A survey by McKinsey also comes to the conclusion that car subscriptions from major OEMs are growing at a fast pace, as we can already see happening in the market. BCG is more conservative and forecasts a revenue potential of $30 to $40 billion dollars by 2030 in Europe and the US. This would be equivalent to approximately 15% of new car sales or 5-6 million active subscriptions.

The Lines Between Car Rentals and Car Subscriptions Are Already Starting to Blur

There are a diverse group of stakeholders within the car subscription space. Some car rental services have started to offer their vehicles in dense urban areas as a free-floating car sharing service, while also launching car subscription services in less dense areas. Sixt and Hertz are equipping their fleets with state-of-the-art IoT devices to offer car sharing services for B2C and B2B customers.

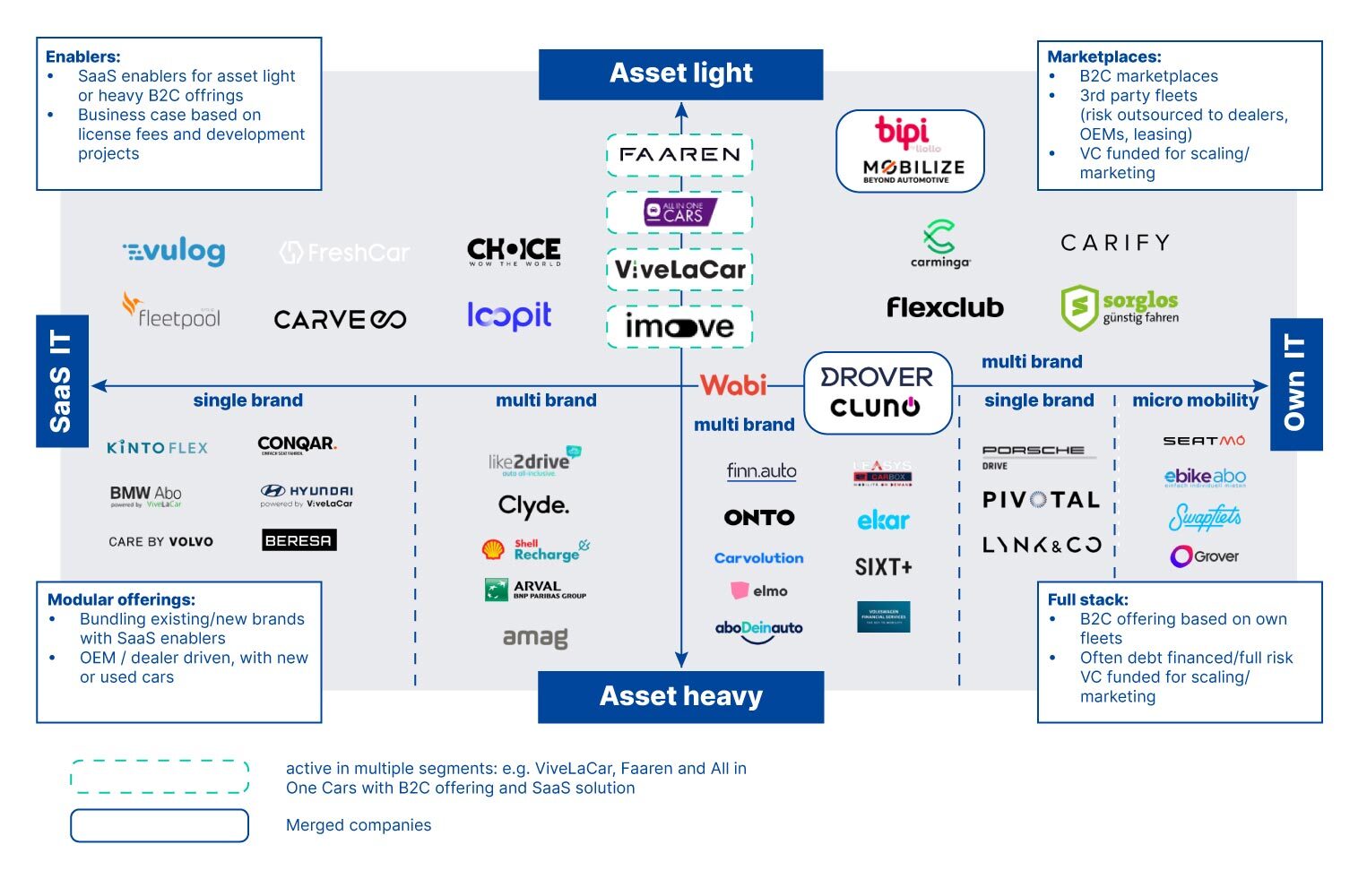

Automotive OEMs are starting their own services to build up direct relationships to customers, such as Care by Volvo - their car subscription program - which was launched in 2018. Dealer groups are also using their local brand when offering subscription services based on technology provided by Faaren, ViveLaCar, and others.

In addition, start-ups and platforms are trying to disrupt the car subscription space with unique offerings, such as Cluno, Drover, and Carvolution who build dedicated fleets for car subscriptions linked to a fully digital user journey.

Meanwhile, free-floating car sharing services like WeShare from Volkswagen, CityBee or Wible in Spain see the opportunity to increase the utilization of their fleets by offering multi-day or weekly packages, bringing their services closer to car rental services. Other car sharing services are updating their pricing and maximum rental durations to move into the turf of traditional rental companies.

Figure 1: Players in the growing car subscription space

Why Are Customers Option for Car Subscription Services?

Car subscriptions are built for customer groups that are already used to shared mobility and that prefer access to car usage over ownership. Changing customer requirements and behaviors have accelerated the trend towards subscribing to goods and services, and not only to digital services and software.

Car subscription customers don’t have to pay high upfront fees and are also not tied into multi-year contracts. The residual value risk linked to the ownership of a vehicle is managed by the fleet owner not the vehicle user. The flexibility and reduced risk may also motivate customers to try out new brands or electric vehicles.

Additionally, a growing sub-segment of car subscription customers are B2B drivers with the urgent need of a car or light commercial vehicle for transportation or mobility services. Drivers for on-demand economy platforms like Uber, Lyft, Free Now in the mobility sector and DoorDash or Amazon are often looking for flexible access to cars without high upfront costs. The challenges for fleet operators are that the usage patterns are different (more miles, higher risk for damages) and that the credit score of the B2B driver base could be challenging with risks of outstanding payments for the fleet owners.

What’s in it for Car Rental Companies?

From a fleet operator perspective, it is wise to offer multiple pay-per-use offerings with the same fleet. As usage and peak demand patterns for car sharing, car rental, and car subscriptions differ, offering a range of services with a single fleet would maximize the utilization of the vehicles, leading to more revenue and profits.

This multi-use setup is only possible with a fully connected fleet and the capability to track and analyze the collected fleet data for ideal redistribution between the different modes. However, it is noteworthy that the feasibility and success of combining pay-per-use offerings depends on the location, ambition, and expertise of the fleet owners. Core competencies along the value chain from vehicle sourcing to remarketing are required to build a strong offering.

In a nutshell

Car subscriptions are here to stay and have a very promising future. This presents rental fleets with opportunities to tap into new revenue streams. These opportunities could be increased by venturing into multiple verticals with a connected fleet; talk to INVERS to learn how.

This article is written by industry expert and INVERS guest writer Augustin Friedel.

media brand

media brand