WeYield Data: European Car Rental Struggles to Emerge from Covid Lockdowns

In its latest market trends report for Europe, WeYield found that utilization is down 18% in July year over year and that cancellations have increased 10 times over than last year. Trends are better for August.

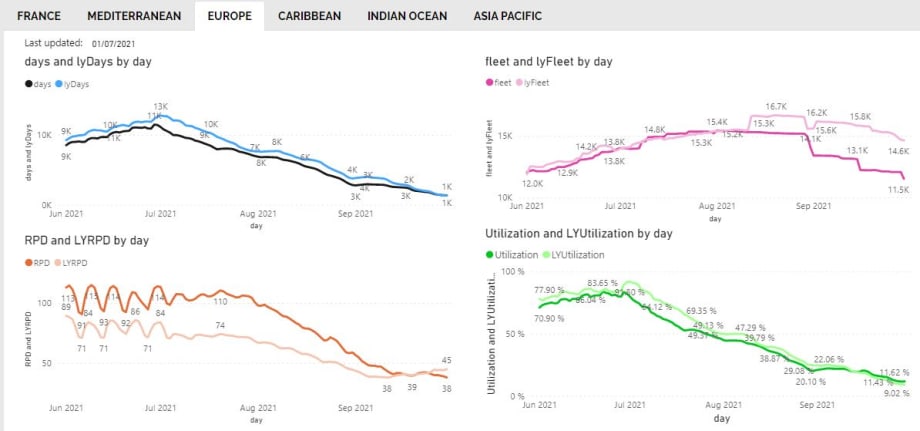

WeYield’s latest market trends report of Europe shows that key trends in rental days, fleet, and utilization are still tracking below last year (LY) during the pandemic, while revenue per day (RPD) is a bright spot.

Photo: WeYield

Who wouldn’t like to compare his own rental indicators to know if he/she is performing better or worse than the market?

As a revenue manager expert, it has always been crucial for me to elevate the knowledge of my situation and integrate it in a wider market scope.

In revenue management, it is key to get this helicopter view about the general trends. Analyzing your data is key but knowing how the entire car rental market is behaving, is interesting too.

Since the beginning of Covid-19 in Winter-Spring 2020, WeYield has been broadcasting twice a month a market trends report. WeYield aggregates all client data from around the world and displays them in a consolidated and anonymized format by geographical zone.

As June 2021 just finished, here are the indicators from a European standpoint:

Overall demand shrunk by -10% in days due to less reservations -13% partially offset by a longer duration.

Fleet was stable vs last year but at a level around -20% vs 2019.

The good news was on RPD (revenue per day), with a strong increase of +45% vs last year at 106€ vs 73% on June 20.

But due to a lower utilization (77%) the profit impact was negative with a revcar of 55€ compared to 66€ in 2020. Revcar equals revenue per available car (utilization ratio x revenue per day)

Peak Summer Trends

Regarding the super-peak summer (July and August), trends are pretty similar to June for the car rental sector in Europe:

Demand stands at -10% for July and -20% for August 2021 vs last year at the same time of reservation (equivalent reservation date) to compare a like-for-like situation.

Utilization is a bit better currently for August with only -10% (40% utilization globally) while July is at -18% (59% utilization globally) thanks to a stable fleet vs 2020.

The level of cancelations is extremely high, about 10 times more than last year.

The good news is that the RPD continues to increase at +40% for the Summer. Revenue managers are taking advantage of the constraints on the fleet and the appetite to travel of the people who can go abroad.

For most European citizens, an increase in household savings and a strong desire to enjoy their summer escapes after two lockdowns in autumn 2020 and spring 2021 — without winter vacations — are supporting overall strong demand. Clearly, the travel restrictions in the United Kingdom, number one source country for European destinations, jeopardize July trends.

“Clearly the Prime Minister wants the British to stay in the UK and spend their money locally,” says a Cypriot car rental operator. All operators accept that Boris Johnson will release the travel bans and reduce the cost of PCR tests.

About the author: Emmanuel Scuto is CEO and founder of WeYield, providers of smart data-driven decisions for ambitious car rental companies.

More Rental Operations

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →