How to Explain Car Rental to Banks and Investors

Based on 18 years of experience raising money for major car rental companies, investment banker Scott White gives eight good reasons to convince banks their money will be safe, and three compelling arguments to attract equity investors.

It's important to make the distinction that car rental is driven by travel trends, not necessarily the larger auto industry.

Photo: Canva

As you know, the car rental industry faces biases and misunderstandings. Through hard experience and many hours of talking to skeptical and smart investors, I can attest to the many knee-jerk biases held against car rental. As active business and leisure travelers, most investors have had some negative experience renting a car and have drawn broad judgments about the industry based on random fact patterns.

My purpose here is to reveal the arguments and explanations I've used successfully with large global banks, leading private equity firms, institutional investors and Wall Street analysts in car rental's biggest mergers and acquisitions and financing deals.

Some versions of the arguments below can be used by local operators with their banks and equity investors. As car rental people, you know all this already. But what follows is the framing of the issues I've found to be effective. With banks, I stress why their money will be safe. With equity investors, I stress why their money will grow.

Addressing the Misunderstandings

I generally start by asking bankers to "set aside what you think you know about car rental and your own personal experiences renting cars." I strive to grab their attention and let them know right away that I'm going to take the offensive, tell them stuff they don't know and refrain from apologizing for the industry. Make no mistake; I say car rental is a great business.

Here are the most common biases and misunderstandings I've encountered and how I've addressed them:

"FEAR OF EXPOSURE TO 'AUTO.'"

The last 30 years of automaker troubles have made bankers and investors generally want to stay away from anything having to do with "auto." But car rental revenue, first and foremost, is driven by travel levels. And since travel spending has mostly grown steadily for decades, so have car rental revenues.

A related concern has been fear of automaker bankruptcies. For several years, that was an active, though theoretical, discussion. Recently, as you know, it became real. And it played out for car rental just as car rental people said it would; namely, manufacturers honored their repurchase agreements and continued to sell to car rental fleets. Car rental is and remains an important customer for automakers.

Car rental is really a kind of finance business and rental service combined. It has nothing to do with manufacturing, unions, or foreign competition. In fact, I "go big" early in the discussion. Car rental is an essential service and a key part of the transportation network. It enjoys a "utility-like quality" of predictable and recurring revenues. You can't outsource it to a developing country, nor disintermediate it with the Internet. It is here to stay.

"EBITDA is huge!"

EBITDA, or earnings before interest, taxes, depreciation and amortization, is what companies use to pay debt service. Unfortunately, you don't get to service non-fleet debt with gross EBITDA. You first have to deduct the costs of the fleet. Vehicle depreciation and interest is "cost of goods sold" for a car rental company. What's left is often called Adjusted EBITDA or Corporate EBITDA. It's the cash flow that can be spent at management's discretion after fleet costs have been paid. Finally, depreciation of the fleet is a cash expense, not a non-cash expense as it is in a business with longer-lived assets, so you don't add it back when determining cash flow.

"There's too much exposure to used car prices."

This bias is based on the fear that car rental is nothing but a play on the used car market and that such risk is virtually unmanageable. I go right at it: the used car market is huge, efficient, liquid and the same for everybody. Car rental companies monitor their monthly depreciation charges constantly and make changes as needed. In fact, major car rental companies, over time, average a gain on sale of a few hundred dollars per risk car. What's more, they are all impacted equally and can instantly adjust by tweaking depreciation schedules, raising prices or cutting costs.

"Car rental is too capital intensive."

Oh really? Who says? In fact, one can argue it's not capital intensive at all-the fleet is financed largely by debt, and non-fleet capital expenditure (capex) is relatively small. A dollar of debt is matched against more than a dollar of car and cash. I explain that it's hard to go bankrupt, so long as you don't incur non-vehicle debt. Too much non-vehicle debt combined with a downturn in demand or pricing has led to a couple of bankruptcies.

On the other hand, Dollar Thrifty demonstrated the terrific credit quality of a properly capitalized car rental company during the recent downturn. You shrink fleet and staffing levels so that diminished revenue can continue to cover costs. Car rental companies enjoy a proven ability to de-fleet in a downturn. They benefit from a "highly variable cost structure;" that is, it's relatively straightforward to match costs to revenue.

"There's no free cash flow because you always have to plow cash back into the fleet."

Don't worry: free cash flow equals net income over time. This is stating the obvious to someone who's taken accounting. (After all, net income is what's left over after all the bills are paid). It's sort of like a first principle. But I find I need to point it out because financial models of car rental companies often lead the modelers to conclude that there's no free cash flow (which, if true, would make bankers and owners nervous). In fact, properly modeled and demonstrated by decades of performance, car rental companies generally produce net income margins of 5 to 10%. Fleet growth can be accommodated by new debt and a growing Owners' Equity account.

"Car rental is a 'commodity service' that is too competitive."

We all know service levels matter, and brands have distinct positioning that plays an important role in pricing. In fact, well over 90%of market share in the U.S. is in the hands of the eight well-known brands. The stability of these brands and market shares over decades is remarkable. On the other hand, it's not as if nothing ever changes, or you can't invent a better mouse trap. But compared to many industries, car rental exudes stability. Market shares do move around, but the established brands attract the business.

"Pricing is not rational."

That is to say, "On any given day, in any given market, on any given car class, prices among competitors can be all over the place." As we know, that is true. But I've looked at decades of detailed pricing data by brand, and long-term price trends among the brands are consistent with the brand images. What causes spot discrepancies? Roughly speaking, half the pricing decision on any given rental is based on competitive factors, and half on the need to "move the metal."

"What about insurance exposure?"

What about it? There's no meaningful insurance exposure so long as car rental companies follow best practices regarding asset management. That is, be careful about who can rent one of your cars and know where your cars are. But don't car rental companies give away the rental so that they can make money by selling insurance? I bet we've all heard that one. Actually, insurance sales are probably best thought of as extra price. Companies manage the insurance issues in various ways, but car rental is not an insurance play.

The Equity Story

That takes care of the banks. But why would equity investors want to own a car rental company? Owning a car rental company works for all the reasons discussed above, and for the "upside" laid out below. Here's why your money should grow if you invest in car rental.

Financial Leverage

This means you can use lots of debt, which is cheaper than equity. The amount of equity needed to support a car rental company is less than you'd think because cars can be largely debt financed. The big opportunity is leverage. That means that small changes in the performance of the business can have big impacts on the value of the equity. In part, that's because high debt levels magnify changes to the equity (a good analogy here would be to a home loan and the home's equity; a rise in the value of the home adds wholly to the equity). This is referred to as financial leverage.

Operating Leverage

The other component is operating leverage, meaning performance that creates earnings above relatively fixed costs accrues disproportionately to the owner (as opposed to other stakeholders, such as employees, debt holders, automakers or landlords). For example, incremental pricing drops to the bottom line. There's little offsetting cost (although don't forget that raising prices without reference to the competition can crimp demand). Benefits from operating leverage are why you always want to push pricing as hard as you can.

Another example is that better technology facilitates charging the highest price for every rental (yield management). Also, better technology lowers costs, especially fleet management and reservation delivery. Fleet is typically 60 percent of cost structure, so even small improvements in fleet management produce big impacts on earnings. Leapfrog technology (do a lot more for a lot less) can allow car rental companies to lower costs and pocket the difference in earnings.

Ever-Rising Travel Spending

Finally, perhaps the strongest argument for putting money into car rental companies, in the form of either debt or equity, is the long-term, secular trend (that is, over and above business cycles) of more and more travel. The "democratization of the skies," discount airlines, low-cost hotels, GPS and rising global affluence all cause the travel sector to grow constantly. While we've lived through some recent contra-experiences, the broader truth is that travel spending almost never declines. As people around the world increasingly get on planes, they increasingly rent cars, ensuring the return of capital to banks and bondholders and an equity account for investors.

As you may have noticed by now, I'm a big believer in the business of car rental. I just keep talking about its fabulous attributes until the skeptical, smart people who control large amounts of money say "yes" to me or ask me to stop. I've brought billions of dollars into the industry deploying the points above. I hope you can make them work for you.

Photo: Scott White

About the Author

Scott White is senior managing director and head of investment banking at C.L. King & Associates, a New York-based investment bank.

He's been involved with the car rental industry since 1994 when, as a young investment banker, he executed the IPO of Sandy Miller's company, Team Rental Group. In the late '90s, he oversaw the acquisitions of Budget Rent a Car, Ryder Truck Rental, Premier Car Rental and Cruise America as executive vice president of corporate development and investor relations at Budget Group, the successor to Team Rental.

In the early 2000s, back in banking, he advised Avis on the acquisition of Budget and on the sale of PHH Europe. In 2005, he advised a consortium of large private equity firms on the cover bid in the Hertz auction. Over the years, he's also worked on many capital raising deals for car rental companies. Finally, he's performed due diligence related to live deal activity on all the major car rental companies in the world, including Enterprise, Hertz, Avis, Budget, National, Alamo, Dollar, Thrifty, Avis Europe, Europcar, and Sixt.

More Rental Operations

DriveItAway, Free2move Plan Shared Fleet Program for Independent Rental Fleet Operators

Vehicles would be placed with participating rental operations to support car renter demand and provide additional fleet capacity.

Read More →

Green Motion And U-Save Open Rental Operations In Guatemala

The brands will open their first rental car outlets in the country at La Aurora International Airport in Guatemala City.

Read More →

U.S. Business Travel Drives $623 Billion+ in Economic Impact as Spending Reaches $538 Billion

The data also underscores the industry’s strong multiplier effect across the U.S. economy, revealing that each dollar invested in business travel in 2024 generated $1.16 in GDP.

Read More →

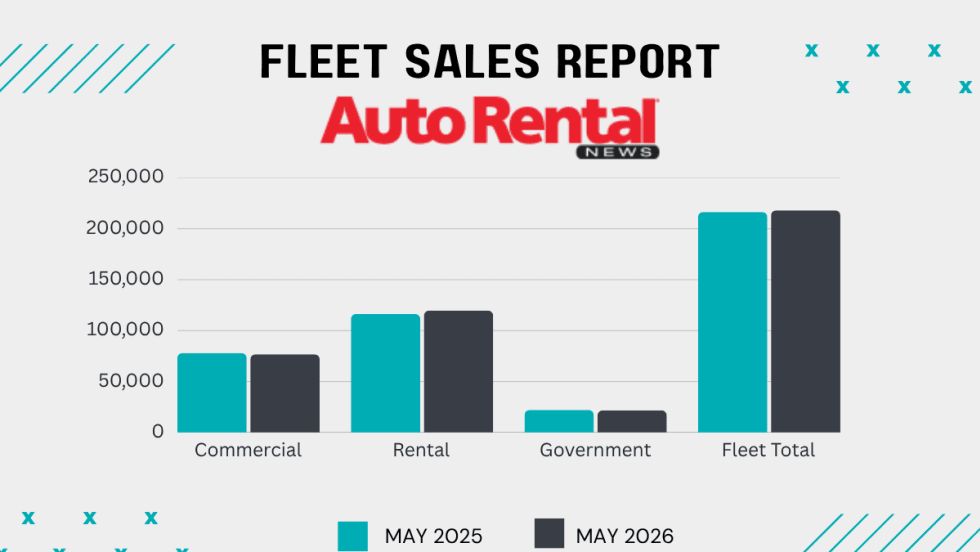

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Grow Your Rental Business Beyond Cars

Rental fleet operations are facing numerous evolving challenges and opportunities from AI technology to rate and revenue management, to customer service and business growth.

Read More →

Using AI to Create Clarity, Not Conflict, in Rental Car Damage

Rental companies still need people, policy, judgment, and thoughtful implementation, with operators remaining in control of the customer experience.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Southwest Airlines Selects CarTrawler For Its Car Rental Booking Platform

The platform is designed to allow customers to compare and book rental vehicles more easily during the travel booking process.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

Government Affairs Executive Wins Leading Rental Car Industry Award

Robert Muhs started in the car rental industry with Avis Budget Group two years before the first International Car Rental Show.

Read More →