Related Story: How Lenders Can Help Rental Fleets

Taking Advantage of the New Lending Landscape

If you're not following these steps to show your lender confidence in your business, you may be leaving money on the table.

by Mark Eckhaus

July 23, 2015

7 min to read

Is everything old new again? The answer is a very strong yes and no. Are you confused? That›s the car rental business.

In the midst of the Great Recession, Eckhaus Fleet gave a seminar at the Car Rental Show on “How to Be Your Bank’s Best Customer.” Much has changed since then in both the banking and car rental worlds, but not the fundamentals. And all the same factors apply, regardless of your source of funds: banks, financing companies, leasing companies, manufacturers’ captive finance companies or private lenders.

Even in an improving economy, lenders are still nervous. And let’s face it; most conventional lenders still do not understand your business. To take advantage of the ever-changing lending landscape, set a game plan based on the following insights.

Communicate Regularly

Money is available to those who communicate. If you do not personally speak with your lender at least twice a month, you are making a critical mistake. People tend to be more receptive to new requests if they are in the habit of speaking with you and feel they know you.

Show your lender how much business you do with them, from company and employee bank accounts to loans and credit card accounts.

Ready to fleet up or de-fleet? Let them know, along with your reasons. Let the lender make suggestions that will speed up the process. They have more than likely seen it all before and will be happy to help. If you succeed, they succeed.

Keep Financials Current

Detailed financial statements will build credibility and allow you to grow your business — almost nothing else is as important to all lenders. Would you lend money to a rental car company that could not rapidly provide you with full financials and copies of its prior year’s tax returns?

In this day and age, if your lender calls and asks for a copy of last quarter’s financial reports and you tell them it will take a couple of weeks, you’ve raised a red flag. Once you balance your daily business report (DBR), most car rental software packages automatically create journal entries for your chart of accounts.

Define Your Business

Lenders need to know what makes your business special. If you can’t tell them, you’re fueling a lack of confidence.

Who are your customers? Who do you want your customers to be? Who is your local competition? What is your competition doing wrong and what are you doing right? What niche do you fill now, and what niches are you looking to exploit?

Think about this: Do you need to continue to grow or are you right-sized for your market? Don’t grow just to grow. Gaining market share is great, but profits are more important.

Reduce Risk

Reducing risk makes your lender happy. There are a variety of ways to accomplish this:

Have accountant “reviewed statements” always available. Showing retained earnings are crucial.

Really depreciate your cars, not just on paper. Lenders will be much more comfortable if they receive a check to reduce your outstanding credit line each month. Let your lender know about the cars in your fleet that historically have not depreciated significantly. Then they can be sold quickly without a loss should the need arise.

It is extremely important that smaller rental companies own a portion of their fleet. This is a true confidence builder for your lender. It is also good for you.

In the end, you need to show you will make money.

Plan for All Seasons

What is your written business plan for the 2016 and 2017 model years? The next five years? Plan your selling cycle by analyzing your sales history. What has worked well and what has not?

Your fleet plan is a living document! Let your lender see it each time you update it. It is not cast in stone, and your lender will see when you plan to add cars to the fleet and when you plan to sell or send them back. This allows the lender to be prepared.

Share your succession plan and update it as it changes. Be sure your bank has a copy of your “key man” insurance policies — you do have one, don’t you? You need this for yourself and any other true key persons in your company. Is there a “buy-sell” in place that spells out the terms of any such transfer?

Introduce your key people to your lender.

Monitor Everything

Be hands on with your company’s books; question everything. Lenders love owners who are hands on and can explain why they make the decisions they do. Do not continue to do something because that is what you have always done. Be creative. Ask all your employees to participate. Get their opinion on what should be done to make everything run smoother.

Closely monitor the key metrics of your business: daily dollar average, utilization and revenue per unit (RPU). Review every expense every month. Where can you do better?

Delegate or Outsource

Sometimes we find ourselves so busy helping out that we have no time to make money. Do what you do best and delegate or outsource the rest.

Remember that the major car rental companies have tremendous buying power and will always get much better pricing than you will. If you use a fleet management company (FMC) to help with buying and selling, it will advise you on alternative vehicles that make more sense.

If you are going to sell at auctions, an FMC with a national auction account will help you get better run times. If you cannot attend the auction, make sure you have someone to rep your cars and help lower fees.

Let your FMC not only purchase cars for you but also license your cars. The FMC will get it done immediately, saving you rental days that would’ve been lost. For example, one large Eckhaus Fleet account used to have a 12- to 16-day lag time between deliveries and receipt of tags. That was 16 days of lost rental revenue after the company had paid for the car! Eckhaus Fleet changed the scenario so the tags are now sitting at the stores before the cars arrive.

Show Your Expertise

Be sure your lender understands that you and your key personnel are experts in your field. Take your lender to an auction, send him or her an occasional informative email and keep him or her in the loop at all times.

Let your lender know if your company receives an award or other positive recognition. Toot your own horn, just not too loud.

Buy Smart

Buy better-equipped vehicles and not the same cars everyone else does. Buy low mileage used cars as part of your fleet strategy and explain why to your lender.

Don’t buy cars you like — buy cars that make you money, both when you rent them and when you sell them. The last thing you need is to do a superb job at the rental counter and give it all away when you sell.

Occasionally, manufacturers offer those too-good-to-be-true deals. You need to have the flexibility to take advantage of these deals. Your lender needs to understand why these occur and the importance of you being able to immediately say “yes” when these deals appear.

Be a contrary seller. Most everyone sells on the same cycle. Sell your cars sooner with lower miles and get more money. This is a good strategy in today’s market.

Explain the Downturns

A lender who knows you and your business will not panic when you have one-time negative events. When you have these one-time events, or when you change your plans, let your lender know before the fact — never after. This open communication builds confidence in you and your business acumen.

You must perceive your lender as your partner. Tell them the good, the bad and the ugly. This demonstrates that you understand your business and are able to overcome unexpected events.

Most important — when you tell your lender something, deliver on the promise. Telling a lender one thing and then doing something else — or not doing what you said — does not inspire confidence. Everyone understands that things change. Again, just communicate changes before they happen. Be smart!

Know Your Lender

Lenders are also a business and they, too, must make a profit. Never forget that your lender operates under rules, mandates, guidelines and regulations. Be 100% sure you understand and adhere to them.

Be prudent; don’t ever put all your eggs in one lender’s basket. Strange and unexpected things will happen, such as a company buyout. Can you afford to have your current lender exit the market? Suppose the new owner decides to call in your loan(s) because he or she doesn’t like your business model. What then?

So, are you one of your lenders best customers? You must be if you want to stay in business and grow.

Subscribe to Our Newsletter

More Rental Operations

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

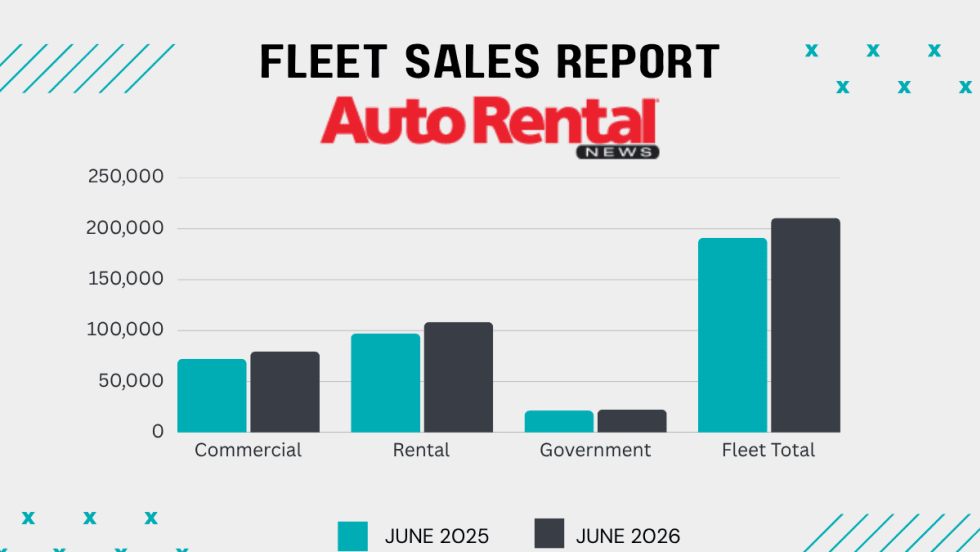

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →