DTAG Previous Filings to Be Restated for Accounting Under SFAS No. 133

Company will amend past quarterly and annual reports to reflect accounting corrections.

Dollar Thrifty Automotive Group Inc. today announced its plans to restate previous financial results from fiscal year 2001 through the third quarter of fiscal year 2006. After further examination and discussions with the company's independent registered public accounting firm, Deloitte & Touche LLP, the management of the company recommended and the Audit Committee of the Board of Directors concluded that the company's historical financial statements should no longer be relied upon as a result of an error related to the accounting for certain derivative transactions under Statement of Financial Accounting Standards No. 133, "Accounting for Derivative Instruments and Hedging Activities," as amended ("SFAS No. 133").

The correction of the accounting treatment of these derivative transactions does not change the highly effective nature of the interest rate swaps, nor does it have any impact on the company's cash flows; however, it will introduce significant volatility to the company's reported net income and earnings per share.

The company entered into interest rate swap agreements in connection with its asset-backed note issuances to reduce its exposure to market risks from fluctuating interest rates. The company accounted for its derivative instruments in accordance with SFAS No. 133. SFAS No. 133 requires that all derivative instruments be recorded on the balance sheet as either an asset or liability measured at its fair value, and that changes in the derivatives' fair value be recognized currently in earnings unless specific hedge accounting criteria are met.

From inception of the company's hedge program in 2001, it applied a method of cash flow hedge accounting under SFAS No. 133 to account for the interest rate swap transactions that allowed it to assume the effectiveness of such transactions, called the "short-cut" method. The company recently concluded that its interest rate swap transactions did not qualify for the "short-cut" method under SFAS No. 133 in prior periods because of certain prepayment clauses contained in the documents relating to the asset-backed note issuances. Therefore, fluctuations in the derivatives' fair value should have been recorded through the income statement instead of through other comprehensive income (loss), which is a component of stockholders' equity.

Although management believes that the interest rate swap transactions would have qualified for hedge accounting under the "long-haul" method, hedge accounting under SFAS No. 133 is not allowed retrospectively because the hedge documentation required for the "long-haul" method was not in place at the inception of the hedge. The company expects that future interest rate swap transactions will qualify for hedge accounting under the "long-haul" method and thus be reflected in the balance sheet in other comprehensive income (loss).

The company will be filing an amendment to its Annual Report on Form 10-K for the year ended December 31, 2005 ("2005 Annual Report"), to amend and restate financial statements and other financial information for the years ended December 31, 2005, 2004, 2003, 2002 and 2001, and for each of the quarters in the years ended December 31, 2005 and 2004. In addition, the company will be filing amendments to its Quarterly Reports on Form 10-Q for each of the periods ended September 30, 2006, June 30, 2006, and March 31, 2006 to amend and restate financial statements for the first three quarters of 2006 ("2006 Quarterly Reports").

The change in accounting treatment for the affected swaps, excluding the impact of the state income tax rate discussed below, had the following impact:

Increase

(Decrease) in Net Income ($000s) | Increase

(Decrease) in Diluted EPS | |

For 2006: | ||

3rd Quarter | $(15,488) | $(0.62) |

2nd Quarter | $6,307 | $0.25 |

1st Quarter | $4,829 | $0.18 |

2005 | $18,133 | $0.69 |

2004 | $14,801 | $0.56 |

2003 | $5,430 | $0.22 |

2002 | $(18,855) | $(0.76) |

2001 | $(6,758) | $(0.28) |

The company also identified an error in its estimated effective state income tax rate, which has resulted in a cumulative overstatement of the net deferred state tax liability of approximately $5 million at December 31, 2005. The company will correct this error in the amendment to its 2005 Annual Report and its 2006 Quarterly Reports.

Additionally, management has determined that as a result of the restatement of the financial statements for the above referenced periods, management's prior conclusion on the effectiveness of internal control over financial reporting as of December 31, 2005, and management's evaluation of the effectiveness of the design and operation of the company's disclosure controls and procedures for the 2005 Annual Report and the 2006 Quarterly Reports should be amended. Management determined that a material weakness, as defined by the Public Company Accounting Oversight Board (United States), existed relating to its assessment of the ability to continue to use the "short-cut" method under SFAS No. 133 as of September 30, 2006, June 30, 2006, March 31, 2006 and December 31, 2005. Management also determined that a material weakness existed related to management's periodic assessment of the methodology used for estimating the deferred state tax liability as of December 31, 2005.

Further information regarding the company's restatement can be found in its Form 8-K filed with the SEC today.

More Rental Operations

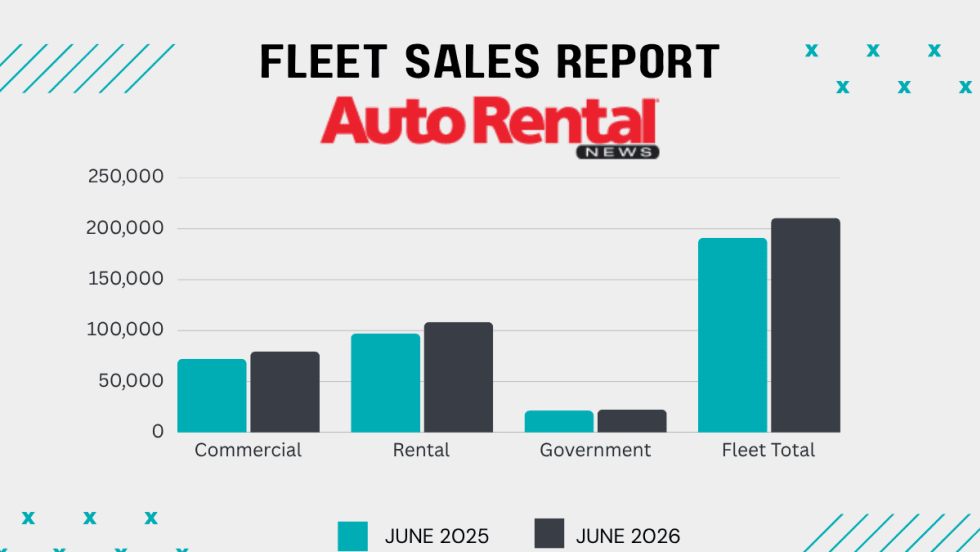

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →

Stop Losing Money On Rental Tolls

Regardless of your rental fleet size and structure, fleet managers, executives, and owners can gain valuable insights into an often-overlooked area of fleet operations.

Read More →

Rethink The Future To Avert A Race To The Bottom

Rental car operators heard a sobering industry message and a stern challenge at the close of the International Car Rental Show.

Read More →

DriveItAway, Free2move Plan Shared Fleet Program for Independent Rental Fleet Operators

Vehicles would be placed with participating rental operations to support car renter demand and provide additional fleet capacity.

Read More →