Dollar Thrifty Plans for Refranchising, Remarketing and Recovery

Scott Thompson and Jeff Cerefice discuss Dollar Thrifty’s move to refranchise, debt restructuring, fleet financing, the science of car sales, loving 45,000-mile rentals and how the company is positioned well for the run to recovery.

At the end of Dollar Thrifty Automotive Group’s second quarter 2009 investor slideshow, Scott L. Thompson, the company’s president and CEO, closed with a quote from George Patton: “Success is how high you bounce after you hit bottom.”

In the timeline of any business, peaks and valleys are a fluid thing. But if one charts Dollar Thrifty’s progress since the company’s management transition on October 13, 2008, the bounce has been a slingshot bungee ride at the state fair.

In Wall Street terms, DTG was languishing at 97 cents a share at the time. The stock would go even lower, as the company teetered on the verge of being delisted from the New York Stock Exchange amidst talks of bankruptcy in late 2008.

What 10 months and a corporate makeover can do: By mid-August of this year the stock had reached $23, continuing to defy the odds in a stubborn recession and soft travel demand. The company returned to profitability in the second quarter of 2009.

Thompson is quick to point out that the company does not define success or failure based on stock performance. Irrational exuberance or pessimism and market forces beyond a company’s control can drive stocks, like bungee rides, to erratic swings.

Yet the bullish performance is a visible marker that Thompson and his team have positioned the company well to be able to take advantage of an economic recovery in 2010.

In an exclusive first-time interview, Scott Thompson and Jeff Cerefice, vice president, DTG Global Franchise Operations and Development, discuss Dollar Thrifty’s move to refranchise some corporate stores, debt restructuring, fleet financing, the science of car sales, loving 45,000-mile rentals and how a renewed focus on the leisure market is feeding the bottom line.

The Refranchising Initiative

Dollar Thrifty’s corporate belt tightening this year included staff cuts in Tulsa and the closure of smaller, unprofitable stores in the local market. At the same time, 11 corporate stores in smaller airport markets are in various stages of transitioning to franchise operations.

“These stores are profitable, but may not be a good use of our capital,” says Thompson. “Some would be run better by an owner/operator who is entrepreneurially focused. I was a franchisee; I think franchisees can run certain operations better than a corporation.”

Cerefice notes that although the company had been buying back some of the larger franchises in recent years, it had not stopped selling franchises.

“We’ve always felt it’s been a good complement to our corporate store operations,” he says. “It gives us network flexibility depending on the environment. It’s a nice balance.”

Cerefice says the two key ingredients for a Dollar Thrifty franchisee are automotive experience, particularly in car rental or car sales, and the financial means to handle the size of the operation.

Though not a significant revenue driver, refranchising will be part of the business model moving forward. Thompson anticipates a “couple more” refranchise deals by year’s end. “I don’t mind letting some other people make some big money,” says Thompson. “If they make money, we’ll make money.”

Another franchise initiative is an integration of Thrifty Car Sales and rental outlets. “I see Thrifty Car Sales as part of the rental car business,” says Thompson. “I’m optimistic about blending those two business models.”

Managing Debt

As part of the industry right-size crusade this year, Dollar Thrifty has shed 26 percent of its debt since June 30, 2008. The company has a fleet maturity coming due in the first quarter of 2010, though Thompson says the company can pay off that debt with the cash it has on its balance sheet. Other maturities won’t come due until fourth quarter 2010.

This gives the company a needed breather in a still-difficult credit market. The company has avoided any creative financing such as major lease deals and TALF loans. “There are available funds out there, but unless you have a gun to your head, it doesn’t seem like those are the terms you ought to jump on,” says Thompson.

As the credit market thaws, fleet purchases will normalize. However, “I don’t think we’re fixing to go back to robust purchases from the OEM standpoint,” Thompson says. “I don’t think the overall fleet size will change significantly.”

New car pricing continues to be favorable. Whereas manufacturers blamed “low-margin” rental fleet sales for much of the overall sales dip this year, it’s not because they didn’t want to sell to rental, Thompson contends. “[Pulling back from rental sales] has been the public statement, but I don’t feel that from any of the OEMs.”

[PAGEBREAK]

The Science of Sales

Thompson and Cerefice say the company has put a lot more “science” into the buying and selling of fleet. This includes a more disciplined approach to predicting future residuals, setting better floor prices on used units and matching the buy with customer demands, “as opposed to accepting what the manufacturer wanted to sell that week.”

“My background is in retail, so I just look at this like a big used car lot,” says Thompson, a founder of Group 1 Automotive. Thompson grew the megadealer from nothing into a $5 billion player and took it public. “We think the acquisition, management and disposition of inventory are at least equal to the job of renting the cars.”

The company’s two-pronged remarketing approach involves the traditional auction networks and a direct sales team developed in 2007 in anticipation of the move to a risk fleet (the company buys 90 percent risk now). The team resembles the Enterprise model, with incentivized local representatives. Online auction sales are increasing.

With these new sales strategies, attending to almighty utilization figures have taken a back seat. (Fleet utilization for the second quarter of 2009 declined 5.1 percentage points to 80.6 percent. Part of this was a strategy to hold Chrysler product through the bankruptcy.)

“Although we think utilization is an important statistic, it does not dominate our thinking in the organization like it used to,” says Thompson.

Thompson explains that a utilization focus can negatively affect other areas such as revenue per unit. “In order to get utilization up, you may be telling the remarketing guys to ‘shove the cars out the back end of the store’ when the market doesn’t really want the cars,” Thompson contends.

While utilization has decreased somewhat, the buying and selling initiatives have had a positive effect on RPU.

Getting Fleet Mix Right

In line with the industry trend, Dollar Thrifty has cut fleet by about 18 percent through the second quarter and lengthened hold times. The company is running units to about 45,000 miles, before major repairs become an issue.

“The early returns are that the used car market can absorb and love these 40,000 to 50,000-mile cars,” Thompson says. “But I don’t think we have enough information yet to know exactly where the sweet spot is.”

Dollar Thrifty is reducing its dependence on Chrysler, though the manufacturer remains a main supplier. Dollar Thrifty signed a secondary supply agreement with Ford this year.

While the company’s fleet by OEM make is more diversified, the model mix is less “rich.” The company is running fewer minivans, more compact cars and few SUVs.

With new OEM diversity, the move to a risk fleet, extending hold periods and improved remarketing processes, the company expects its fleet costs to fall back to the industry average at some point in 2010.

Position in the New Economy

In the business travel sector, Thompson says Dollar Thrifty has benefitted from companies under corporate travel cost pressures. Yet the company is leaving the Fortune 500 marketplace to Hertz, Avis and National, focusing instead on small entrepreneur mom-and-pop type businesses. Corporate business will not be a significantly larger part of the revenue pie, Thompson says.

With local market stores no longer a factor, Dollar Thrifty will continue to focus on the leisure traveler. The company’s market share is up slightly this year, though not necessarily by design, Thompson says, as the leisure segment has held up better than business travel. Market share will shake out at 12 to 13 percent on airport.

Brand differentiation is narrowing, Thompson maintains. “The car rental industry is becoming a commodity,” he says, highlighting the homogeneity of airport consolidated facilities and a similar OEM and model mix across car rental companies.

Thompson believes higher mileage units and staff cuts have impacted service to a greater extent at the top of the value chain. “I would suspect that some of the premium brands’ wait lines are not that much different than ours now.”

All in all, the new economy seems to be playing into Dollar Thrifty’s hand as a value brand.

“There is a significant price gap there for people to step down in the value chain in tough times,” says Thompson. “If you’re trying to charge a premium for your product, then you have to differentiate yourself. If you’re the value brand, I don’t think you have to differentiate yourself, you just have to provide good value.”

More Fleet Acquisition

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

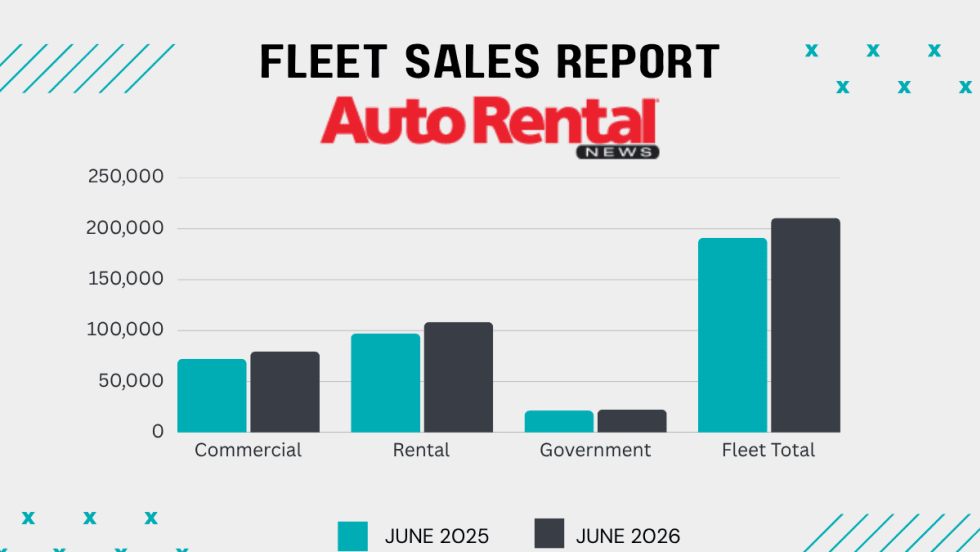

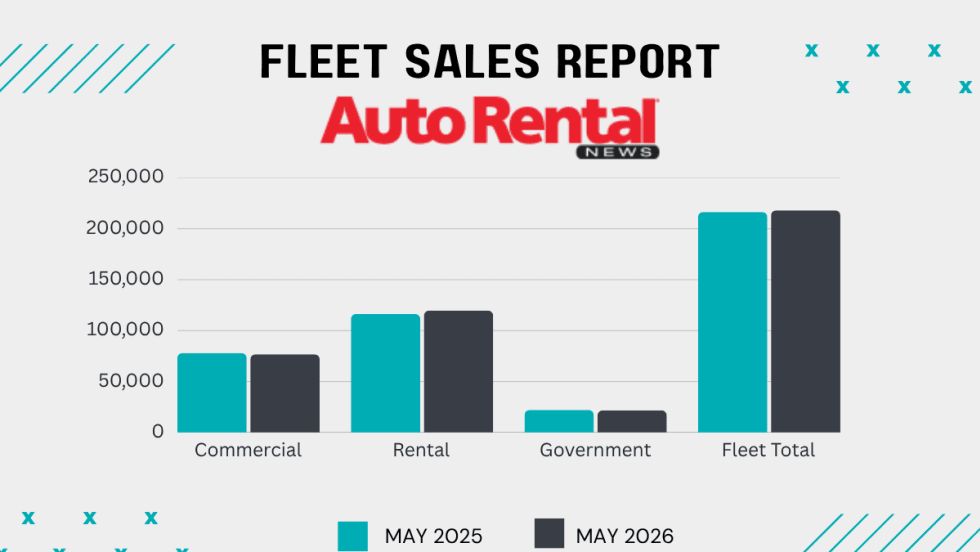

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →

Rethink The Future To Avert A Race To The Bottom

Rental car operators heard a sobering industry message and a stern challenge at the close of the International Car Rental Show.

Read More →

DriveItAway, Free2move Plan Shared Fleet Program for Independent Rental Fleet Operators

Vehicles would be placed with participating rental operations to support car renter demand and provide additional fleet capacity.

Read More →

Stellantis Recalls 1.3 Million Jeep Vehicles Worldwide Over Fire Risk

Stellantis is recalling more than 1.3 million Jeep Wrangler and Gladiator models worldwide over a fire risk linked to power steering pump wiring.

Read More →

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →