Like-Kind Exchanges Kind to Business's Pocketbooks

There is the potential to spend less money on taxes and more money on fleets. A panel at the September Car Rental Show explored the benefits of like-kind exchanges and the tax deferment options that they carry.

Brent Abrahm, Accruit co-founder and executive vice president, joined by presenters Marty Verdick, managing director of RSM McGladrey Inc. and Chuck Aton, CEO of SVI, an independent franchise of National Alamo Car Rental, led a panel discussion aimed at conveying the benefits of repetitive like-kind exchanges for those in the car rental industry.

Frequently used in real estate, like-kind exchange (LKE) is a process where a business disposes of one asset (in this case a vehicle) and acquires another similar asset in the same class while allowing the funds to flow through a third-party individual known as a qualified intermediary. The business then defers income tax on the transaction. Since 1921, Congress has allowed the deferral of gain on exchanges of this sort using Section 1031(a) of the Internal Revenue Code, however, it is just now beginning to be used in the car rental industry.

According to the panel, though, the benefits of a like-kind exchange for rental car companies are simple — they can avoid paying a 40% tax on the gain earned from selling and buying vehicles and use the capital saved to pay down interest on loans or to purchase more vehicles instead. “Depending on your buying and selling patterns, and if you’re growing your fleet or not, you can defer taxable income almost up to the average cost of your fleet over time, which at a 40% tax rate could be a substantial advantage,” Aton said. “Will that bill ever come due? Sure it will, but at that point you may be selling your business.”

RSM’s Verdick used his time to try and simplify for the audience just how a like-kind exchange works when trading assets other than real estate. Verdick said that vehicle trades can be considered like-kind property as long as they fit within the same asset classes specified under section 1031 of the IRS code or within the North American Industry Classification System (NAICS). The latter, part of the U.S. Census Bureau, replaced the U.S. Standard Industrial Classification (SIC) system in 2002 as a tool to compare statistics of North American business activity. “As long as we’re trading assets in those general asset classes, that is like-kind property,” Verdick said. “So, trading a car for a car is like-kind, but trading a car for a light duty truck is not, because those are in two different general asset classes. Once we stay in the same general asset class, though, we’re good.”

The more complex rules associated with like-kind exchanges were then addressed, such as the necessity for car rental companies to identify within 45 days the replacement for their relinquished vehicles. The panel discussed the IRS’s need for this identification process to be “unambiguous,” meaning that it has to be put into writing and made to be as specific as possible, such as identifying the make, model and year of the vehicle.

“The regulations give us some guidance in this. For instance, if you actually acquire the replacement property within the 45-day period then you’d be deemed as satisfying this identification process, as well,” Verdick said.

Other parameters for LKEs were discussed, as well, such as the need for replacement property to actually be received before a 180-day period has lapsed. Also mentioned were the due date of a company’s tax return, and the fact that a qualified intermediary is generally used to complete the exchange to avoid constructive receipt of the sales proceeds. [PAGEBREAK] During the presentation, Abrahm and Verdick also examined a qualified intermediary’s ability to redistribute cash. Money that would normally go toward paying the IRS its 40% can be used to sweep against a line of credit they may have with a finance house, a process known as funds netting. That would help pay down the interest and make funds available for vehicle purchases. Since there are other options available for qualified intermediaries, such as a joint account with the taxpayer, it is important for a licensee and the qualified intermediary to be on the same page when it comes to deciding what to do with the funds earned from selling vehicles.

The panel stressed that licensees must adhere to the rules of repetitive LKEs that are laid out in revenue procedure 2003-39 to receive its potential benefits. If the cycle of buying and purchasing is snapped, or the company deviates from any of the safe harbor guidelines that 2003-39 provides, a company would be forced to come up with the 40% tax that LKEs are helping it avoid.

The savings that LKEs can generate are often tremendous. As Aton said during his first-person account of somebody who actually uses the system, a company that runs a $10 million fleet could possibly be saved from paying $4 million in potential taxes, using the additional resources to add to its fleet instead. “With interest rates and car costs creeping up, your competition is embracing some of these programs, and that’s going to reduce their costs,” Aton said. “So take a look at it, investigate it, and make your own decision, but definitely get some tax planning advice along the way, as well.” At his rental facility, which implemented the LKE program in March, Aton added that it has been a seamless process once the software program was established, and his support staff was trained with it.

Likewise, Verdick said that Accruit’s software program has helped him, as a tax practitioner, relieve the headaches that LKEs used to cause when they were strictly a form-driven operation. “If you trade your vehicles every year, you can have as many as five or six layers of depreciation on your depreciation schedule for each and every vehicle,” Verdick said. “If it’s one car, two cars, three cars it’s not a big deal. But, if you’re trading thousands of cars a year, the process of maintaining the actual depreciation numbers, with all the layering, can be very, very difficult. That process is much easier now that companies like Accruit are creating software to do just that.”

Prior to wrapping up their discussion and opening up the floor for the Q&A portion of its presentation, the panel said that instituting an LKE could be extremely beneficial since many companies that took advantage of bonus depreciation, ended in December 2004, spent their monies elsewhere. They are now scrambling to find capital to pay their taxes. A problem, they argued, that would be rare if companies took advantage of like-kind trading and made the right choices for their tax deferments.

More Remarketing

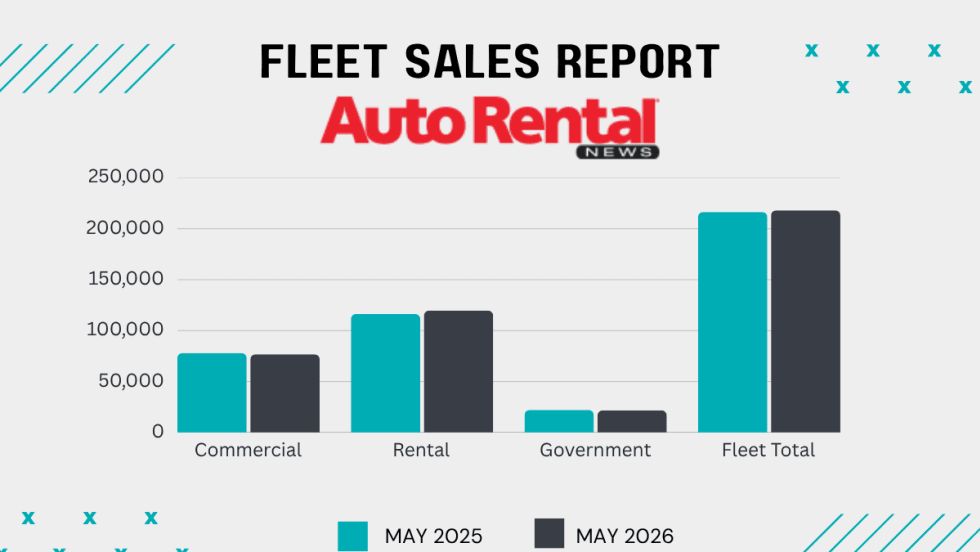

Rental Fleet Sales Skating Just Above 2025 Levels

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

Cross-Pressures, Evolving Trends Drive 2026 Rental Car Industry

A combination of cautious economic behavior, shifts in the rental vehicle market, and technological influences are shaping car rental operator decisions.

Read More →

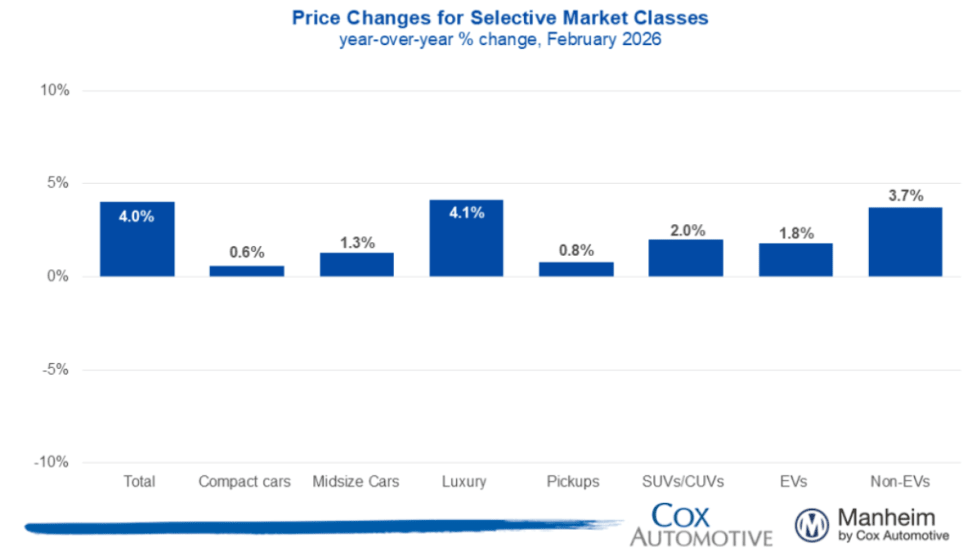

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

Surprice Opens Two Rental Branches In Japan

The launch highlights the global car rental operation’s growing presence in Asia.

Read More →

Wholesale Used Vehicle Prices Up In February

Solid demand at Manheim auctions with higher sales conversion rates indicate an appetite from dealers to buy.

Read More →

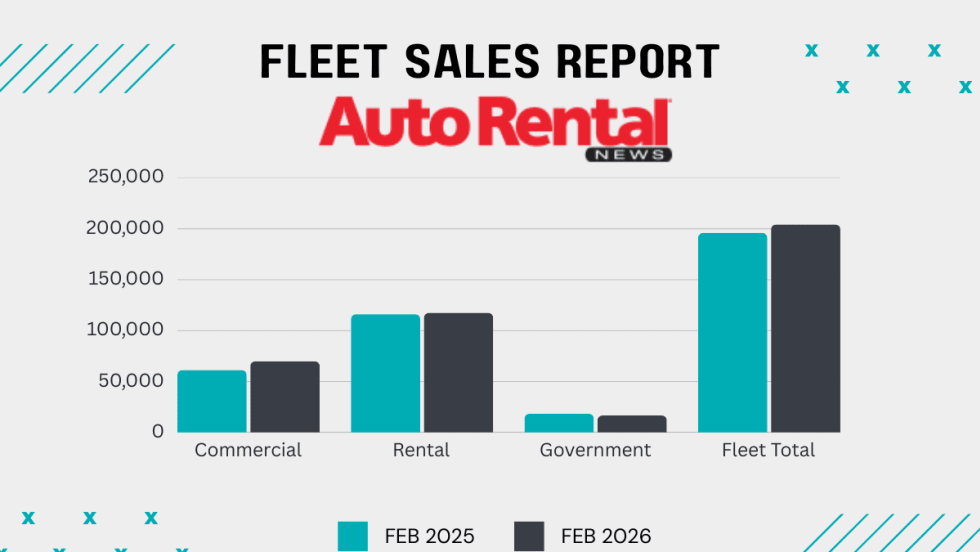

Rental Fleet Sales Slow In February Ending A Strong Streak

Commercial fleets posted the most gains, sustaining increases in monthly and year-to-date fleet sales

Read More →

Avis Budget Group Reports Near $1 Billion Loss Tied To 2025 EV Fleet Write-Down

Following Hertz, the company is the second global car rental conglomerate to sustain sizable losses due to lower customer demand and usage of electric rental cars.

Read More →

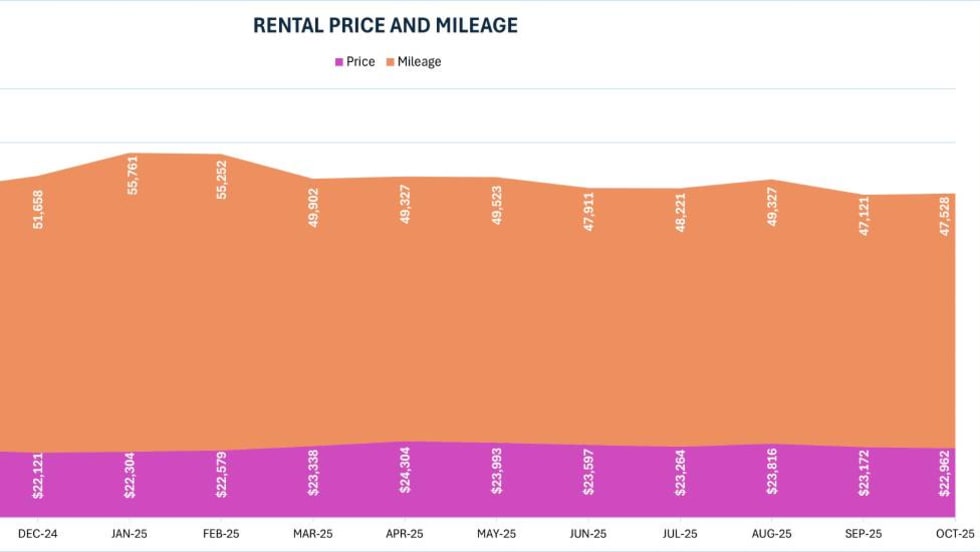

2025 Rental Vehicle Remarketing Summary And Outlook

The year brought modest and flatter results across wholesale values, total off-rental supply, and rental risk units.

Read More →

Auctions Record Highest Vehicle Sales Since 2019

2025 figures show a steady recovery in wholesale vehicle activity this decade.

Read More →

DriveItAway Holdings, Free2move Launch Operations In Nine Cities

The co-branded program with Stellantis’ mobility division scales up leasing and financing options nationwide with more cities to come online in 2026.

Read More →