Rent to Own: A New Way to Reach the Subprime Market

Auto By Rent, a Springfield, Mo.–based RTO operation, says its licensees can maintain a 20 percent net profit before taxes when the business is in full swing and can expect a reasonable minimum net profit of $200,000 a year.

Auctions, brokers, eBay, used car sales from the back of your lot. Is there a better way to dispose of your de-fleeted rental cars?

The “rent-to-own” concept has been around for years, but did you know that just about anything—including tires, wheels and even houses—can be set up for “rent to own?”

Why not do it with automobiles?

The rent-to-own sales idea caters to the subprime market, the same customers in the “buy-here-pay-here” used car sales market.

However, the “rent-to-own” customer completes the payment terms at twice the success rate of “buy here pay here,” says Wayne Lewis, CEO of Auto By Rent, a rent-to-own operation based in Springfield, Mo. Moreover, Lewis says net profit on an Auto By Rent location should be 20 percent after two years maturity, with very low overhead.

Auto By Rent has begun to offer rent-to-own franchise opportunities to take advantage of this healthy profit margin and growing customer segment.

Before getting into franchise specifics, it is important to understand what “rent to own” is—and what it is not.

Defining Rent to Own

Though both “rent to own” (RTO) and “buy here pay here” (BHPH) cater to the same subprime customer, the sales models are vastly different.

BHPH outlets can make good money in fees and interest; however, they must surrender the title to the high-risk buyer while the loan is sold to a subprime lender. For the BHPH customer, the upfront costs for tax, title and license can be difficult to swing, meaning the seller often has to get creative to put the deal together.

The RTO customer avoids upfront sales tax in most states and is taxed only on the payments. License fees are handled by the operation. Likewise, the RTO operation is taxed on rental receipts as opposed to gross profit booked as receivables. Taxes are paid only on actual payments received from the customer.

In the RTO model the car is not sold, it is rented. The title stays with the operation. If agreed rent payments are made the title will then pass to the renter. Auto By Rent’s average rental contract is two years, though terms can vary per customer.

Because the customer is not financing, there are no interest payments and no credit checks. The customer’s credit is not further deteriorated if they cannot complete the obligation on the rental agreement. However, the customer that walks away from the agreement has no rights to the vehicle.

Payments are made weekly, not monthly, which works better in the subprime arena, Lewis says. Ideal payments are $75-$100 per week. In the Auto By Rent program a missed payment does not incur added interest costs, just a $25 one-time late fee per late payment.

The cars that best fit this market are high mileage, mechanically sound cars bought at auction for $5,000–$6,000.

Cars are marked up about twice the wholesale price and the franchisee assesses the customer a non-refundable origination fee. The goal is to make more than 100 percent gross profit on the vehicle over the life of the rental.

In terms of car sales, a rent-to-own operation works best on its own lot, where higher priced cars available to good credit customers can be separated from the more affordable models in the price range of the subprime customer.

This avoids the touchy conversation regarding not being able to afford the car, says Roberts. “It alleviates the possibility of losing a customer who feels he is swallowing his pride.” [PAGEBREAK] The Auto By Rent Franchise

Wayne Lewis started out selling cars in 1995 as Premier Auto Outlet. He was so intrigued with struggling subprime customers who could not find a way to buy a car of any kind he decided to experiment with the rent-to-own concept. Auto By Rent was born in 2003. The company has grown into a four-location, profit-making, standalone business.

The company has five franchise agreements in place and expects three stores to open by the end of 2008, with another five expected to open in 2009. Opportunities are available now in 36 states with more coming in the next year.

The franchisee gets a full complement of training, expertise and materials to get the business up and running.

In addition to the logo identity and trademarked name, the company provides a rental software package, sales brochures and other printed collateral, as well as 20 payment devices and installation instructions. The company even provides ready-to-go television ads.

However, the real value is in the training, Roberts says, and that starts with the operating manual. “Everything our franchise knows and has already learned by our mistakes is in the manual,” says Roberts.

The manual explains how to arrange client accounts, qualify buyers and set up a Web page, as well as the best cars to buy for this market.

For those unfamiliar with buying at auto auctions, Lewis will personally take the franchisee to an auction to teach buying skills.

The Auto By Rent experts will help to get financing through either the licensee’s bank or the company’s, and then work with the bank to understand the operation’s true financing needs and a realistic loan payment plan.

The company will help develop a property to have the right look and feel for an Auto By Rent location. Locations with a sales lot for at least 25 cars, such as gas stations or old dealerships, work well.

Auto By Rent provides up to six weeks of training for two people and will send staff to help out on site for the opening week if needed.

A profitable Auto By Rent location should expect an average production of 15 vehicles per month while maintaining 200 total accounts, according to franchise materials. At least 25 cars should be available for rent. These numbers can be serviced by four or five employees.

According to the company’s Uniform Franchise Offering Circular, a licensee can maintain a 20 percent net profit before taxes when the business is in full swing and can expect a reasonable minimum net profit of $200,000 a year. [PAGEBREAK] Keeping Them Honest

Subprime customers are usually on a stressed cash budget. Experience shows that a certain percentage will do desperate things to keep the car, Roberts says. Auto By Rent has means to determine the worthiness of the customer as well as ways to keep them making payments.

Auto By Rent has created a proprietary “stability factor,” which measures a potential customer’s risk. Also, customers need to show they have valid car insurance before they take possession of the rental.

After the rental is approved, technology takes over to keep these customers honest.

The payment device is a legal electronic starter interrupt that requires a six-digit code to keep the car running. After payment is received, the driver keys the code into the device. The code keeps the car running for a week, with an additional three to seven days of wiggle room.

Roberts says over a five-year span the company’s four locations have only lost one car using the device. About 90 percent of the customers make their payments on time.

“The subprime client is our main customer, so we roll the carpet out for him,” Roberts says. “Their credit is strained but they have a steady job and are trying to turn their lives around.”

The payment device keeps the customer honest, and allows the rent-to-own company to treat its customers not like substandard borrowers but just like a prime customer.

Because of the established payment checks and balances, “We don’t treat them as a credit criminal; they don’t get the subprime treatment,” Lewis says. “Customers feel that they’re not being punished.”

Ultimately, 25–30 percent of rent-to-own customers complete the term, double the percentage of BHPH, Lewis says. Those who don’t take title don’t necessarily have their vehicles repossessed, according to Lewis. Some vehicles are totaled, while many customers voluntarily trade up to a more expensive vehicle or a standard loan.

While some bankers find it hard to understand the rent-to-own concept, they do get the concept of the payment device. They understand the higher percentage of success of franchises over an independent startup, Roberts says. And Auto By Rent has the numbers to support a positive return on investment in the first year, Roberts says.

The Growing Subprime Market

The subprime market is growing, evidenced by all the payday loan places, title loans storefronts and pawn shops. However, due to the delinquencies in subprime mortgages, banks are becoming reluctant to buy subprime loans from BHPH outlets.

If those loans dry up, credit-challenged buyers will be forced to look for alternative ways to acquire things like houses, tires and cars. This makes the rent-to-own concept more attractive, says Roberts.

Andy Batchelor owned a nine-location car rental company and four body shops the Springfield, Mo area. He now consults with rental car companies through the Small Business Association.

More Rental Operations

Car Rental Rates Forecast to Rise 3.6% in 2026 Before Easing in 2027

Car rental rates are projected to rise less than airfares and hotel rates in 2026, then become the only major travel category forecast to decline in 2027, according to projections from GBTA and ALTOUR.

Read More →

Avis Cuts Fleet as Summer Demand Trails Expectations

Avis Budget Group increased second-quarter earnings despite lower Americas revenue and softer-than-expected summer demand. The company also expanded Avis First and advanced its autonomous fleet operations with Waymo.

Read More →

Why Bookings Are Only the Start of the Rental Day

A reservation captures demand. The operating test is whether the business can keep the customer, vehicle, commercial terms, and next action aligned until the rental is closed.

Read More →

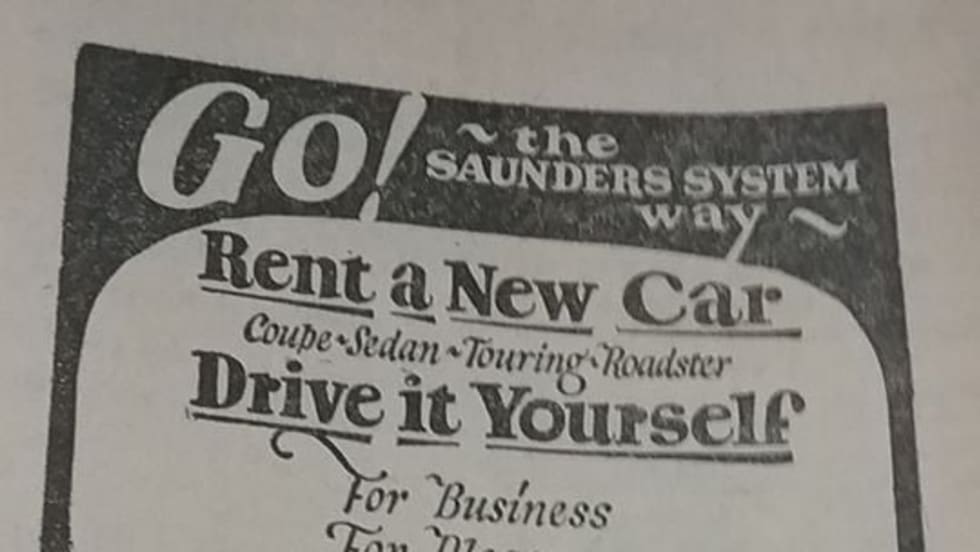

This Is the Oldest Car Rental Advertisement You’ll Ever See

This ad for Saunders Drive it Yourself, believed to be the first car rental company in the U.S., was found in an Omaha phone book from 1926.

Read More →

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

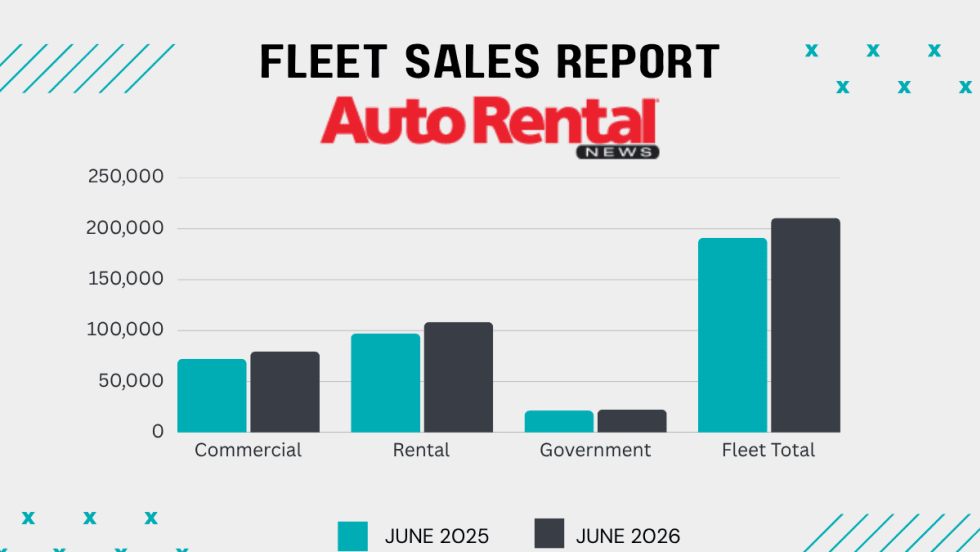

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →