2025 Rental Vehicle Remarketing Summary And Outlook

The year brought modest and flatter results across wholesale values, total off-rental supply, and rental risk units.

At the end of October, prices are slightly higher than at the same time in the previous three years, despite spending most of the year below 2023 and 2022 levels.

Credit: Cox Automotive

For most of 2024, wholesale values continued to correct from their 2021 peak, with the Manheim Used Vehicle Value Index ending December 2024 up 0.4% year over year, slightly below the typical observed rate.

The year began with significant year-over-year declines and depreciation rates higher than those typically observed in the first half of the year.

However, the declines became increasingly muted as the year progressed, eventually turning positive by year-end, as the contraction in lease maturities reduced wholesale market supply.

New-vehicle sales were quite strong at the end of the year, bolstering used-vehicle sales and creating some scarcity in the wholesale market.

The first quarter of 2025 maintained this modestly positive trajectory, with values hovering slightly above prior-year levels. Then in spring, the wholesale market experienced a notable surge.

From April through June, values increased sharply as tariffs raised wholesale prices, pushing new-vehicle prices higher, with year-over-year gains peaking at 6.3% in June. This represented the strongest period of growth since the post-pandemic peak began unwinding.

However, that strength soon waned, and the market cooled through the summer months, with July and August showing more moderate gains of 2.9% and 1.7%, respectively.

By fall, the momentum had largely evaporated. September held at 2% year over year, but October saw a sharp monthly decline of 2%, bringing the year-over-year comparison to essentially flat.

The wholesale market remains relatively tight relative to the longer-term run rate, as measured by days’ supply. Current days’ supply at Manheim sits at 27.3 days, less than last year’s level of 28.4 days.

Looking at segment performance, there’s clear divergence: luxury vehicles and EVs continue to show strength (up 3.6% and 3.9% Y/Y, respectively, in October), while traditional sedan segments—particularly compact and midsize cars—are experiencing notable declines of 6.5% and 4.6%.

These factors have led to a forecast that vehicle values will be only 0.5% higher at the end of 2025, with a more normal increase expected by the end of 2026. The market typically rises by about 2% per year due to the inflationary effects of new vehicles entering the wholesale market over time.

Sales into rental are estimated to be 14% higher than last year for the rental segment of the fleet, but this hasn’t translated into a higher volume of wholesale rental disposals.

Credit: Cox Automotive

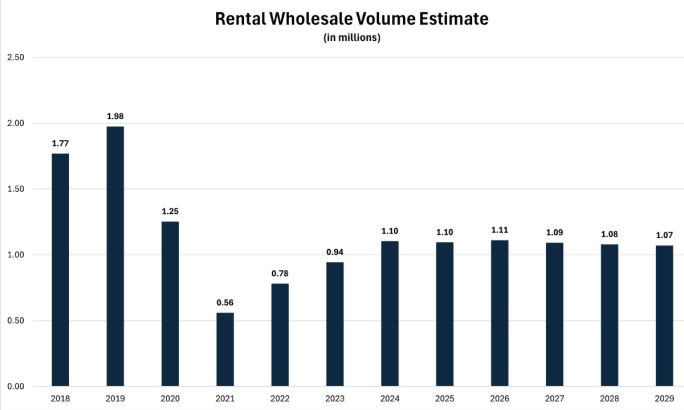

Total Wholesale Supply Off-Rental (Rental Wholesale)

Rental companies have had more options to purchase new fleet vehicles in recent years due to increased supply, which has enabled the disposal of rental units into wholesale markets and contributed to a rebound in recent years.

Rental volumes in wholesale markets increased by about 17% in 2024, although we have seen a slight slowdown in this segment in 2025. Sales into rental are estimated to be 14% higher than last year for the rental segment of the fleet, but this hasn’t translated into a higher volume of wholesale rental disposals, according to Bobit Business Media data.

As we’ve seen in key dealer segments, more used-vehicle operators are adjusting how they source and sell units, and the impact of tariffs means operators can retail a higher proportion of used vehicles rather than bring them to auction.

While new rental fleet purchases are much higher, we expect wholesale volume to decline by almost 1% for the full year 2025 before rising modestly in 2026.

Rental car companies have many more options for disposing of end-of-service units and are continually innovating their disposal methods.

We believe that growth in the direct-to-consumer channel will continue to limit the flow of those units into the wholesale channel.

Rental wholesale volumes are projected to grow from about 1.1 million units in 2025 to a peak of about 1.1 million in 2026 before gradually declining to just over 1 million by 2029.

While this represents stability in the near term, these volumes remain well below the two million units we saw in 2019, reflecting the structural shift in how rental companies are managing

fleet disposition.

The balance between wholesale and direct-to-consumer channels will continue to evolve as companies optimize their remarketing strategies.

Rental Risk Units: Average Auction Price / Mileage

Wholesale prices for rental risk units have remained above pre-pandemic levels, showing more movement this year than in the previous year.

At the end of October, prices are slightly higher than at the same time in the previous three years, despite spending most of the year below 2023 and 2022 levels.

Overall, rental price trends have followed a pattern similar to that of the used-car market, rising in the early part of the year before trending downward more recently.

Prices are not expected to fall meaningfully in 2026 and are expected to follow the overall wholesale market, with a stronger-than-normal spring rebound anticipated due to a stronger-than-normal tax refund season.

Mileage bands for rental risk units run through auctions shot higher at the start of 2025 but have since been trending down and now sit below last year’s levels at this time. This is the lowest mileage reading for this time of year since 2020, though it remains above pre-pandemic levels. This drop in mileage is most likely due to an increase in younger model-year vehicles entering auction after the post-pandemic period, when much higher-mileage units were prevalent.

However, rental companies have multiple options for disposing of units, and consignors are expected to continue retailing a greater percentage of the lowest-mileage risk units rather than sending them to auction. This shift in practice should keep auction units’ mileage higher than the overall average.

This article originally appeared in the print edition of the 2026 ARN Annual Fact Book.

More Remarketing

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

Surprice Opens Two Rental Branches In Japan

The launch highlights the global car rental operation’s growing presence in Asia.

Read More →

Wholesale Used Vehicle Prices Up In February

Solid demand at Manheim auctions with higher sales conversion rates indicate an appetite from dealers to buy.

Read More →

Rental Fleet Sales Slow In February Ending A Strong Streak

Commercial fleets posted the most gains, sustaining increases in monthly and year-to-date fleet sales

Read More →

Avis Budget Group Reports Near $1 Billion Loss Tied To 2025 EV Fleet Write-Down

Following Hertz, the company is the second global car rental conglomerate to sustain sizable losses due to lower customer demand and usage of electric rental cars.

Read More →

Auctions Record Highest Vehicle Sales Since 2019

2025 figures show a steady recovery in wholesale vehicle activity this decade.

Read More →

DriveItAway Holdings, Free2move Launch Operations In Nine Cities

The co-branded program with Stellantis’ mobility division scales up leasing and financing options nationwide with more cities to come online in 2026.

Read More →

Tariffs, Digital Tech, Industry Stats Among Top 10 Remarketing Topics for 2025

The annual look at most-consumed vehicle remarketing content shows what audiences think mattered the most in the mid-decade year.

Read More →