Fed Rate Hikes Denting Demand for Autos

Analysis: The Fed wants to see less credit flowing as part of their plan to induce pain, and it's working. Are they taking enough time to see the effects of their moves before doubling down?

Cox Automotive chief economist Jonathan Smoke sees the Fed's quest to tame inflation as possibly tamping down vehicle demand, as the retail and wholesale used markets have been oversupplied this summer, leading to more than 10% declines in wholesale prices over the last 100 days.

Photo: IARA

The Fed raised the target for the Federal Funds Rate by three-quarters of a percentage point on Sept. 21, making another aggressive move to, as Fed Chair Jerome Powell suggests, induce “pain in the economy” as the cost of reducing inflation. The biggest news was not the increase, but the plans for where rates go from here.

Combined with the increases made in June and July, the Fed has now moved the target rate more in 120 days than at any point since 1981.

The current short-term rate level is now considered restrictive, meaning that this level of rates will cause the economy to slow. And the Fed is not done. Their new dot plots reflect they want rates to be 1.25 points higher by year-end and another .25 points in 2023. Perhaps worse still, the dot plots indicate rates remain restrictive through 2025, although the absolute level may come down slightly.

We have seen auto loan rates move this summer to be consistent with the Fed moves through July. In housing, mortgage rates have moved even more.

Pain Management Ahead

The Fed wants to see less credit flowing as a key part of their plan to induce pain, and they are getting what they want. The problem may soon be that they are not taking time to see the impact of their moves before doubling down.

Housing and auto account for more than 20% of the U.S. economy. These are the most credit-dependent parts of the consumer-driven economy. With the moves already made, we are in for a period of adjustment as consumers deal with interest rates not seen since 2007. And for those with less-than-perfect credit, financing big-ticket purchases is becoming impossible.

By raising rates, the Fed has forced lenders to follow. Meanwhile, consumers who are most payment sensitive are falling out of the market, and that makes the subprime share fall.

While the rate movement from the Fed has priced them out of the market, deteriorating economic prospects are also causing lenders to gauge risk as higher.

As a result, rate increases for these would-be borrowers are even larger than the Fed’s movements because the yield spread on riskier loans, like loans for used cars and especially to subprime borrowers, is widening, making those interest rates even higher.

Credit Squeezing Buyers

Credit is still available, but it is flowing to a smaller portion of the population, which means demand is shrinking. The consumer has limited ability to get a payment they can afford as they cannot adjust the remaining variables enough to keep payments within reach.

The Fed cannot directly influence inflation in the auto market without damaging the industry. With low supply in the new market, prices are still going up. Higher rates will not resolve semiconductor shortages, COVID lockdowns in China, or production challenges.

The Fed can claim some credit for the deflation we are seeing in the used market, but that was inevitable. Vehicles are naturally depreciating assets. Last year’s stimulus-induced demand frenzy that led to historic used-vehicle price inflation had already shifted to normalized supply and declining prices at the start of 2022. Simply put, used-vehicle prices were declining before the Fed’s first rate hike in March.

But with the aggressive rate moves and rhetoric this summer, demand has fallen more than it would have naturally. As a result, the retail and wholesale used markets have been oversupplied this summer, leading to more than 10% declines in wholesale prices over the last 100 days. Retail prices have not decreased as much as wholesale, but they likely will this fall.

Q: Buy Before Rates Rise Again or Wait for Prices to Drop?

Consumers now have a dilemma: race to buy before rates go even higher or wait for prices to fall. When the payment is what matters, it is an impossible choice. The market is in for a payment affordability reset, and affordability will get worse before it can get better.

The dynamics in housing are very similar, and the mortgage market has been far more reactive than the auto loan market. Before the most recent rate hike, the average 30-year mortgage rate had already increased by 3.2 percentage points.

The term length of a loan determines the impact of a change in rates on the average payment. The longer the loan term, the greater the payment inflation. A 1-point change in a 30-year mortgage has a 12% impact on the average payment, all other factors equal. A 1-point change on a 6-year auto loan has a 3% impact on the average payment.

Therefore, past rate movements hurt the real estate market more than the auto market. That 3.2 percentage point change in mortgage rates has caused a 38% increase in the average payment from interest rates alone. That effect is evident in the home sales data; existing home sales have fallen for seven consecutive months.

So far in September, the average auto loan rate has increased by about two full percentage points for the year. That means the average payment has increased by 6% due to interest rate changes alone.

With the latest increase and an additional 1.25 points before year-end, financing costs will make purchases more challenging with at least a double-digit increase in hypothetical monthly auto loan payments.

Despite this headwind, with continued limited new-vehicle production because of supply chain challenges, there is no evidence yet of demand destruction in the new market. It is the used market that is the canary in the coal mine.

Higher Interest Rates Meet Supply Chain Constraints

With additional rate increases expected by year-end, new-vehicle demand may not hold up when production and product availability improve. That could mean the market will likely see the return of discounting and incentives. If that does happen, the Fed will claim victory over inflation in all parts of auto.

However, it is not a given that higher rates will lead to lower new-vehicle sales, especially as the market remains supply-constrained and shifts to producing more electric vehicles. As the new market has become more concentrated in higher price points, the industry benefits from primarily selling to higher income and higher credit quality buyers who are less likely to lose jobs in recessions and enjoy much lower rates when they choose to finance. With prices at record highs and rates heading higher, the new-vehicle market will behave like a de facto luxury market for the foreseeable future.

The other concern arising from the Fed’s aggressive plans for the rest of the year is that odds now favor a recession occurring in 2023. Stocks are on the decline in response. Therefore, even well-heeled new-vehicle buyers may pull back in the short term. When housing looks less strong and stock portfolios decline, the wealth effect depresses even luxury buyers. And that is more bad news for an already fragile new-vehicle market.

Jonathan Smoke is the chief economist at Cox Automotive.

Originally posted on Vehicle Remarketing

More Remarketing

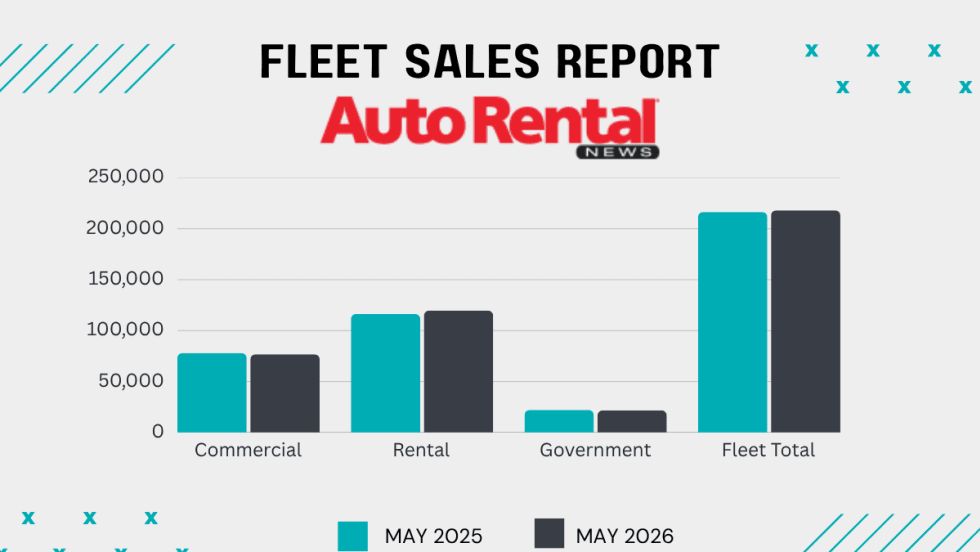

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

Surprice Opens Two Rental Branches In Japan

The launch highlights the global car rental operation’s growing presence in Asia.

Read More →

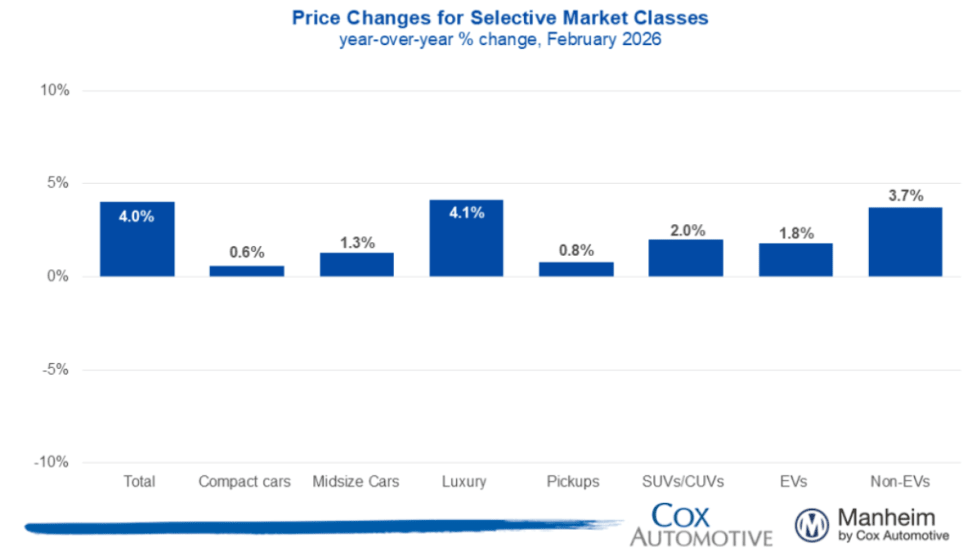

Wholesale Used Vehicle Prices Up In February

Solid demand at Manheim auctions with higher sales conversion rates indicate an appetite from dealers to buy.

Read More →

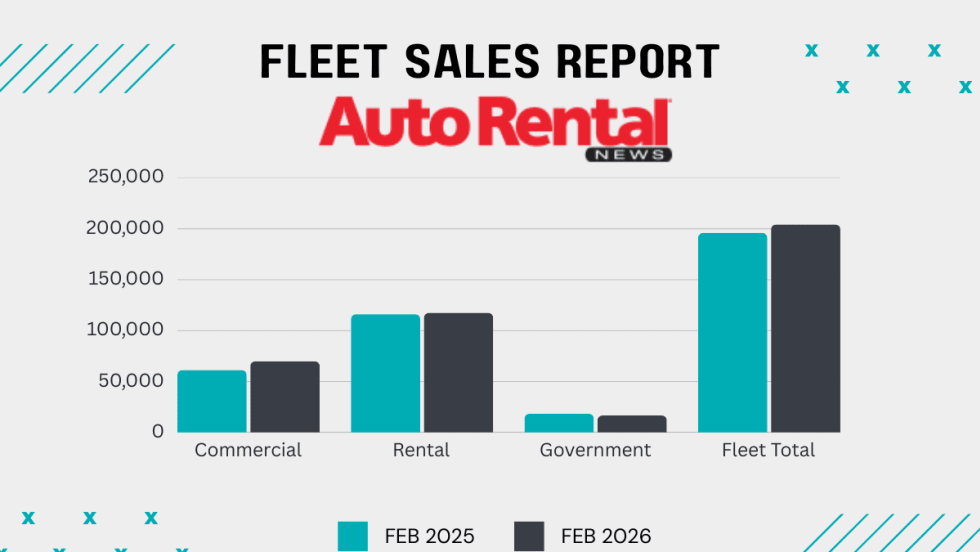

Rental Fleet Sales Slow In February Ending A Strong Streak

Commercial fleets posted the most gains, sustaining increases in monthly and year-to-date fleet sales

Read More →

Avis Budget Group Reports Near $1 Billion Loss Tied To 2025 EV Fleet Write-Down

Following Hertz, the company is the second global car rental conglomerate to sustain sizable losses due to lower customer demand and usage of electric rental cars.

Read More →

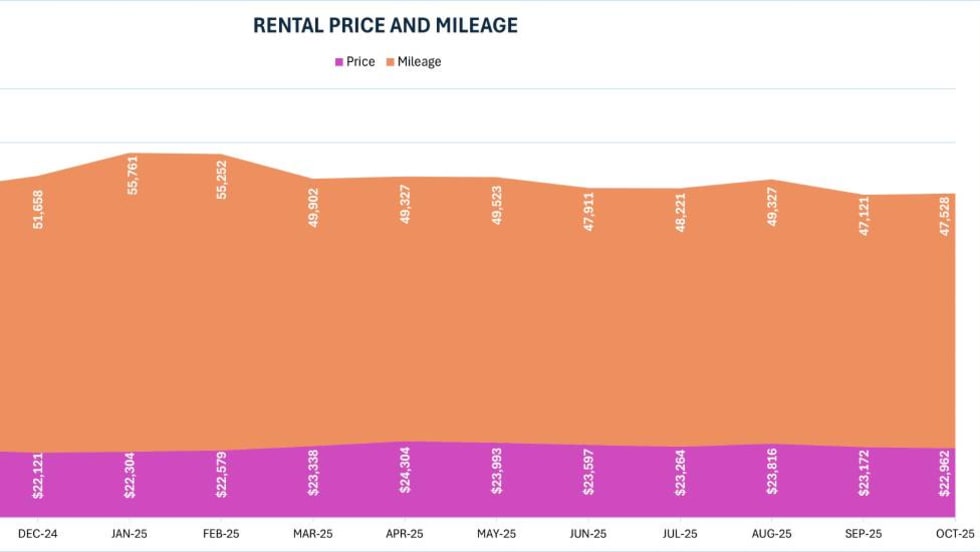

2025 Rental Vehicle Remarketing Summary And Outlook

The year brought modest and flatter results across wholesale values, total off-rental supply, and rental risk units.

Read More →

Auctions Record Highest Vehicle Sales Since 2019

2025 figures show a steady recovery in wholesale vehicle activity this decade.

Read More →

DriveItAway Holdings, Free2move Launch Operations In Nine Cities

The co-branded program with Stellantis’ mobility division scales up leasing and financing options nationwide with more cities to come online in 2026.

Read More →