More Reading: How Auto Transport Is Adapting to Supply Chain Challenges

What is Scott Painter’s Plan for 23k Electric Vehicles?

In explaining strategy for his new all-electric subscription startup Autonomy, Painter shares which manufacturers are poised to win the EV race, why Fair failed, and how his large EV order holds clues for where EVs will grow and how they’re used.

October 11, 2022

Painter says that 80% of Autonomy’s present customers are primarily plugging into 110v outlets at home for Level 1 charging and only traveling an average of 25 miles a day.

Photo: Autonomy

9 min to read

Scott Painter is all in on electric.

If car manufacturers are switching to electric, and California and New York are legislating electric futures, Painter figures it’s time to get ahead of the game right now.

Painter — the self-proclaimed serial entrepreneur who founded CarsDirect.com, TrueCar, and Fair — has a new startup called Autonomy. In August, the all-electric vehicle subscription service placed an order of 23,000 EVs from multiple manufacturers worth $1.2 billion.

Six years ago, the vehicle subscription model appeared poised to steal share from ownership, leasing, and long-term rentals. It offered an “easy button” to get a car: no dealer paperwork or long-term contract, the ability switch into multiple vehicles, and one price that bundled the vehicle payment with routine maintenance and insurance.

Painter was there with Fair, which by 2017 had raised more than $2 billion from high-profile investors such as SoftBank and the venture arms of BMW and Penske. Yet Fair would wind down operations three years later, and other high-profile services — particularly the ones offered by auto manufacturers — didn’t survive that long.

With Autonomy ramping up with new customers and new markets, Painter is ready to share why this new vehicle subscription model is poised win where previous iterations did not. Within this discussion, he shares insights into his dealings with individual manufacturers on the order, how his EV deal differentiates from Hertz’s offerings, the surprising use profiles of Autonomy’s customers, and a candid assessment of why Fair failed.

Painter’s assessments hold clues as to where EVs will grow in the near term and how they’ll be used.

Which Manufacturers Are Stepping Up?

When Autonomy started service in January of this year, the fleet consisted only of Tesla Model 3 and Model Y. This 23,000-unit order is spread across Tesla and 17 other manufacturers: BMW, Canoo, Fisker, Ford, General Motors, Hyundai, Kia, Lucid, Mercedes-Benz, Polestar, Rivian, Stellantis, Subaru, Toyota, Vinfast, Volvo, and Volkswagen.

Those vehicles will be fleeted in the next 12 to 18 months. In terms of which manufacturers can deliver and when, Painter is learning that “not everyone is in the same place.”

Autonomy is buying 600 Mercedes EQS and EQEs. “Mercedes has been very diligent and very responsive,” he says. “They got back to us with VIN numbers, delivery dates, and locations for all 600 cars.”

He credits General Motors as an incumbent manufacturer with a “strong fleet muscle and a very disciplined organization” that gave a quick response on selling cars, yet with lingering supply chain issues. “They just said point blank, ‘We can't get any cars for 60 days,’” though he adds that GM has “a very deep lineup of cars coming around the corner; they're just not here tomorrow.”

In terms of the non-major upstart manufacturers, “These new entrants are all over the map,” Painter says. “Some of them are so new, even though they have billions of dollars, I don't think those cars are going to hit the market en masse any time soon.”

Painter is banking on only a small flow of ordered vehicles to come in during the fourth quarter, with the faucet opening in three to six months.

Tesla Is the Gold Standard

In terms of the supply chain, Painter believes Tesla is winning by having greater control of its chipset and component production, as well as making smart decisions like using a 1-megapixel camera instead of 12 megapixels, which limits the number of chips and alleviates the need for greater processing power. (Elon Musk has called his company “absurdly vertically integrated compared to other auto companies.”)

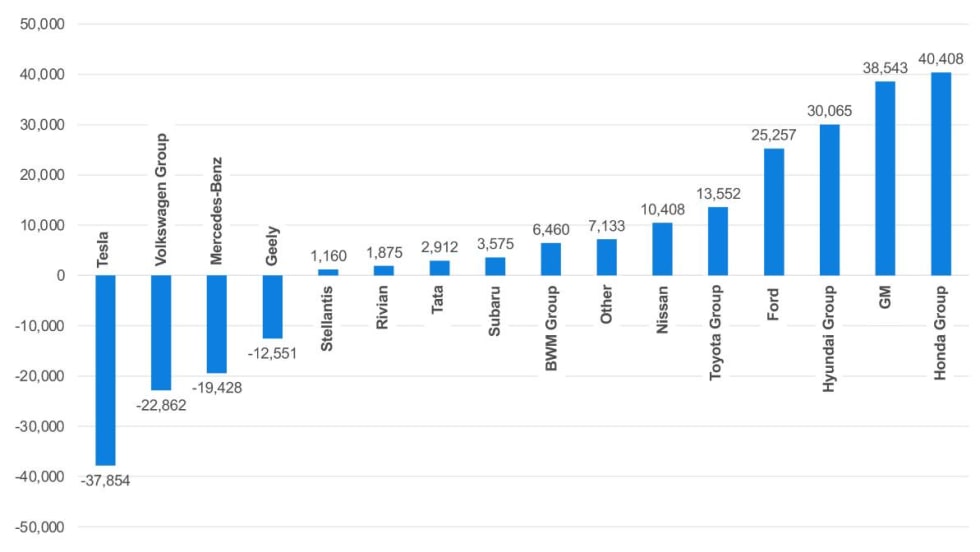

The result for Tesla is healthy production. Tesla scored the highest year-over-year sales increase by far through the first nine months of 2022, while virtually every other manufacturer experienced steep declines.

Painter knew he had to diversify the Autonomy fleet across multiple OEMs to spread supply chain risk. Yet running one EV manufacturer has its advantages. Autonomy easily integrated the Model 3 into its app, while onboarding new manufacturers will take a new 45-day learning curve.

Further, Teslas are 5G connected; the factory modem allows Autonomy to locate every car all the time, and it receives digital notification of crashes instantly to allow the immediate creation of a digital accident report.

Tesla faces demand concerns and growing competition. However, “If you want to start rolling cars right now, the name of the game is Tesla,” Painter says.

EV registrations are growing in the obvious areas such as the state of California and New York’s tri-state area, along with Seattle and the Miami/Ft. Lauderdale market. Up-and-coming markets that aren’t so obvious include Austin and San Antonio in Texas and Phoenix.

Photo: Autonomy

Putting Hertz’s EV Order in Perspective

While Autonomy’s 23,000-unit order is a large one, it can’t compete in sheer size with Hertz’s gauntlet-laying order last year of 100,000 Teslas, and its most recent order of 175,000 EVs from other manufacturers over the next five years.

Painter says to look past the headlines at the actual ratio of EVs in Hertz’s fleet, which Painter contends will be under the adoption rate of EVs in general. “The fact that they're ordering electric is more about the zeitgeist of the moment,” Painter says. (Hertz’s stated goal is to have one-quarter of its fleet be electric by the end of 2024.)

“We're making a very different bet,” he says. “We believe that electric is what we're going to drive. And that's all we have.”

Renting to Uber drivers is a big part of the Hertz play, with up to 50,000 units dedicated to them. This will have an immediate impact on infrastructure, as most Uber drivers will need to use Tesla Superchargers.

Autonomy’s Contrarian Customer Patterns

On the other hand, Autonomy’s subscribers fit more of an ownership driving pattern. They aren’t putting many miles on the cars, which enables Level 1 charging.

Painter says that 80% of Autonomy’s customers are primarily plugging into 110v outlets for Level 1 trickle charging. While that’s like filling up a gas tank with an eye dropper, Painter says that the same 80% only travel an average of 25 miles a day. With 300 miles of range and trickle charging at night, drivers could get two weeks of driving in that scenario.

“I think part of the reason why we've had real traction with Tesla as a partner is that the charging pattern of a subscriber is at home,” says Painter, who asserts — perhaps surprisingly — that he trickle-charges his Tesla at home too.

That said, trickle charging is not the answer to how Autonomy will scale. Look to the growth of DC fast charging instead, he says. And for that reason, Painter is charting the correlation between EV registrations and DC fast charging to plan the markets in which Autonomy will open next.

The Unexpected Markets Where EVs Growing

EV registrations are growing in the obvious areas such as the state of California and New York’s tri-state area, along with Seattle and the Miami/Ft. Lauderdale market. Up-and-coming markets that aren’t so obvious include Austin and San Antonio in Texas and Phoenix.

Autonomy’s next markets are Florida, Texas, Washington, and Arizona. The service is working with AutoNation, which will provide vehicle prep and delivery along with maintenance and reconditioning for the fleet.

However, “California is still the mother's milk and it’s going to be that way for the foreseeable future,” Painter says, adding that 16% of new cars registered in the state today are electric and there are five times the number of DC fast charging stations in California than in any other state.

Early Subscriptions Had Old Financing Models

As to why early subscription models didn’t survive, there were issues from a customer value perspective and others from a provider operations perspective.

On the latter, a big issue was financing. When Fair started, financing companies didn’t quite understand subscriptions, Painter says. Instead, they were trying to marry traditional fixed-term 36-month leases and long-term loans with the short-term flexibility of a subscription.

That traditional financing instrument was easier to manage but came with higher monthly fees for users because they needed to account for vehicles’ inherently steep first-year depreciation.

As well, Painter was dealing with multiple lenders, and each one preferred different car types and customer profiles. “That level of complication was impossible,” he says. “All these programs looked great; they just weren't priced well. But they did reset the customer experience around the ease of a subscription.”

Lenders today are more sophisticated in their offerings to subscription services. Autonomy uses a “warehouse” facility that doesn’t require securitization of cars and allows the service to borrow money more like a large car rental company or car dealership. “We're now seeing lenders for the first time come to us and say, let's give you the kind of debt you need to be able to finance the fleet,” he says.

Why Are Subscriptions Poised to Win Now?

On this question, Painter starts with the traditional customer-focused angle of flexibility and transaction ease. Those points have formed the value proposition of subscriptions all along. Then what’s new?

The penetration of electric cars, for one. With EVs, customers can test the present charging infrastructure to see if it fits their driving patterns. They can walk away after Autonomy’s initial three-month term if desired. (An emerging option is to roll charging into the vehicle payment in Electric Vehicles-as-a-Service schemes. However, this is not part of Autonomy’s offering.)

Early subscribers were allowed to trade out cars in set intervals. While this was a relevant perk, the service needed to have a fleet of available cars on hand. Autonomy, however, only acquires cars in response to a reservation holder waitlist, which allows for precise utilization. “Right now, our utilization curve is full. We don't have any cars just sitting,” Painter says.

Another new change involves insurance.

Autonomy is readying an episodic (on-demand) insurance product that can be activated by the day, which is more flexible to a greater variety of customers’ needs for a car. When the car sits, the insurance is turned off and the vehicle will be protected under Autonomy’s comp and collision policy.

“That is pretty groundbreaking,” Painter says of the product, which will launch in the first quarter of 2023. “We are essentially a captive insurance company. This is as much of an Insurtech play as it is a FinTech play.”

Painter says Autonomy is more astute at navigating various regulations around leases and short-term rentals, which has tax and paperwork efficiency implications depending on the state. Autonomy is writing contracts on leasing regulations in most of its states, and on rental regulations in others.

“We understand this stuff at a deep operational level,” he says. “But the name of the game is delivering the customer a 100% digital contract that they can sign with their finger on their phone.”

In this new model, Autonomy can address the biggest issue with subscriptions: Adding up subscription costs and those borne by the user, erstwhile programs were just too expensive. Autonomy markets its service as cheaper than a Tesla lease. Others have done the math to compare Autonomy’s and Tesla’s options in detail.

A New Tipping Point?

The used car market is cooling off from its incredible pandemic-induced run of the last two years, which is likely to continue into the first quarter of 2023. After that, “We're about to experience for the first time a true supply shortage, in addition to a demand shift,” Painter says.

The demand shift is to electric vehicles, which will result in residual value gains. (The values of used Teslas validate this, though representative of only one manufacturer so far.)

But don’t count out ICE vehicles. Because of the leases that weren’t generated when the pandemic started, by the end of the first quarter of 2023 that lack of lease returns will cause used values to spike again and last some 12 to 18 months.

“Used cars are going to become a massively precious commodity,” Painter says. “If you’re in the car business, it means start buying used cars now and load the heck up.”

Subscribe to Our Newsletter

More Green Fleet

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

Green Motion Expands Its African Presence with Mozambique Launch

This new rental car outlet reflects the growing demand for reliable transportation and the emphasis on sustainable travel across the continent.

Read More →

Survey: New Tech Tools, Sharper Pricing Plans, and Focused Service Can Improve Rental Car Industry

ICRS 2025: What are key trends, challenges, and opportunities confronting rental car operators this year?

Read More →

Green Motion Adds South Korea to Its Asian Service Region

The first Green Motion locations in South Korea are scheduled to open in key travel hubs during the coming months, including Seoul, Jeju, and Busan International Airports.

Read More →

Federal Highway Administration Halts EV Charger Funding, Delaying National Expansion Plans

The FHWA has rescinded funding for the NEVI Formula Program, delaying nationwide EV expansion as policies undergo federal review.

Read More →

Operator Outlook: EVs Slow to Charm Rental Car Industry

2025 ARN Fact Book: Electric vehicles still must prove their reliability and worth in a fleet sector that puts rolling metal on the ground 24/7 for a demanding customer base.

Read More →

Green Motion Opens Franchise in Germany’s Most Populous State

The rental car outlet brings its hybrid and electric vehicles and sustainable approach to business to one of Europe’s most economically powerful regions.

Read More →

U.S. EV Sales Push to Record 1.3 Million in 2024

Domestic sales of EVs benefitted from strong incentives from the automakers, excellent lease deals, and federal and state incentive programs.

Read More →

Electric Vehicles Still Destined to Succeed

2025 ARN Fact Book ACRA Column: The technology, lower costs, and energy improvements of future electric vehicles will make them too good to turn down. Rental fleets should prepare now.

Read More →

4 Global Trends in Carsharing for 2025

Despite operational challenges and questions, the global car-sharing market continues growing and will likely double during the next decade.

Read More →