See More: Photo Highlights: 2022 International Car Rental Show

ACCRO's Craig Hirota Recaps 2022 ICRS

The vice president of the Canadian car rental association puts into context the dynamics of the industry going into the event, the overall attendee atmosphere at ICRS, and his takeaways from the seminars.

by Craig Hirota

May 6, 2022

Panel members attempted to look in their crystal balls on Tuesday's breakfast keynote to assess the incredible challenges around vehicle supply.

Photo: Ross Stewart, RMS3Digital

10 min to read

I was very excited to attend this year’s show. The International Car Rental Show has always been the single best opportunity to get a read on the types of industry trends, challenges, and innovation percolating among the operators and innovative suppliers in the industry.

In the years preceding 2019’s show, there was a growing participation from outside North America, bringing even more diversity and innovation to the forefront. With the travel and gathering restrictions imposed by the pandemic, the three years between ACCRO’s attendance has felt like operating within a silo.

While video conferencing and the internet have served as useful proxies, there is no substitute for the gatherings of peers and the organic sharing of ideas available at the International Car Rental Show.

As a side note, despite some forecaster’s predictions that business travel will never return to pre-pandemic levels, I believe many businesses will soon re-experience the outsized returns on travel investment from seeing customers and employees in person compared to remote contact pandemic-era workarounds.

My plans for attendance at this year’s show was to attend as many sessions as possible to report back to ACCRO membership. In previous years, there would be participation from as many as 10 or more Canadian operators, a number of suppliers, and a contingent of ACCRO representatives including our partners at Baird MacGregor.

With Canada still emerging from pandemic lockdowns, a sixth wave of COVID, incomplete vaccination among young children, and the exposures to potential health care expenses in a foreign country, representation from Canada and ACCRO at this year’s show was at historically low levels.

A comparison of the 2022 schedule to the schedule from the last show ACCRO attended in 2019 is a reminder that in the current era of 100-year black swan events occurring on a quarterly basis and the always incredible pace of technological innovation, three years is a long time.

In 2019, one session profiled a relatively new On-Demand mobility provider Virtuo (est.2016). In this year’s show, Karim Kaddoura, Virtuo’s co-founder, announced his fleet was up to 7,000 vehicles with growth constrained by the common industry refrain, vehicle supply.

Another topic from 2019, “The Connected Rental Car and the New Data Economy” discussed the potential risks and benefits of in-car generated data. At this year’s show, there were multiple sessions about using in-car generated data to optimize operations and multiple exhibitors including session participants and show sponsors like Zubie, RENTALL Software, Rent Centric, and Geotab now have years of data working with fleets and case studies showing meaningful return on investment.

The 2019 schedule included multiple sessions addressing daily operational or employee/rental counter issues that represented the top-of-mind concerns of the industry at that time. Sessions from 2019 included maximizing profit and sales, customer identification and retention, and managing insurance risks.

Perhaps reflecting three years of the rental industry adapting on the fly to one global macro event after another, 2022’s schedule focused on forecasting trends in fleet availability and residual values, new technology, and the impending EV transition with minimal attention on day to day operational issues at the employee/counter level. In fact, a number of the sessions and the trade show exhibit hall featured suppliers that offer solutions that bypass the rental counter and most employee/customer interactions altogether.

Seminar Takeaways

Car Rental, an Investment View

This session was led by John Healy, analyst, Northcoast Research. He provided an overview of investor’s observations on the industry. My takeaways from the session were that it appears the investing community believes publicly traded companies’ statements on exercising fleet growth discipline and operating a profitable business are sincere but that forecasting demand is very imprecise and could still lead to potential over-supply situations and corresponding softness in the current strong pricing environment.

Car Rental 101 for 2022 and Beyond

Like the session on Sunday, this session was very well attended. It was one of the first signs that there has been an amazing amount of pent-up demand for information among industry participants. These early sessions also started a continuing theme throughout the show of high participant engagement. The Q&A periods at the end of each session I attended were almost always timed out rather than ended due to a lack of questions.

Mark Paley and Alex Aryafar discussed how car rental operators can access a specific “car rental” payment rate structure via payment processors. Perhaps this is not news to many of our members but it was news to me. Apparently if the payment processor gets access to additional information (invoice number, beginning and ending time/date of the contract) there is a lower rate available than the standard retail transaction rate. Ballpark range for discounts on the rate of approx. 0.3%.

First Timer’s Orientation

I attended this session even though this was my 10th ICRS because I wanted to be able to give ACCRO members who have never attended an ICRS an idea of what to expect. Much of the session was devoted to promoting the benefits of joining the American Car Rental Association (ACRA), an important opportunity for US operators to participate in necessary government relations.

The biggest takeaway from the session for me and other international attendees was the ice breaker activity where, in a “speed dating” format, we had the opportunity to meet with other operators for 5 minutes at a time. To be honest, five minutes wasn’t enough, there was just so much to share and learn about operators in different markets and at different levels of business development.

If attendees weren’t already tuned into the value in the collaborative opportunities afforded by the ICRS, the ice-breaker activity drove that point home. Many attendees were still chatting with others even after the session was over.

Electric Cars are Coming, Are We Ready?

While the session panelists were US based and did a great job presenting the challenges in building out customer demand and EV support infrastructure from a jurisdictional perspective, the over-riding message that growing utilization of EVs necessitates forward thinking at many levels resonates. Another great takeaway from the session was Ben Prochazka’s announcement that a research report on a public private partnership for rental EVs in Orlando was now available for review. ACCRO members currently renting or planning to rent EVs can access the report here. The session also provided ample evidence that there are likely to be very stark differences, regionally and politically, in terms of the acceptance of and the adoption of EVs.

Opening Keynote Address: Preparing for the New Mobility Landscape

This session was notable because Europcar announced not just the purchase of Fox Rent A Car but also Europcar’s intent to enter the US market under the Europcar brand. Europcar, like the existing major rental car corporations already in North America, presents a variety of product offerings for various market segments. My initial thoughts wondered if growing populist and ‘buy American’ trends will clash with a brand so heavily anchored to a foreign geography.

Overcoming Operational Challenges to Renting EVs

Main takeaways from this session were the infrastructure challenges with building out a proper charging facility for airport locations (CONRACs or Consolidated Rent A Car facilities) and for standalone rental facilities. There are extremely high costs to install the necessary DC Fast Chargers for rapid turnaround of EVs and the potential need for accommodations by utility providers to address high peak power demands.

In addition, there are even potential legal pitfalls surrounding contractual recovery of charging fees that don’t exist with current fuel charges (related to regulatory restrictions on what entities can sell electricity). Perhaps instead of recovering electricity, the industry will need to bill for loss of use equivalent to the time/power needed to recharge if an EV is returned with less than the required amount of charge capacity.

How Car Rental Can Leverage OEM Data

This session was a glimpse into the near future. Most, if not all, new vehicles produced today have some degree of over-the-air connectedness. Some manufacturers are already marketing this data to fleet operators. This session described how rental management systems, connectivity platforms, and OEMs are working together to provide much more value add than simply geolocation data. My own personal takeaway from this session and other similar sessions is the potential uses of in car data to reduce insurance risk or to potentially increase residual value by eliminating the justification for “previous daily rental” declarations on the sale of vehicles.

A Data-Driven Approach to Future Fleet Valuations

This session presented the benefits of leveraging in-car data with real-time vehicle residual data to provide extreme accuracy in fleet management decisions. The key takeaway from this session was how operators using the combination of in-car data to track mileage and unit residual values (via linkage with vehicle sales databases) can maximize cost to carry decisions or utilize fleet vehicle equity to leverage additional financing from one’s lenders.

Fleet Outlook Roundtable

Very interesting session on fleet residual forecasts. Panel stressed that there is a cumulative multi-year supply deficit of new vehicles and that even if the OEMs are able to resume production at the peak of pre-pandemic levels, it would still take years to address the over 7.5 million vehicle deficit that currently exists and growing by the quarter. They also stressed that the situation will get worse in 2024 and 2025 since there were very few leased vehicles in 2021 and 2022. The supply of near new, off lease vehicles in 2024 and 2025 will be near zero placing additional strain on new vehicle availability. The panel felt very comfortable that used vehicle residual values would weaken in a very gradual manner giving fleet operators plenty of margin to adjust fleet mix in the coming years.

Telematics, EV’s, and Other Pressing Topics in Vehicle Rental Law for 2022 and Beyond

Main takeaways from the customary legal session are know your state/provincial/federal laws and disclose to your customer anything relating to charges, fees, collection of data, or the presence of tracking or monitoring devices.

How to Scale Contactless/Keyless Solutions in Your Operations

Keyless/contactless rental management is evolving to become minimally invasive to preserve vehicle warranties. Thoughtful integration of keyless systems and rental management systems can provide opportunities for virtual rental “offices” and location-free rental operations.

Winning Customer Payment Disputes the Smart Way

Main takeaway was the reinforcement that it is imperative to utilize the chip and PIN capability whenever possible. Apparently this isn’t as widespread in the US as it is in Canada but it pays to be reminded of it. The panelists stressed that if the chip and PIN is not used when the card is presented, if the customer were to subsequently dispute the charge on fraud grounds, the charge is always reversed. If chip and PIN is used, the credit card issuer accepts that the card was present at time of charge and that the cardholder was the user.

Closing Keynote Panel: The Future of Car Rental if you’re not Hertz, Enterprise, or Avis

Main takeaway from the session centered around the independent operator’s ability to build deep relationships in their community and among their dealer network. Creative business arrangements that might facilitate a sale of a new vehicle in return for the opportunity to buy it back when retired from rental fleet can create flexibility that the majors might not have.

Conclusions

Not including time spent in the exhibitor trade show, I attended 13 hours of sessions over the three days of the International Car Rental Show. My perspective as an attendee at the ICRS is different from that as an operator. Not being consumed with the day-to-day operations of a rental car company, my focus is on where the industry is going and how ACCRO can help our members best prepare for that future. I saw many exhibitors at the ICRS trade show presenting solutions for today’s and tomorrow’s challenges. I also observed many operator attendees talking and learning from each other.

Q & A periods at the end of sessions were vibrant and the show attendees were more engaged with the content than I can ever remember. If you are on the fence about attending next year’s International Car Rental Show taking place April 16-18, 2023 at Paris Hotel and Casino, Las Vegas, I would strongly recommend you consider whether or not exposure to your peers and solutions for today’s challenges and tomorrow’s opportunities would be beneficial. With the current strong rental rate environment, many in the industry are experiencing operating profits outside of fleet management gains for the first time in a long time, maybe ever. While this situation lasts, it could be an opportunity to reinvest a portion of those profits into modernizing your rental management system and implementing a vehicle-based technology solution that returns increased revenue, vehicle efficiency, and preserves residual value while improving productivity with the same or fewer employees.

Craig Hirota is vice president of ACCRO, the Canadian car rental association.

Subscribe to Our Newsletter

More Rental Operations

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

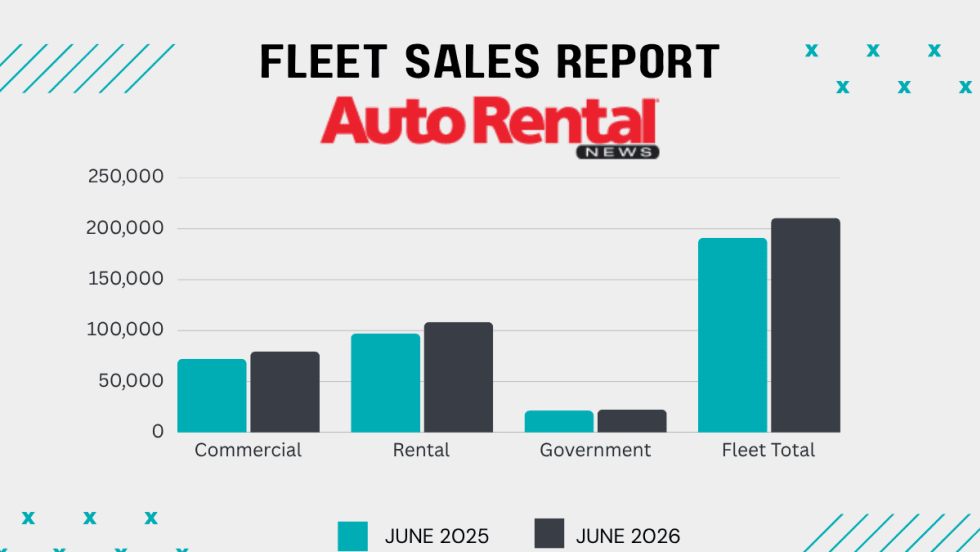

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →