Dollar Thrifty Reports $42.3 Million Net Income in Q2

Total revenue flat due to planned reduction in leasing to franchises. Same-store revenue up 2.9 percent. Revenue gains for vehicle rentals partially offset by drop in rental days, though volume improving. Utilization up. Strong used-car market keeps vehicle depreciation costs in check.

Dollar Thrifty Automotive Group Inc. today reported results for the second quarter ended June 30, 2010. Net income for the 2010 second quarter was $42.3 million, compared to net income of $12.4 million in the year-ago period.

Non-GAAP net income for the 2010 second quarter was $38.0 million, compared to non-GAAP net income of $6.9 million, for the 2009 second quarter. Non-GAAP net income (loss) excludes the (increase) decrease in fair value of derivatives and the non-cash charges related to the impairment of long-lived assets, net of related tax impact.

The company reported corporate adjusted EBITDA for the second quarter of 2010 of $74.3 million, compared to $20.9 million in the second quarter of 2009. The company noted that it incurred merger-related expenses of $6.8 million during the quarter, negatively impacting reported results. Excluding these merger-related expenses, corporate adjusted EBITDA for the second quarter of 2010 was $81.1 million.

"The company's ongoing efforts in the areas of revenue management, expense control and fleet management continue to reap significant benefits, as demonstrated by our sixth consecutive quarter of year-over-year double-digit growth in corporate adjusted EBITDA," said Scott L. Thompson, president and chief executive officer. "Our day-to-day focus continues to be on improving the company's return on assets while maximizing our cash flow. I am pleased to report that we are on track to make 2010 the most profitable year in the history of the company."

On a same-store basis, rental revenues for locations that were open during the second quarter of both 2010 and 2009 were up 2.9 percent compared to last year's second quarter. For the quarter ended June 30, 2010, Dollar Thrifty's total revenue was $396.2 million, as compared to $399.6 million for the comparable 2009 period. The decline in total revenue was primarily driven by a decline in vehicle leasing revenue, resulting from a planned reduction in vehicles leased to franchisees. Vehicle rental revenue for the quarter was consistent on a year-over-year basis as an 80 basis point improvement in rate per day offset a 50 basis point decline in rental days. The second quarter 2010 average fleet was down 0.8 percent compared to the second quarter of 2009, while the ending fleet was up 0.9 percent from the second quarter of 2009.

"We are pleased with the results for the quarter, having realized increases in transaction days and utilization on a same-store basis, while continuing to realize pricing improvement in a more challenging and competitive pricing environment. Based on our solid second quarter results combined with our current reservation book and our outlook for the economy, we expect revenue growth going forward," said Thompson.

Vehicle depreciation per unit for the second quarter of 2010 totaled $193 per month as the company continued to benefit from the overall strength of the used vehicle market, in addition to changes the company made in 2009 to its fleet planning and remarketing operations that were designed to lower fleet depreciation costs per unit and mitigate enterprise risk. Vehicle utilization was 80.8 percent, up 20 basis points from last year's second quarter.

Operating expenses (direct vehicle and operating expenses and selling, general and administrative expenses) were higher in the second quarter of 2010 compared to the same quarter in 2009 primarily as a result of $6.8 million of merger-related costs incurred, in addition to a $3 million increase in self insured vehicle liability reserves related to a vicarious liability claim that is currently under appeal by the company. These costs were partially offset by ongoing cost reduction efforts and cost efficiency initiatives. As a percentage of revenues, operating expenses totaled 62.7 percent of revenues in the second quarter of 2010, compared to 61.0 percent in the second quarter of 2009, primarily as a result of the cost increases noted above.

Interest expense, net of interest income, for the second quarter of 2010 declined $1.3 million on a year-over-year basis primarily as a result of approximately $300 million in net reduction in the debt outstanding for 2010 compared to 2009, partially offset by reduced interest income as the company deployed the excess cash balances on hand in 2009 to reduce indebtedness, and to reinvest in the rental fleet.

[PAGEBREAK]

Six Month Results

For the six months ended June 30, 2010, net income was $69.6 million, compared to net income of $3.5 million in the year-ago period.

Non-GAAP net income for the six months ended June 30, 2010 was $61.0 million, compared to non-GAAP net loss of $4.9 million, for the same period in 2009. Non-GAAP net income (loss) excludes the (increase) decrease in fair value of derivatives and the non-cash charges related to the impairment of long-lived assets, net of related tax impact.

The company reported corporate adjusted EBITDA for the six months ended June 30, 2010 of $123.7 million, compared to $18.5 million for the six months ended June 30, 2009. The company noted that it incurred merger-related expenses of $8.5 million during the first half of 2010, negatively impacting reported results. Excluding these merger-related expenses, corporate adjusted EBITDA for the six months ended June 30, 2010 was $132.2 million.

Liquidity and Capital Resources

As of June 30, 2010, Dollar Thrifty had $370 million in cash and cash equivalents and an additional $114 million in restricted cash and investments primarily available for the purchase of vehicles and/or repayment of vehicle financing obligations. The company's tangible net worth as of June 30, 2010 was $443 million.

During the quarter, the company repaid $200 million of maturing medium term notes utilizing a combination of restricted cash and borrowings under newly completed fleet financing facilities. As previously reported, the company completed a two-year $200 million variable funding note facility in April 2010 which was fully drawn upon issuance. In addition, during June, the company completed a three-year $300 million variable funding note facility that is currently undrawn, and will provide additional liquidity for repayment of the company's next scheduled debt maturity of $600 million of medium term notes that begin amortizing in December 2010.

2010 Outlook - Update

In addition to announcing results for the quarter, the company reaffirmed its previously announced guidance updates for 2010 for revenue, fleet costs and corporate adjusted EBITDA, as well as for fleet costs for 2011.

As previously announced, the company expects rental revenue growth in 2010 of 1 to 2 percent over 2009 as growth in the back half of 2010 is expected to more than offset the decline realized during the first half of the year.

The Dollar Thrifty noted that it sold approximately 32,500 risk vehicles during the first half of 2010 at a cumulative pre-tax gain of $53.2 million. The company also noted that it expects gains from vehicle dispositions to decline significantly during the second half of 2010, and as a result, expects its depreciation per unit per month to be within a range from $300 to $310 per unit per month during the third and fourth quarters of 2010. Based on results for the first half of 2010, combined with the fleet cost outlook for the third and fourth quarters, the company expects its full year 2010 fleet cost to be $245 to $255 per unit per month.

Based on the company's actual results through the second quarter and its outlook for revenue and fleet costs for the remainder of 2010, the company expects corporate adjusted EBITDA, excluding merger-related expenses, to be within a range of $200 million to $220 million for the full year of 2010. The company's 2009 corporate adjusted EBITDA was $99.4 million.

In addition, the company reaffirmed its expected fleet cost for 2011 to be within a range of $300 to $310 per unit per month. The company noted that the ongoing positive effects of changes made in its operations and fleet management, combined with solid macroeconomic factors in the used car market, are expected to impact fleet costs in 2011 and beyond.

More Rental Operations

DriveItAway, Free2move Plan Shared Fleet Program for Independent Rental Fleet Operators

Vehicles would be placed with participating rental operations to support car renter demand and provide additional fleet capacity.

Read More →

Stellantis Recalls 1.3 Million Jeep Vehicles Worldwide Over Fire Risk

Stellantis is recalling more than 1.3 million Jeep Wrangler and Gladiator models worldwide over a fire risk linked to power steering pump wiring.

Read More →

Green Motion And U-Save Open Rental Operations In Guatemala

The brands will open their first rental car outlets in the country at La Aurora International Airport in Guatemala City.

Read More →

U.S. Business Travel Drives $623 Billion+ in Economic Impact as Spending Reaches $538 Billion

The data also underscores the industry’s strong multiplier effect across the U.S. economy, revealing that each dollar invested in business travel in 2024 generated $1.16 in GDP.

Read More →

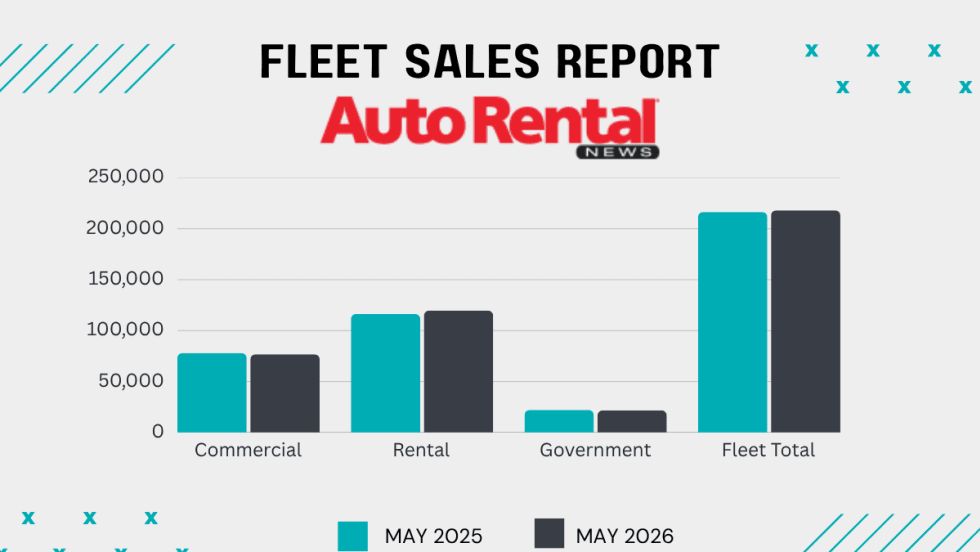

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Grow Your Rental Business Beyond Cars

Rental fleet operations are facing numerous evolving challenges and opportunities from AI technology to rate and revenue management, to customer service and business growth.

Read More →

Using AI to Create Clarity, Not Conflict, in Rental Car Damage

Rental companies still need people, policy, judgment, and thoughtful implementation, with operators remaining in control of the customer experience.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Southwest Airlines Selects CarTrawler For Its Car Rental Booking Platform

The platform is designed to allow customers to compare and book rental vehicles more easily during the travel booking process.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →