ACE Rent A Car has been experimenting with forms of prepaid reservations since 2011. Here's what worked best.

by Kevin Stutz

May 8, 2017

4 min to read

ACE Rent A Car took its first prepaid booking in the fall of 2011, and in the almost six years since, prepaid reservations have become a central part of how we do business.

Through recent experimentation, we began to wonder if, instead of asking customers to pay less to commit to a reservation, perhaps we should be asking them the opposite — pay more not to commit.

Ad Loading...

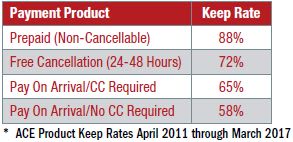

But first, some definitions and a little history for context: A prepaid reservation is a fully prepaid, non-refundable reservation; a deposit reservation comes with refund rights; with a pay-on-arrival reservation the customer pays in full at the counter.

Typically, prepaid reservations are offered at a percentage discount off an operator’s retail price. A keep rate, as ACE calls it, is the percentage of gross bookings that become a contract. Lastly, we measure no-show rate as a percentage of gross reservations.

Prepaid Experiments

In our first full year of offering prepaid reservations (2012), ACE saw its overall no-show rate decrease 40% year-over-year, falling from 20% all the way down to 11% of gross reservations.

Sure, no-show and cancellation rates tend to average out over time, but nevertheless, no-shows had always been a nuisance, and these results convinced us that we were on to something.

How much of a discount would it take to convince customers to book a prepaid reservation? Our data showed that when a customer was presented with an option between a cancellable reservation and a non-cancellable reservation at a 5% discount, the customer forfeited their cancellation rights 50% of the time in order to save money.

Ad Loading...

We’ve seen these forfeiture numbers climb as high as 85% when presented with a 10% discount. Bottom line: it doesn’t take much to get customers to commit.

Fast forward to 2016: Pay Now, as we now call it, is an almost universal part of our industry. A quick scan across brand and OTA websites, and you’ll find discounts ranging from 10% to — gulp — 40% off the retail price.

Due to the increasing discounts, we started to question if the trade-off of getting a guaranteed booking was worth further discounting already tumbling prices. That’s when we started to look at other data points like customer service and chargebacks.

We found that about 6% of ACE customers who booked a prepaid reservation in 2016 reported an issue with the customer care department. Further, the 2% that booked a prepaid reservation ended up filing a chargeback with their credit card company. In 2016, ACE lost approximately 50% of these chargebacks as the merchant of record.

Product Analysis

This was no doubt a startling revelation to us, so in the fall of 2016, ACE started to experiment with two new products: Free Cancellation, a full deposit product with a 24-hour cancellation policy at market price, and Pay On Arrival, a credit card-required product with no penalty at a 5% markup from our market price.

In the first quarter of 2017, the data collected on these two new products was quite compelling.

Ad Loading...

When presented with a side-by-side option, customers elected to pay ACE 5% more than our market price product 46% of the time for the right to pay on arrival. When presented with a list view, this number declined to 31% of customers.

Only 0.8% of customers reported an issue with customer care on these new products when compared to the prepaid predecessor, and less than .10% of these reservations have ended up in a chargeback status.

Here’s how the products’ keep rates have performed over the last six years:

The data demonstrates that we can influence the likelihood of keeping a reservation with payment products, but at what point is the benefit of an improved keep rate outweighed by the problems that come with trying to improve it?

The solution is to keep exploring the messages our customers send us through data.

Ad Loading...

Observations

Don’t be afraid to lose gross reservations: It’s true, the more we require from our customers, the less likely they are to book. Yet in general, all it will cost are those customers who weren’t going to show anyway.

Here are my observations:

• We need better disclosure of terms: The customer issues we experienced with our prepaid product had more to do with our failure to communicate terms and with market inconsistency than it did with problems with the product itself.

• Customers like flexibility: So much so, our data shows, that customers are willing to pay more for it.

• Display matters: How our industry and OTAs display prepaid products has an enormous impact on the effectiveness of higher priced, flexible products.

Ad Loading...

• The markets are different: Prepay and post-pay are not the same.

West Coast disasters pose unique challenges and liabilities for rental fleet operators, who are advised to take steps tailored to their specific situations.

Angry car renters are storming social media, the mainstream media, and online ratings platforms to complain about charges they claim are either unfounded or excessive.

Revcuity, an outgrowth of Frontline Performance Group, aims to help clients capture more revenue moments with face-to-face customers, including in the car rental space.

Martin Romjue has been editing and reporting for ARN since 2023 and fully transitioned to the role of chairman of the International Car Rental Show in 2026.