Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) decreased 2.7% from March in the first 15 days of April, according to the midmonth Manheim Used Vehicle Value Index released April 18, which dropped to 231.7 and was down 4% from April 2022.

The seasonal adjustment contributed to the decline. The non-adjusted price change in the first half of April was an increase of 0.6% compared to March, while the unadjusted price was down 5.1% year over year.

During the last two weeks, Manheim Market Report (MMR) prices were mostly unchanged. Prices usually start to decline in the first two weeks of April, as the average price change for these weeks in the six years from 2014 through 2019 was a decline of 0.3%. But in each of the last two years, prices increased substantially over these same weeks. During the first 15 days of April, MMR Retention, the average difference in price relative to current MMR, averaged 99%, indicating that valuation models are ahead of market prices. The average daily sales conversion rate of 61.4% in the first half of April declined relative to March’s daily average of 64.9% and was below the April 2019 daily average of 63.6%.

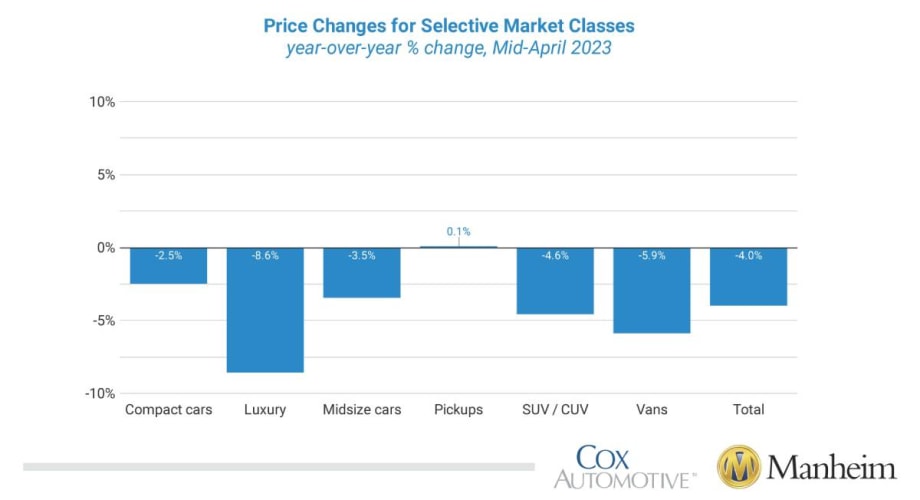

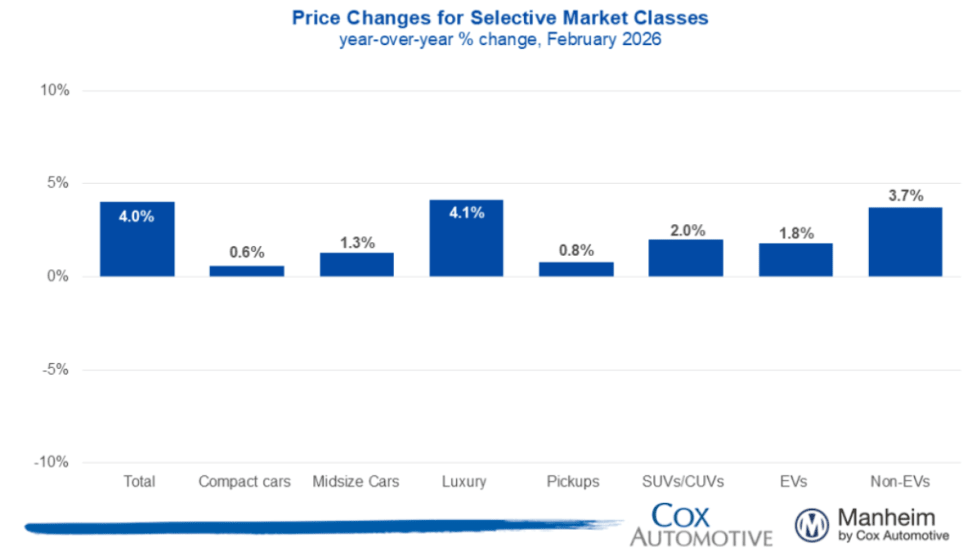

Seven of eight major market segments saw seasonally adjusted prices that were again lower year over year (YOY) in the first half of April. Pickups had a minimal 0.1% increase, while only midsize and compact cars lost less compared to the overall industry in seasonally adjusted year-over-year changes. The remaining segments lost between 4.6% and 8.6%, with luxury units again faring the worst. Seven of eight major segments saw price decreases compared to March, with losses ranging from 1.2% to 2.9%. Sports cars again were the lone exception, this time with a 1.4% increase from March.

Retail Supply Normal in Mid-April

Using estimates based on vAuto data as of April 10, used retail days’ supply was 40 days, unchanged from the end of March. Days’ supply was down nine days YOY and unchanged compared with the same week in 2019. Leveraging Manheim sales and inventory data, Manheim estimates that wholesale supply ended March at 22 days, down two days from the end of February and down one day year over year. As of April 15, wholesale supply was at 24 days, up two days from the end of March, unchanged year over year, and three days lower than in 2019. Used supply measured in days’ supply and compared to 2019 suggests supply is close to normal for this time of year, which indicates demand and supply are relatively balanced despite low inventory levels.

Rental Risk Prices Increase in First Two Weeks of April

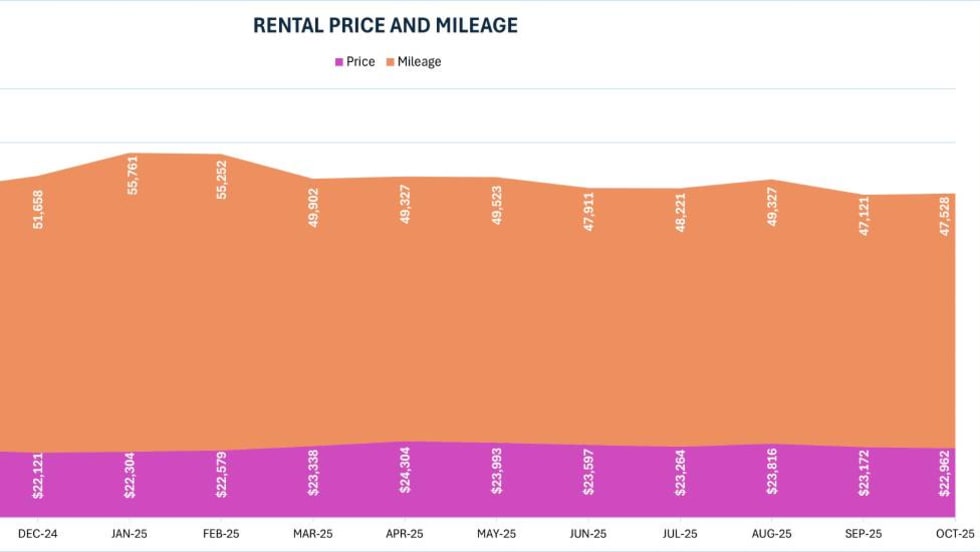

The average price for rental risk units sold at auction in the first 15 days of April was up 5.1% YOY. Rental risk prices were up 2.4% compared to March. Average mileage for rental risk units in the first half of April (at 58,700 miles) was down 8.8% compared to a year ago and down 9.4% month over month.

Tax Refunds in 2023 Down Compared to Last Year in All Key Metrics

While the 2023 tax refund season started faster than last year in terms of distribution of refunds, 2023 is now behind 2022 on all key metrics. With statistics through the week ending April 7, $199 billion in refunds have been issued. The number of refunds issued is down 1% from last year, 11% less has been disbursed than last year, and the average refund at $2,878 is down 9% YOY.