Rental Companies Favorably Weather Used-Car Trends

Manufacturer retail ‘employee-pricing’ promotions caused a downturn in the used-car market, but car rental companies held cars and weathered the worst of it. Overall, rental companies say they had a positive year in 2005.

Calendar year 2005 was certainly a challenging year to remarket cars, especially since the manufacturer “employee- discount” programs made buying new vehicles more economically feasible than buying used. Car rental companies were nervous during the summer, especially since 2005-model year repurchase programs and allocations had moved them more into risk units than they had in recent years.

Two factors helped the car rental industry record an above-average year on the risk remarketing front. The first, car rental companies buy a lot of subcompact and compact cars, which were more in demand on used-car lots in 2005 than large cars and SUVs. The second factor is that car rental companies have the flexibility to hold cars longer, or move them to better geographic markets, to ride out rough spots and obtain better residuals.

According to data from ADESA Corp., rental risk mileage spiked from about 28,000 miles in the spring of 2005 to about 32,000 in the summer and fall, signifying that car rental companies were holding these cars longer. In 2004, risk car mileage averaged about 30,000 miles consistently throughout the year.

Resale prices on used-rental risk units went through a roller-coaster ride in 2005, according to ADESA data. Average prices shot up early in the year to about $13,000. The market low was about $10,500 in the summer, during the peak of the employee sales promotions.

How the Majors Fared

As the largest buyer of risk units in the world, St. Louis-based Enterprise Rent-A-Car provides an important gauge for the state of rental risk remarketing. Mark Whalen, assistant vice president of remarketing research/analysis for Enterprise, says that the company had a neutral year (neither positive nor negative). “Overall the market was flat to slightly down in 2005,” he said. “Demand firmed somewhat in the month of October as the effects of reduced new-car inventories and the recent hurricanes were felt in the used market.”

Dollar Thrifty Automotive Group Inc., (DTAG) in Tulsa, Okla., had a more upbeat tale to tell, says Mario Nargi, vice president of fleet services. “The market was very strong in 2005,” he said. “Although we were very optimistic going into the year, both demand and pricing for used rental vehicles exceeded our expectations. Our primary supplier, DaimlerChrysler, had a lineup of vehicles that helped us attain high residuals. In the final months of 2005, demand for our small, mid-size, and full-size units remained solid.”

Automotive Fleet Resources, a supplier of financing and remarketing support to car rental independents and franchisees based in Memphis, Tenn., also reports positive results in the market, says Bill Lanier, managing partner. The company had its best sales months ever during March, April, May, and June 2005.

“Beginning in June, sales of small cars were strong, whereas larger vehicles, in particular SUVs, were extremely soft due in part to higher gas prices during the summer and the manufacturers offering employee pricing on their 2005 new-vehicle inventory,” Lanier says. “Resale of used rental units has followed the same pattern. At factory sales you saw small cars bringing clean wholesale book value and larger vehicles between rough and average wholesale.”

As mentioned previously, auto manufacturers have reduced allocations of repurchase units and urged large and small rental operators to acquire more risk units. This trend should continue into 2006, says Steve Leach, president of Burnsville, Minn.-based MarketWise. Along with this change, the manufacturers are charging higher prices for repurchase units in 2006, prompting car rental companies to raise rental rates. However, these increased rental rates may not stick, Leach says.

The Role Gas Prices Played

Spiking gasoline prices impacted both the new- and used-vehicle markets in 2005. Manufacturers saw fairly steep declines in large SUV retail sales and other light-truck categories, while smaller car sales surged. Similar trends prevailed in the used-car retail sales market.

Car rental companies tend to fleet-up with small to mid-size cars. The domestic manufacturers sell off inventory to rental companies and have been much more focused on the light-truck side of the business in recent years. Car renters also tend to like smaller cars because they offer the best value in terms of rental rates.

Some car rental companies have complained over the last decade about the lack of product availability from the manufacturers, especially with popular SUV models. In 2005, it turned out to be much better to have smaller cars than large SUVs, when it came time to remarket used vehicles. “Higher fuel prices have clearly played a role in the market for all used vehicles,” Enterprise’s Whalen says. “The recent higher prices are having a negative effect on large SUVs. If fuel prices continue to moderate, it will be interesting to see if demand for large SUVs will rebound. The early sell-down of 2005-MY inventory and the recent hurricanes have also created ripples in the market place.” “Gasoline prices have really hurt the SUV market,” Lanier says. “I looked up a 2004 Expedition for a customer recently and found that it had lost $6,000 dollars in value since June, according to Black Book.”

What About 2006?

With all its remarketing challenges, 2005 drew to a successful conclusion, but what about 2006? Companies interviewed for this article have a mostly positive outlook.

“Overall, we expect to see market conditions similar to the first half of 2005,” Whalen says. “Demand for used passenger vehicles is expected to remain healthy, and SUVs may remain under pressure. Fuel prices will continue to play a role in the performance of both segments.”

DTAG has a strong forecast for the first months of 2006. “We believe that the conditions in the used-car arena are such that we will continue to see solid residuals and demand levels for our used rental vehicles in 2006,” Nargi says.

“I think the first quarter of 2006 will continue in this pattern, since there is a real shortage of small cars in the market,” Lanier says. “Even at factory sales it is unusual to see any small cars with mileage above 10,000-12,000. They are giving away Explorers and Trailblazers.”

Focus on Basics and Integration

There were no revolutionary changes in rental risk remarketing in 2005, just a focus on basics and continued integration of multiple channels, including Internet sales. Car rental companies are trying out all sorts of Internet sales options, including their own Web sites and offerings from auction chains, other Internet-based channels, and specialized remarketing suppliers.

DTAG has had success trying a multi-faceted approach, with emphasis on the Internet. “From a process standpoint, the Internet has been a big factor in making our auction inventory available to a much broader dealership and wholesaler audience,” Nargi says. “We have put a lot of effort into this channel and are working with our auction partners to make sure that we get full-time, 24/7 exposure to our sales inventory.”

DTAG, through its Thrifty Car Sales division, has harnessed the power of retail car sales in the past few years. “On the Thrifty Car Sales side of our business, our franchisees continue to grow their businesses both at their current locations and through opening of additional sites,” Nargi says. “The network of franchised locations sources vehicles from our rental fleet and other avenues. Thrifty Car Sales dealers are given an advance look at rental vehicles before they are grounded for sale. Currently, Thrifty Car Sales franchisees operate 38 locations in 17 states.”

Automotive Fleet Resources has had similar experiences with its stable of independent and franchisee clients. “We continue to utilize our Web site and auctions,” Lanier says. “The large majority of our rental customers are now in the retail sales business and doing quite well in their local communities. I think everyone is utilizing the Internet for retail sales and mostly auctions for wholesale. I have not seen anything really new or innovative in selling vehicles.”

More Remarketing

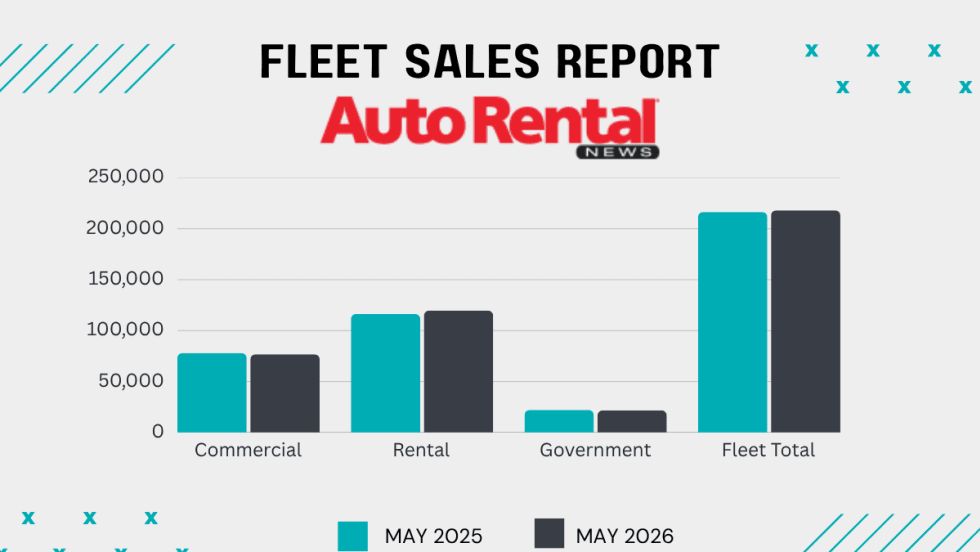

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

Surprice Opens Two Rental Branches In Japan

The launch highlights the global car rental operation’s growing presence in Asia.

Read More →

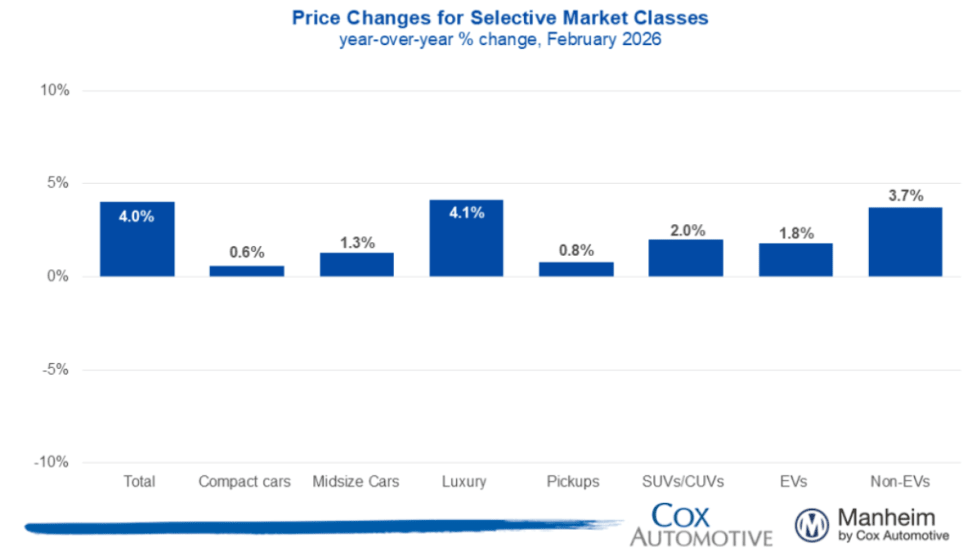

Wholesale Used Vehicle Prices Up In February

Solid demand at Manheim auctions with higher sales conversion rates indicate an appetite from dealers to buy.

Read More →

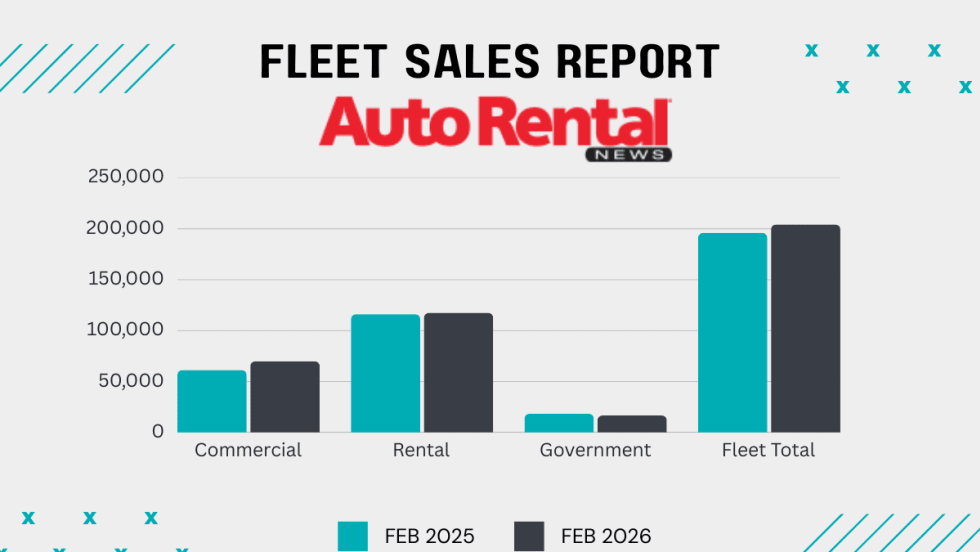

Rental Fleet Sales Slow In February Ending A Strong Streak

Commercial fleets posted the most gains, sustaining increases in monthly and year-to-date fleet sales

Read More →

Avis Budget Group Reports Near $1 Billion Loss Tied To 2025 EV Fleet Write-Down

Following Hertz, the company is the second global car rental conglomerate to sustain sizable losses due to lower customer demand and usage of electric rental cars.

Read More →

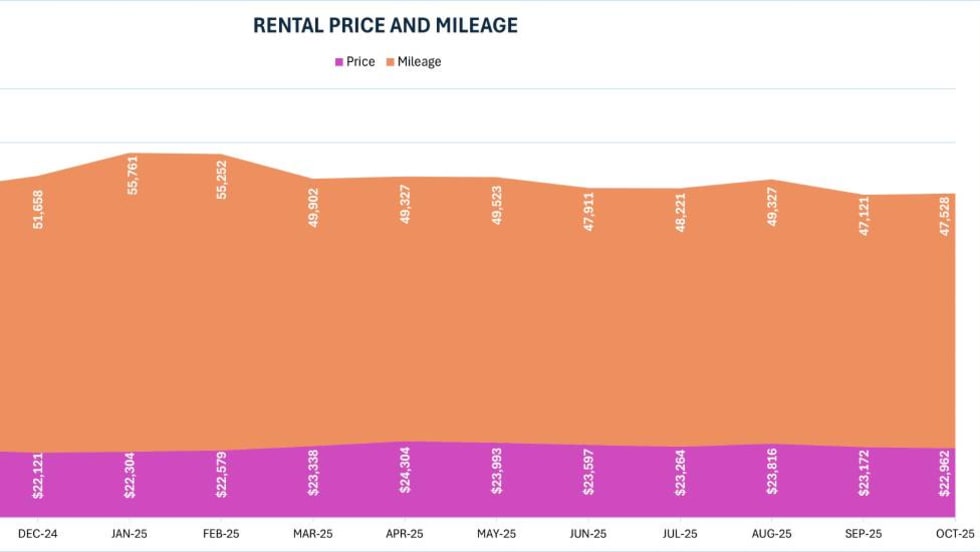

2025 Rental Vehicle Remarketing Summary And Outlook

The year brought modest and flatter results across wholesale values, total off-rental supply, and rental risk units.

Read More →

Auctions Record Highest Vehicle Sales Since 2019

2025 figures show a steady recovery in wholesale vehicle activity this decade.

Read More →

DriveItAway Holdings, Free2move Launch Operations In Nine Cities

The co-branded program with Stellantis’ mobility division scales up leasing and financing options nationwide with more cities to come online in 2026.

Read More →