The ABC’s of Manufacturer Repurchase Programs

Repurchase programs are still available to small- and medium-sized rental companies. For the uninitiated, here’s how they work and when they work best.

The manufacturers have severely curtailed their repurchase programs to the major car rental companies in recent years. Smaller rental operators might then assume that repurchase programs are becoming extinct. On the contrary, repurchase programs are alive and available to small- and medium-sized rental companies through independent fleet suppliers.

For the uninitiated, here's a primer on how auto rental repurchase programs (also called buyback programs) work and in what financial and business environments they work best.

What Are Repurchase Programs?

In a repurchase program the manufacturer agrees to buy back the vehicle for a set monthly depreciated value, provided the vehicle is returned in a specified time period and in the contracted condition. The model choices and quantity are limited by the manufacturer. The cars are delivered directly to your location or a nearby dealer depending on the program. The cars are returned to regional return locations, usually auctions.

The manufacturers provide these programs for a variety of reasons. Their vehicles are introduced to a large captive set of potential customers (your renters!). The returned vehicles provide a source of clean, low-mileage used cars for their dealers. Since the cars are ordered months ahead of time, a repurchase program guarantees a minimum level of production.

Most of the manufacturers' programs for fleets with fewer than 5,000 units are handled by independent fleet supply companies. Those companies commit to ordering a large number of cars and then offer a program to smaller rental fleets at costs comparable to the programs offered to larger fleets. There is a consolidation fee to cover the costs of consolidating the orders to the manufacturer including dealer fees, commissions, processing costs and profits.

Most fleet supply companies are simply order takers, while a few others also handle the order processing, sales support and return processing for the rental car company and the manufacturer. They provide a higher level of support and will work with the RAC and the manufacturer to resolve problems.

When a Repurchase Program Makes Sense

Here are some advantages to repurchase programs and business scenarios in which they work best.

● It is low risk for the rental company. The used-car market can be fickle: With a repurchase program, the RAC does not get stuck with cars that will have to be sold in a down market. If something bad happens, the RAC can defleet quickly and at a much lower cost. If the RAC returns the car early, it only pays the minimum program term depreciation. If the RAC decides to keep the car, it already owns the vehicle. The RAC should call its fleet supplier and request a non-return allowance.

● It is low risk for your funding source, because the lending institution is only funding the depreciation for the time the vehicles are in service. (See the Hyundai Elantra example: Should your company fold the day after the bank funds the car, the car gets returned to Hyundai. The bank gets back $15,902. The bank's maximum risk is only $1,620 plus interest.)

● If the program is for four to six months, the RAC can stock up for a season and not get stuck with cars. For example, the RAC can get AWD SUVs for the ski season in November and return them in March. Or the RAC can get convertibles and small cars in May and return them in September, when everyone else is trying to sell cars.

● For the customer base that puts a lot of miles on the cars, repurchase programs allow as much as 24,000 to 30,000 miles for the term, which can be as short as four months.

● There are no remarketing costs, such as auction fees, and low to no transportation costs.

● The RAC has the customer service benefit of offering nice, new vehicles.

● There are low maintenance costs because the cars are newer.

● You can explore new markets with little risk because you already know what your costs are. For example, you can try a few 15-passenger vans, convertibles or SUVs.

● It is not optimal to buy new vehicles that depreciate quickly, such as 15-passenger vans. On a repurchase program a new Chevy Express van could be available for $550 a month in depreciation plus interest. You can cover its monthly cost with a week's rental.[PAGEBREAK]

When Buying at Risk Makes Sense

While the term "risk" could worry an untrained banker, buying risk vehicles has numerous advantages as well. (We are moving toward the term "asset value" to replace it.)

● You remarket your own cars. If you own a used-car lot or have a team dedicated to maximizing your profits when you sell your car, it makes a lot of sense.

● You keep your cars for 18 months or more and you depreciate them properly.

● When the fleet price offers a great discount and the car can be depreciated at 2 percent. For example, the fleet price on a 2010 Hyundai Elantra is $13,922, $3,300 under invoice. The Manheim Market Report (MMR) on the 2009 model is $11,296, while the 2008 model is $9,058. The RAC can depreciate the car at 2 percent comfortably and the car covers two rental classes.

● When the car model has a history of holding its residual value.

● When you only buy used cars.

● When you have limited finances and you need more cars than you can afford with a repurchase deal. With a repurchase program you buy the car at clean fleet invoice, which is not a deeply discounted price. The manufacturer wants the cars back, so it prices them to encourage their return.

● When your bank does not understand or is unfamiliar with repurchase. Some banks do not understand that the manufacturers actually buy the cars back after you use them for a few months. It just seems too good to be true.

Examples:

2010 Hyundai Elantra GLS sedan, four-month program

The cost of the car is $17,522 (a capital cost of $17,222, plus $300 consolidation fee).

Hyundai deducts depreciation of $330 per month for the use of the vehicle from the cap cost of $17,222. After four months the depreciation totals $1,320. The RAC's four-month holding cost is $1,620 plus interest.

On return of the vehicle, assuming all terms and conditions of the repurchase contract have been met, the manufacturer pays $15,902 (cap cost of $17,222, minus $1,320 in depreciation).

2010 Chevrolet 15 Passenger Express LT van, eight-month program

The cost of the vehicle is $33,534 (a capital cost of $33,034, plus a consolidation fee of $500).

Chevrolet deducts depreciation of $550 per month for the use of the vehicle from the cap cost of $33,034. After eight months the depreciation totals $4,400. The RAC's eight-month holding cost is $4,900 plus interest.

On return of the vehicle, assuming all terms and conditions of the repurchase contract have been met, the manufacturer pays $28,634 (cap cost of $33,034, minus $4,400 in depreciation).

[PAGEBREAK]

SIDEBAR: A Step-by-Step Guide to Repurchase Programs

The rental car company decides what vehicles it needs to meet fleet demands. The manufacturers offer a variety of new-vehicle programs, from compacts to 15-passenger vans.

The RAC decides how long it needs the vehicles. This is a function of the mileage limitations of the selected program and your season. Plan for a five- to six-month period in an area where customers drive long distances, with a second delivery of new cars at the end of the period. For a shorter season, select a four-month period. The length of the program, mileage limits and other terms vary by manufacturer. Work with the fleet supply company for the best available programs.

The RAC arranges funding with the bank or lending institution. The amount funded is the capital cost of the vehicle plus a consolidation fee. The manufacturer guarantees to repurchase the vehicle at the end of the service period. This assumes that the vehicle is not over the mileage limit or damage allowance.

At the end of the period, the cars are sent back to a location designated by the manufacturer. Depending on the program, this cost is partially to fully covered by the manufacturer through a transportation allowance. After the cars are checked in and accepted for repurchase, a check is sent to the lien holder to pay off the loan.

Repurchase Programs: Paperwork and Details

● Vehicles are shipped directly to the RAC or a nearby dealer.

The RAC receives:

- bill of sale

- copy of MSOs (Manufacturer's Statement of Origin) or copy of title application showing bank as lien holder, depending on state.

- copy of vehicle invoice

● On arrival of vehicles, the RAC's funding source overnights payment (cap cost plus fee) to the fleet supply company. On receipt of payment, MSOs are overnighted to you or your funding source as has been previously designated.

● Depending on the program, the RAC notifies the fleet supply company when the vehicles will be returned, usually 10 days before the date they will be sent back. The RAC is given a return location by the manufacturer.

● Vehicles and clear titles are returned and checked in. Condition reports are sent to the rental account to sign off on. The manufacturer sends the appropriate funds to the lien holder usually within 35 days.

Tim Yopp is chief technology officer of Eckhaus Fleet LLC, one of the largest independent fleet suppliers representing Hyundai, Suzuki, Toyota and other manufacturers to the corporate fleet and rental car industries. He can be reached at tim@eckhausfleet.com.

Mark Eckhaus is CEO of Eckhaus Fleet LLC and a principal in several new car dealerships. He can be reached at Meckhaus@aol.com.

More Fleet Acquisition

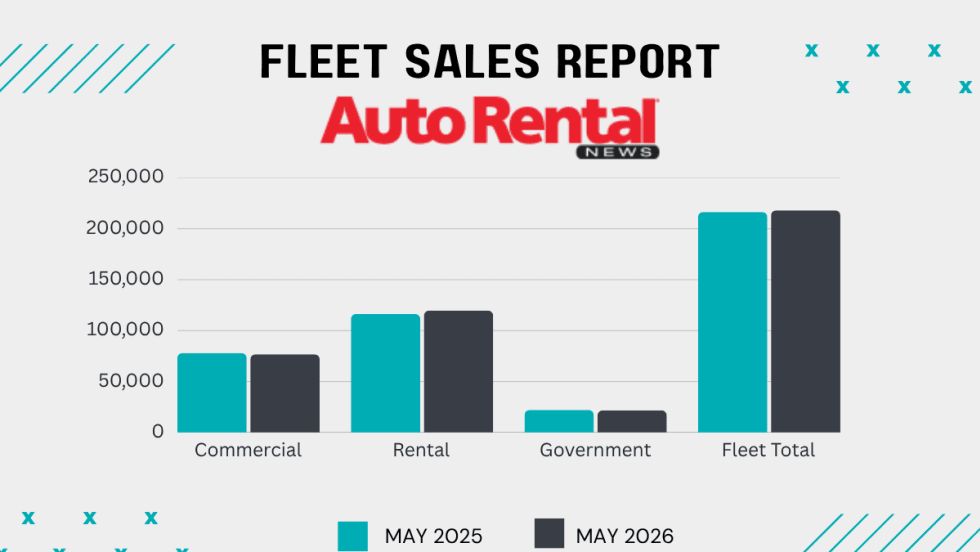

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Get Ready To Roll: No Stopping Self-Driving Rental Cars

The autonomous mobility technology revolution will move at its own pace, but sooner rather than later.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

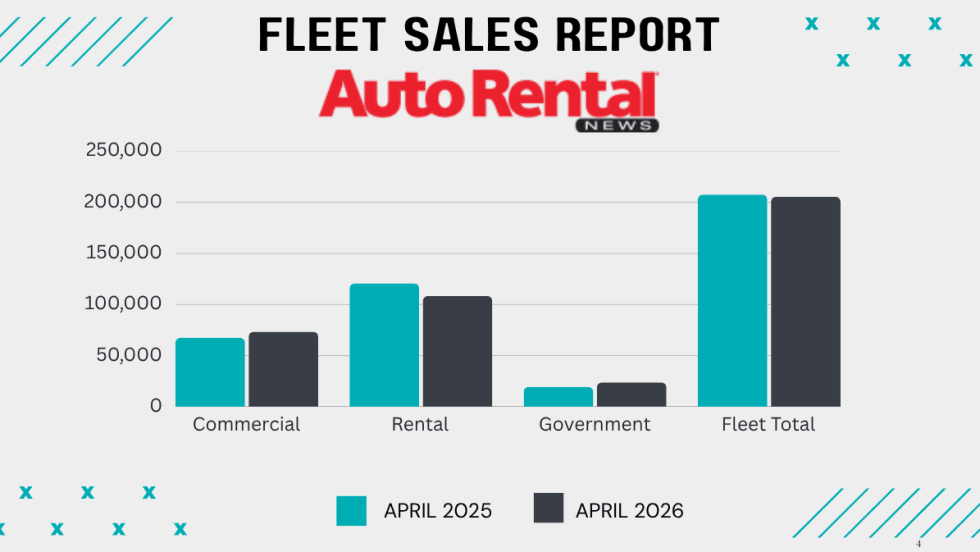

Monthly Rental Fleet Sales Dip Again As YTD Numbers Flatten

Pull-ahead demand for rental cars in the second half of 2025 appears to be slowing purchases so far this year.

Read More →

DriveItAway Transitions To OTCID, Expands To 40 U.S. Markets

The dual milestone propels the company toward its goals of accessing longer-term capital markets and deploying a national platform.

Read More →

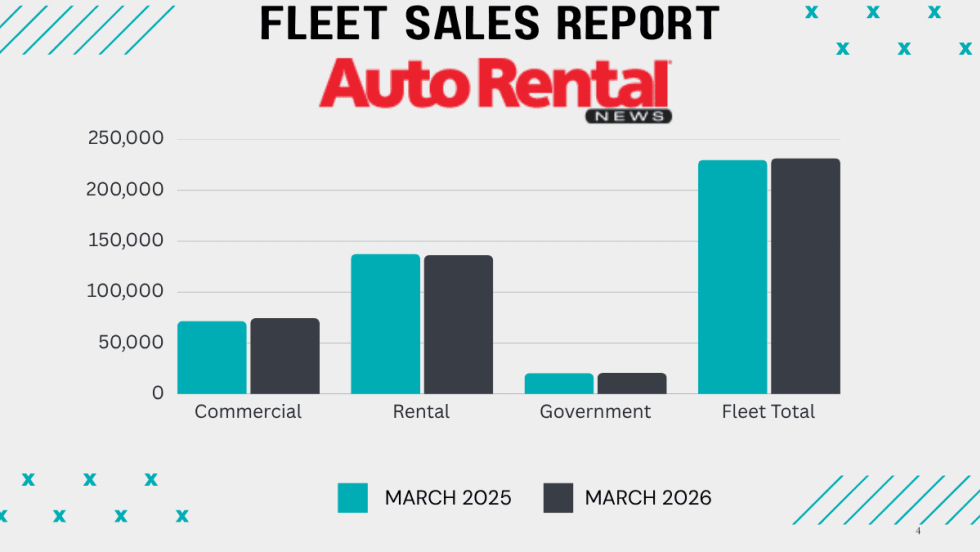

Rental Fleet Sales Stay Ahead In Q1 Despite Monthly Dip

Vehicle sales into commercial fleets are outpacing rental car fleet purchases so far this year.

Read More →

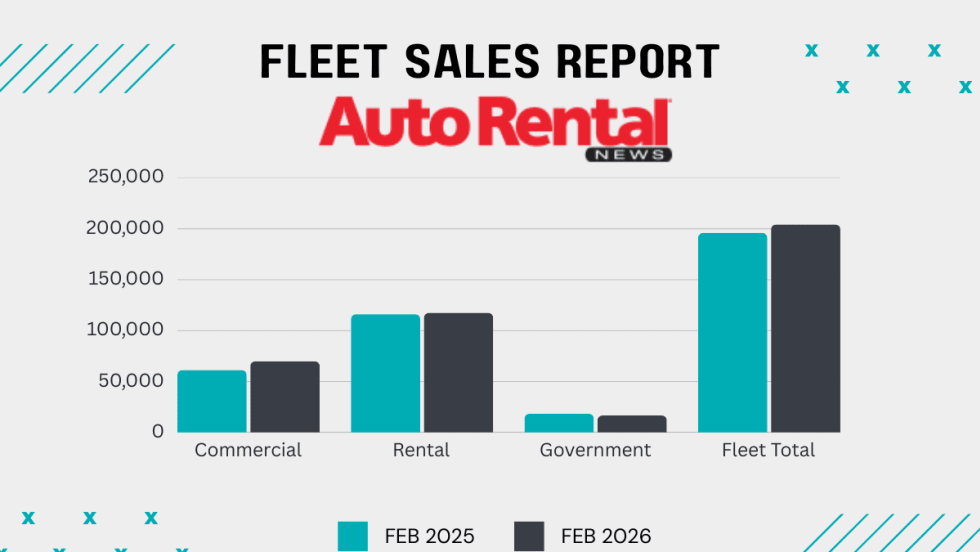

Rental Fleet Sales Slow In February Ending A Strong Streak

Commercial fleets posted the most gains, sustaining increases in monthly and year-to-date fleet sales

Read More →

How It's Still Possible To Run An Electric Rental Fleet

This Season 2 / Episode 4 of Auto Rental News’ Industry Newsmakers series broaches a difficult subject in car rental: How do you make EVs succeed?

Read More →

Avis Budget Group Reports Near $1 Billion Loss Tied To 2025 EV Fleet Write-Down

Following Hertz, the company is the second global car rental conglomerate to sustain sizable losses due to lower customer demand and usage of electric rental cars.

Read More →

Rental Fleet Sales Shoot Ahead From The Starting Line

Rental car operations continued their 2025 reputation as the top driver of fleet sales.

Read More →