Debit Card Payment Processing Changes: Are You Taking Advantage?

New, federally mandated caps on debit transaction fees may benefit car rental companies accepting debit cards. However, be prepared for stricter IRS information reporting rules and the proliferation of payments via smartphone.

PHOTO: ©ISTOCKPHOTO.COM/PAGADESIGN

Recent changes in the payment processing industry will significantly impact — both positively and negatively — the acceptance of credit and debit cards. Car rental companies take notice.

These changes include a government regulatory program limiting charges by banks that issue debit cards. Another change includes an Internal Revenue Service (IRS) program requiring merchant account providers and merchant processors to report merchants’ total annual card volume to the IRS.

In addition to federal mandates, the payment card industry is sorting through the various ways to introduce and support smart (chip) cards and mobile payments in the United States. Smart cards are embedded with integrated circuits that use electrical connectors to transmit data to a merchant’s point-of-sale system.

If all this is not enough to make you dizzy, keep in mind that all the players participating in the electronic payments space — issuers, cardholders, merchant acquirers/processors, software providers and merchants — continue to be under attack by sophisticated hackers using advanced malware.

Durbin Amendment Lowers Fees

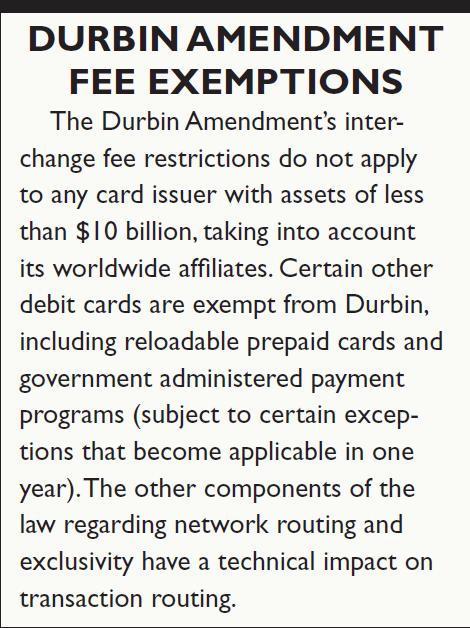

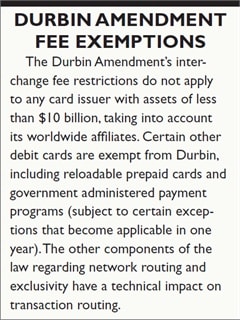

Under the new federal regulation stemming from the Durbin Amendment, as of Oct. 1, 2011, banks that issue credit cards are prohibited from charging or receiving an electronic debit (both signature and PIN) interchange fee greater than 21 cents plus 5 basis points (.0005%) times the amount of the transaction (see sidebar).

Previous to Durbin, fees varied by card used, type of debit routing and other factors. In a common example of a swiped Visa check card at a retail location, fees were as high as $2.10 on a $200 purchase, compared to the post-Durbin fee of $0.31. It’s easy to see how these new fee limits can put money back into car rental companies’ pockets.

However, due to the potential liability associated with debit card transactions, many car rental companies impose restrictions on the use of debit cards. As such, many car rental companies will not reap the benefits from these savings.

In the example of a $200 transaction that costs a merchant $0.31 in debit interchange fees post-Durbin, the same transaction would cost the merchant more than $4 if processed with a credit card. Is it time for some car rental companies to re-examine the no-debit policy?[PAGEBREAK]

IRS Applies Stricter Reporting Rules

The IRS has released final rules (T.D. 9496) relating to information reporting requirements, information reporting penalties, and backup withholding requirements for payment card and third-party network transactions.

These rules implement tax code Section 6050W and related changes enacted by the Housing Assistance Tax Act of 2008, and they require all merchant acquirers and payment processors to report payments in settlement of payment card and third-party network transactions for each calendar year.

Merchant acquirers and processors have been working together with the IRS to perform legal name and tax identification number (TIN) verification in order to minimize potential withholdings. Effective with the 2011 tax year, the IRS 6050W mandate requires all acquirers and payment processors to provide the following information on behalf of their merchants:

● Provide 1099-K forms recording gross payments made to the IRS and businesses accepting card-based payments.

● Verify that business corporate names and TINs match the IRS files.

● Send “Notice B” letters to customers as requested by the IRS to verify legal name and TINs.

The IRS recently announced that its original plan to require merchant acquirers to hold a percentage of payments for the 2011 tax year for businesses (as determined by the IRS) with TINs failing to match, will be postponed until the 2012 tax year.

Processors and merchant account providers will be most impacted by these mandates, as they have the responsibility of verifying information on file for their customers. As such, enhancements will largely be transparent to the car rental companies. However, businesses with mismatched information on file can expect to be contacted in an effort to acquire up-to-date information.

Paving the Way for Smartphone Payments

As previously mentioned, merchants — together with other payment industry stakeholders — must plan for the proliferation of smart (chip) cards and payments generated through mobile smartphones.

In August 2011, Visa announced a program to jump-start EMV (Europay, MasterCard and Visa) smart cards and mobile payments in the U.S.

Visa plans to accelerate the migration to smart-card technology in the U.S., and according to Visa, the adoption of dual-interface chip technology will help prepare the U.S. payment infrastructure for the arrival of near-field communication (NFC)-based mobile payments, or “contactless” payments, by building the necessary infrastructure to accept and process chip transactions.

Smart-card technology is expected to enhance payment security through the use of dynamic authentication. This type of security uses cryptography to create a unique, one-per-session authenticator that must be verified by the merchant’s point-of-sale system prior to receiving an approval on the transaction.

Visa’s plan also includes merchant incentives to upgrade to smart card-enabled terminals, requirements for processors to support the acceptance of smart cards and the introduction of U.S. liability shift policies on cardholder data compromises.

Specifically, Visa will waive Payment Card Industry Data Security Standard (PCI DSS) compliance validation requirements to encourage merchant investment in contact- and contactless-chip payment terminals.

Visa will also require that the acquirer processors ensure their systems support dynamic data acceptance (i.e., smart card/chip) and institute a domestic and cross-border counterfeit liability shift.

Implications for Car Rental

For merchants in the car rental industry, with its unique environment, some of these new regulations and technologies may not be as impactful.

Perhaps car rental merchants should be more concerned about what remains the same — namely the threat of fraud and data security breaches. Car rental merchants and their software systems must find ways to offload the transmission and storage of sensitive cardholder data by implementing point-to-point encryption and tokenization at the point of sale.

Roy Bricker is a payment industry veteran with more than 20 years’ experience in general management, product management and business development. He is the COO for Element Payment Services and has previously held management positions at Pay By Touch, Concord EFS (now First Data) and MasterCard.

Looking for other articles from our January/Feburary 2012 issue? Go to our magazine page here.

More Legal & Legislative

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

Government Affairs Executive Wins Leading Rental Car Industry Award

Robert Muhs started in the car rental industry with Avis Budget Group two years before the first International Car Rental Show.

Read More →

Using AI To Find Rental Car Damage

Angry car renters are storming social media, the mainstream media, and online ratings platforms to complain about charges they claim are either unfounded or excessive.

Read More →

Bandit Towing A Tough Road For Car Rental Companies

Operators often must spend far too much time and resources trying to recoup rental cars towed away and held hostage to outrageously high fees.

Read More →

Bandit Towing A Tough Road For Car Rental Companies

Operators often must spend far too much time and resources trying to recoup rental cars towed away and held hostage to outrageously high fees.

Read More →

ACRA: Spurring Car Rental Industry Success

The American Car Rental Association scored more access and influence in 2025 as it grows its services for car rental operators.

Read More →

AVOA Partners with AALA and NLC

The American Vehicle Owners Alliance (AVOA) recently announced its partnership with the American Automotive Leasing Association (AALA) and the National League of Cities (NLC).

Read More →

ACRA Takes Bold Strides On Capitol Hill

The American Car Rental Association’s annual legislative and lobbying event upped the face time with and access to members of Congress.

Read More →

Rental Car Leader Engages With Primary Industry Causes

Q&A Interview: Federal contracting, EV charging infrastructure, stolen vehicles, and policy advocacy drive an agenda for Carlos Bazan-Canabal that stretches beyond his car rental executive post.

Read More →

Get Ready: ICRS 2026 Open for Business and Call for Papers

The 30th anniversary International Car Rental Show heads to the Dallas area as it celebrates a legacy and pivots toward an industry marketplace and forum suited to the fourth decade ahead.

Read More →