COVID-19 Survey: Rates, Revenues, Optimism Rebound in Q3

The latest Auto Rental News coronavirus survey tells the story of an industry that was initially devastated by the pandemic but is in an encouraging — if slow and uneven — process of recovery.

Auto Rental News has tabulated the results of its third survey deployed to assess the impacts of the coronavirus pandemic. The survey was sent to independent and franchised (non-corporate) U.S. car rental operators and garnered 87 responses. It was conducted beginning Oct. 9 and tabulated on Nov. 10.

The results of this survey, taken with the previous two (tabulated April 14 and May 19), tell the story of an industry that was initially devasted by the pandemic but is in an encouraging — if slow and uneven — process of recovery.

The respondents in this survey were 38% franchise and 51% independent (along with 8% dealership and 3% identifying as other). A plurality (30%) had fleet sizes of 100 to 499 units, with 23% from 50 to 99 units and 17% reporting greater than 500 units.

In terms of customer base, respondents were divided between 40% off-airport/neighborhood and 33% serving airport customers, with the remainder serving leisure destinations, dealerships, and exotic rental customers. The average full-time employee count was 19 and part-time was seven.

Staff Stabilization

As of April 14, the pandemic’s effect was clear. By the time the first survey was tabulated (April 14), 83% of respondents said they had reduced staff hours. Of that group, 57% reported reducing hours by 51% to 100%, with 14% of respondents reducing staff 100%, indicating they closed their businesses, at least temporarily.

Note that in that first survey, 15% of respondents said that their government had forced them to shut down their business as a part of COVID-19 safety measures. By the second survey, a 8% of respondents indicated a 100% reduction in hours.

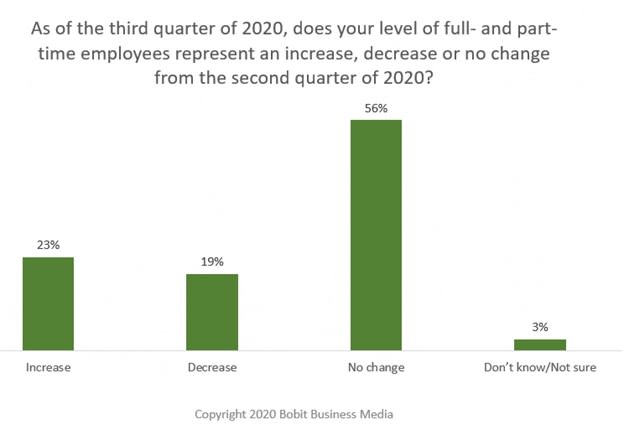

The final survey (tabulated Nov. 10) reveals a stabilization in staffing. In that survey, a majority of respondents reported that their staffing levels had at least stayed the same from the second into the third quarters, with more respondents increasing their staffing (23%) compared decreasing.

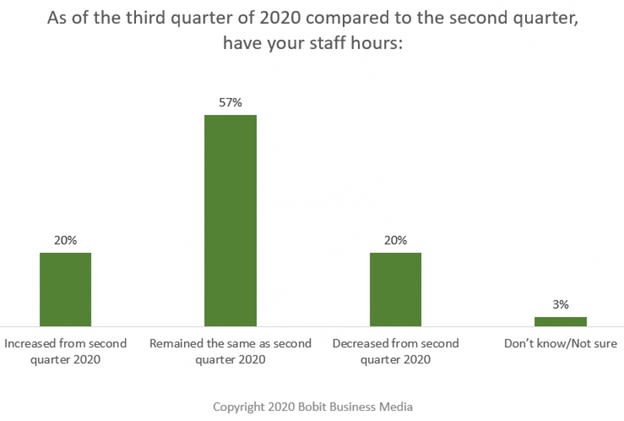

Mirroring the response on employee count, a majority of respondents said that they kept their staff hours the same from the second to the third quarters, while an even percentage of respondents either increased hours (20%) or decreased hours (20%). The key takeaway – operators are meeting the increase in third-quarter business with static staffing levels and hours.

Fleet Gains

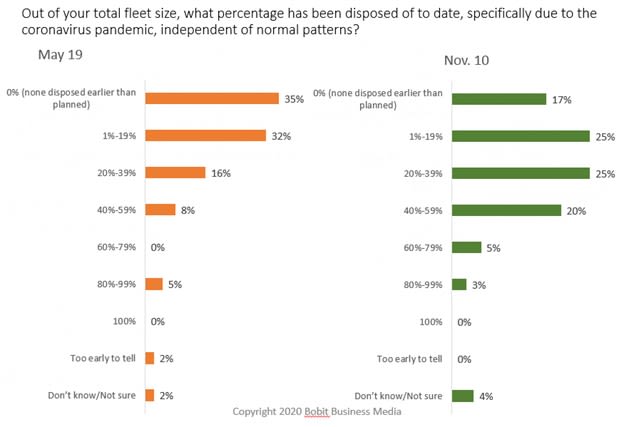

As business almost ground to a halt by mid-April, the great majority of respondents couldn’t shed fleet because the wholesale market’s infrastructure ground to a halt too. By the second quarter, operators were still faced with business losses, but the lack of new and used supply and constriction of auction lanes generated red hot prices. Car rental consignors took advantage.

By the third quarter — usually the busiest for car rental — operators were instead selling fleet. Note that 37% to 48% of respondents acquire all of their vehicles as risk units as opposed to through manufacturers’ repurchase programs.

Revenue Recovery

In the first survey, half of respondents said their first quarter revenue was down by 51% to 100%. (Note that the pandemic hit in the second half of the quarter.)

By the second survey, the revenue drop had accelerated, with 76% of respondents saying revenue had decreased 51% to 100%. The third quarter revealed the green shoots of recovery — compared to the third quarter of 2019, 45% said their revenue decreased to a lesser extent (0% to 50%).

Remarkably, 14% said revenue hadn’t declined in the period, while 14% said revenue had actually increased.

Pricing Shifts

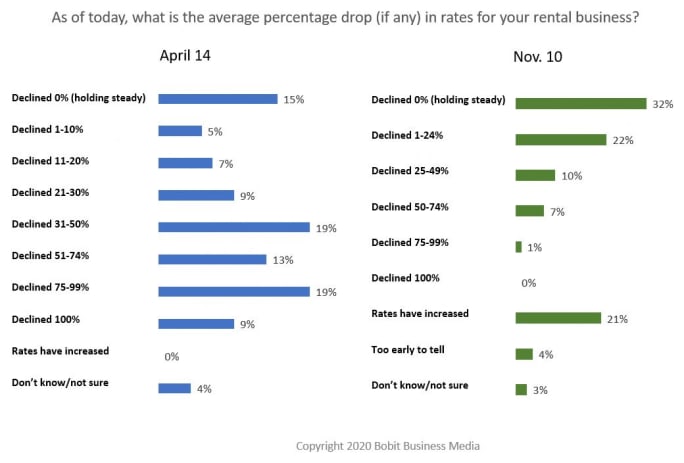

Car rental pricing shows a more dramatic recovery from the first to third surveys, for the specific reason that operators were able to shed fleet, allowing demand to outpace supply by the third quarter.

Year Ahead

The final questions in the third survey speak to the optimism (or lack thereof) of the car rental industry moving forward. While encouraging to see that the most selected response states that the respondent is on the road to recovery, it is not a majority, and 32% say “it’s too early to tell.”

And while respondents believe their company in particular will recover, it’s an almost even split between those that believe the industry in general will recover and those that won’t. (Note that these questions were not asked in the first two surveys.)

Similar to the previous question, more respondents identified as optimistic about the future than the other choices, and only 6% identified as pessimistic. However, the other two choices taken together reveal that 59% of respondents are still uncertain and are taking a “wait-and-see” approach.

More Rental Operations

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

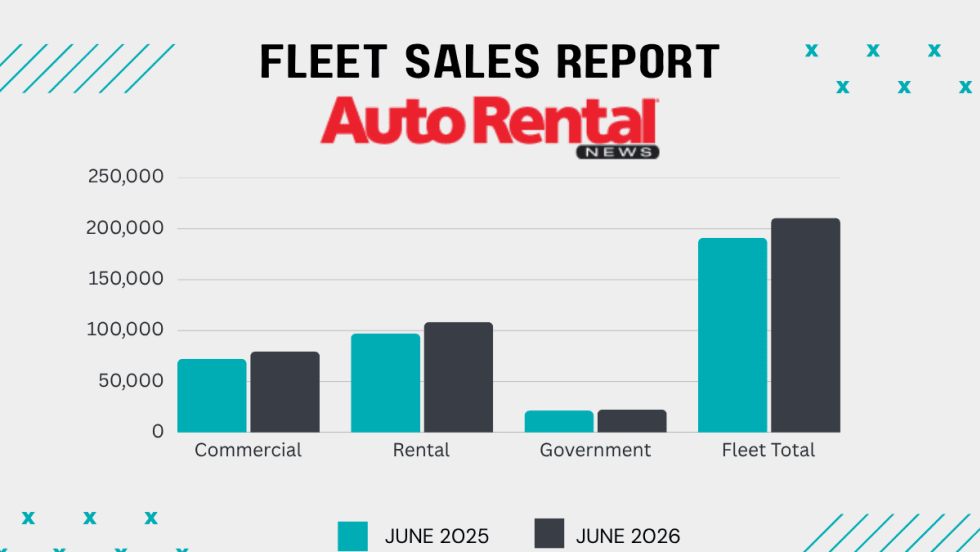

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →