Four car rental operators share their stories of finding lenders, how they strengthened these relationships, and how lines of credit have helped their businesses expand.

Working with several lenders, including 1st Source Bank, has helped Monty Merrill (left) expand his fleet at his Dollar Thrifty franchise locations. Merrill is pictured with Danny Owens, city manager, and Rene Mitchell, director of administration, at the Austin service center.

7 min to read

Working with several lenders, including 1st Source Bank, has helped Monty Merrill (left) expand his fleet at his Dollar Thrifty franchise locations. Merrill is pictured with Danny Owens, city manager, and Rene Mitchell, director of administration, at the Austin service center.

When buying his first rental business in 2008, Kamal Fereg knew nothing about car rental, including how to obtain financing from lenders.

“The previous owner financed my first group of cars, but after that I had no idea how to get additional financing,” says Fereg, owner of America’s Best Car Rental, with three locations in Florida. “The lenders I applied for denied me because I had no history.”

Ad Loading...

After more than a year with no success, Fereg sought help from an accountant to get his company’s financial papers together, making sure everything was accurate. According to Fereg, this was the key to helping him get his first financing.

“When I first got financing, I accepted 8% to 9% interest rates,” says Fereg. “I had to run to see which bank would accept me.”

By developing trust with his financial institutions as well as maintaining a strong financial history, Fereg now has the clout to work with multiple lenders and pick the best interest rate for his company. “I can say ‘no’ to certain lenders and dictate my terms with the companies.”

Obtaining several lines of credit has allowed Fereg to grow exponentially — in 2013 he added 300 cars in one year.

Financing is a key element for any rental company, especially when trying to obtain more vehicles. Here are some examples of how financing has helped these car rental companies expand their fleets — from the beginning of their businesses to today.

Ad Loading...

Beginnings and Growth

After working with 1st Source Bank for several years, Sam Zaman of Los Angeles-based Black and White Car Rental needed to increase his line of credit. “I submitted a request to 1st Source,” he says. “Based on our numbers and sales, they gave us the proper amount of line increase that we needed. We were able to grow our Los Angeles International Airport office and added an additional 100 cars.”

In 2007, Yaz Irani started a van rental company in Los Angeles. Once his company had built a solid financial track record, he was able to start picking and choosing several lenders. Within two years, his company tripled in size. “If a location is doing well, I can increase my credit line if I need more vehicles,” says Irani.

Today, Irani’s Airport Van Rental continues to grow. Recently expanding to the Midwest with a location in Indianapolis, his company also has stores in Los Angeles, Las Vegas, San Francisco, Sacramento, San Jose, Orange County, Ontario, Calif., San Diego, Denver, Houston and Portland.

Finding a Lender

Finding a lender isn’t always easy, especially at the beginning of a business. Zaman had to rely on his own funding to get his car rental business off the ground. No lenders would take his business without a history of profits and sales.

“Don’t open a car rental company unless you can start out with your own funds,” advises Zaman. “Don’t depend on the banks for funding the first few years. To gain a bank’s trust, you need at least three years of experience and need to show proof of a successful operation.”

Ad Loading...

When Sam Zaman first started his car rental company in Los Angeles, he had to use his own funding. After a few years, he was able to gain more trust from lenders by showing them a history of his company's profits and sales.

To finance his rental van startup, Irani took a second mortgage on his house. “Then I could show lenders some history of my company’s profit and loss,” he says.

Even with help from his franchisor, Monty Merrill needed access to other financial lines of credit. When he purchased his Thrifty franchise, Merrill signed a supply agreement that said 90% of his fleet vehicles would be purchased through the Thrifty fleet program. But when he continued to grow, he needed to find other financial means to expand his fleet.

“I had to go to the lending market and say, ‘I’m a new guy in the lending market and I need cars,’” says Merrill. “It was a tougher sell than I had imaged. We had to start small and build on it.”

To build up his store in Austin, Merrill sold his brand in San Antonio because he couldn’t get enough financing through banks or lenders.

Taking a Chance

Few lenders want to be the first one in; most aren’t willing to take that risk. But when they are, it usually comes with higher interest rates.

Automotive Financial Corp. (AFC) was the first lender to take a chance on Airport Van Rental. “AFC was the first bank to ever trust us and give us money,” says Irani. “At the start of a company, no one trusts you. AFC came forward. AFC offered a more expensive rate [initially], but the company was willing to take a risk on us.”

Ad Loading...

In 1998, 1st Source Bank decided to take a risk on Black and White Car Rental. And to this day, 1st Source is still the company’s main lending source, says Zaman.

Many newer car rental companies first knock on the door of their local banks. “To a degree, I think that’s a mistake,” says Merrill, who also works with 1st Source Bank. “I would recommend going to banks [that know car rental] first; they understand your business. There is something to be said for your lender really understanding what you are doing.”

Gaining Trust

According to Merrill, in the beginning his company made banks nervous — the agreement with Thrifty consisted of leases that were written off-balance-sheet and then sold through Thrifty. The company was doing well, “but when you looked at my balance sheet, we had nothing. The financers would look and say, ‘you really don’t know what you are doing.’”

How does a rental company build trust with a lender?

For Fereg, it’s keeping your company’s financial books strong. To keep his bank records, income taxes and profit and loss (P&L) statements up-to-date and accurate, Fereg hired an accountant who understood the business.

Ad Loading...

“If your bank statement is inaccurate, it won’t help with getting financing,” says Fereg. “I start each month strong with a clean balance sheet. Because banks look at the statements, I make sure to never be in the negative or low in the daily balance.”

Merrill recommends audited financials. A professional service company like PricewaterhouseCoopers will look at your company’s finances, which includes verifying assets and searching for any holes in financial processes.

“We decided to do audited financials every three or four years,” says Merrill. “We have received positive feedback from the banks and ended up in a rate decrease.”

AFC started to gain more trust in Irani’s company as it expanded. And with his company’s expansion, he also saw more lenders come around: 1st Source Bank, United Leasing, Union Leasing and GE Capital.

“Not only do you want a lender to trust you, but you want to show that other lenders trust you, as well,” says Irani.

Financing Companies for Rental Fleet

1st Source Bank

100 N. Michigan St.

South Bend, IN 46601

(574) 235-2534 www.1stsource.com

Automotive Finance Corp.

13085 Hamilton Crossing Blvd. Suite 300

Carmel, IN 46032

(317) 843-4801 www.afcdealer.com

GE Capital Fleet Services

3 Capital Dr.

Eden Prairie, MN 55344

(952) 828-2548 www.gefleet.com.

NextGear Capital

11799 N. College Ave.

Carmel, IN 46032

(317) 571-3721 www.nextgearcapital.com

United Leasing

3700 Morgan Ave.

Evansville, IN 47715

(812) 485-3673 www.unitedevv.com

Lowering Your Rates

For Merrill, as his company got bigger, the trust became greater, along with better flexibility and rates. Ultimately, he could pick and choose his lenders and get lower rates.

Ad Loading...

Fereg’s experience is similar. “When growth happened, I could go to several lenders and make sure that I got a good rate,” he says. “I have been able to save money by having the capability to shop for a better rate. My average rate is now 4.5%.”

Merrill summed it up well: when it comes to picking lenders, you can’t place all your eggs in one basket. It’s important to have several lines of credit with different lenders.

Lenders view multiple lines as a positive thing, too, as it shows a solvent company vetted by other financing sources with stringent criteria. And if something goes wrong, one lender isn’t left alone holding the bag, according to Irani.

When Merrill renews a contract with a lender, “They want to know about your other lenders,” he says. “They want to know what percent of your credit line that they supply.”

An established car rental company will have three or four lines of credit, or more, along with another financial instrument such as leasing. Merrill holds a general primary line as well as several secondary lines. That way, he can maintain multiple lender relationships. “There can be turmoil when it comes to rental car financing,” he says. “If one pulls away, it’s important to have other financial lines of credit.”

Ad Loading...

Fereg works with seven lenders on a continual basis, including United Leasing, and a local bank who counts his company as its sole car rental client. (United Leasing does not lease cars to the rental industry; it finances them.)

Partners in Business

To car rental companies, lenders should be seen almost as partners in the business. In fact, Irani recommends consulting with them on a regular basis. He sits down with his lenders about once a quarter to talk about business.

“The lenders want to work with you to help you become successful,” says Irani. “Having a close relationship with lenders is important. Ask them for advice; they are the best consultant to talk to.”

Zaman likes that 1st Source has continued to make an effort to build a personal relationship with him. “Our bank rep comes out to our location once every two to three months,” he says. “It’s not just about numbers, profits and losses; 1st Source wants to get a feel for your business and look at you as a person.”

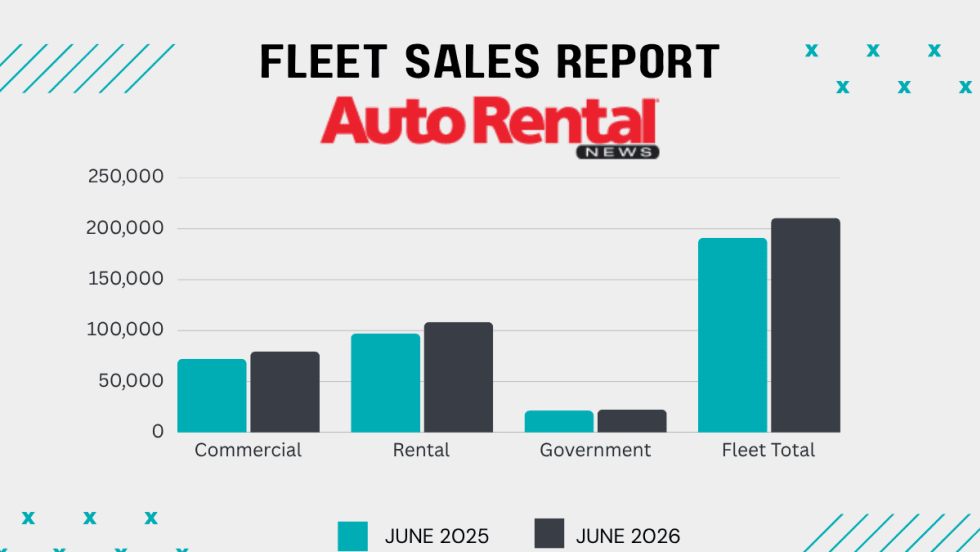

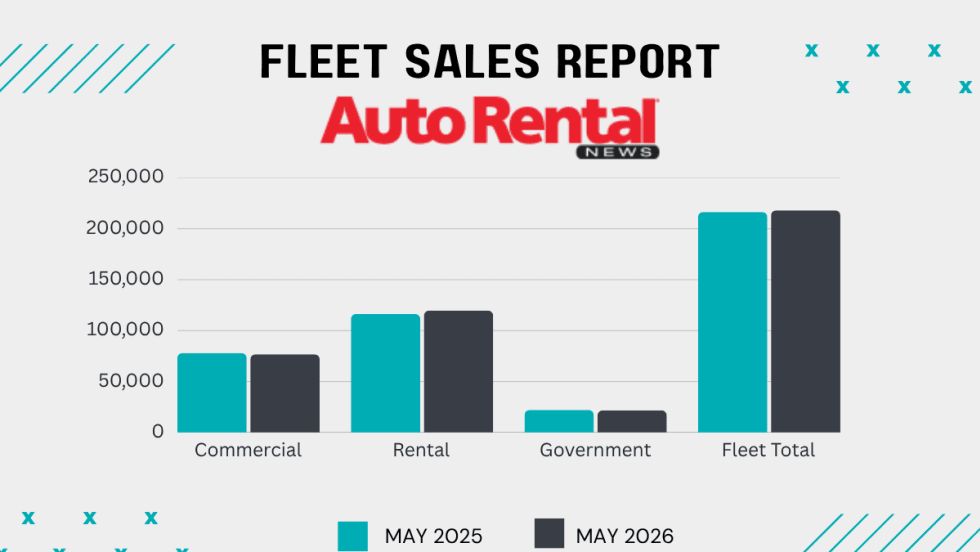

Rental car sales fell 18% from a year earlier, while truck and SUV volume edged higher as rental operators took a more restrained approach to fleet purchasing.