How to Reduce the Risk of Auto Rental Chargebacks

Suresh Dakshina, president of Chargeback Gurus, shares insight on why auto rental companies can be susceptible to chargebacks and tips to lessen the risk.

Photo via Roxanne Tamayo/Flickr

Photo via Roxanne Tamayo/Flickr

Five years ago, only about 20% to 30% of credit card fraud claims were "friendly fraud," where the cardholder made the transaction but later disputed it.

“Usually, they do it because they are unhappy with the company — either because of the way the company did business or something about the product or service sold,” said Suresh Dakshina, president of Chargeback Gurus. “Sometimes it's an outright attempt to get something for nothing.”

Auto rental companies are especially vulnerable to chargebacks. Customers may get upset at additional charges for fuel, tire damage, one-way drop-off, or having a young driver. A sudden change in plans, which by itself can put anyone in a foul mood, may mean getting hit with a cancellation charge, says Dakshina.

Customers may also find a rental company’s written policies confusing. They may accidentally sign for insurance or damage waivers when completing forms at the counter, even if they verbally agreed to something else.

With luxury rentals, the value of the vehicle can make those unexpected charges even higher. Luxury cars are also a tempting target for true fraudsters.

“A few years ago, a woman with stolen credit card numbers and stolen drivers’ licenses engineered the theft of 42 rental vehicles from a major rental car company in Orange County, Calif.,” said Dakshina. “Many of the vehicles were higher-end models such as a Mercedes-Benz E-350.”

Visa and MasterCard are well aware of the percentage of auto rental transactions that result in chargebacks, and they have tagged the car rental industry as being among the highest-risk merchants they deal with.

Reduce Processing Pain

According to UniBul Merchant Services, there is a direct correlation between customer disputes and chargebacks. Fewer disputes mean fewer chargebacks. UniBul recommends putting customer satisfaction at the center of credit card processing procedures, including getting new authorization every time that the customer requests to extend the rental period.

If the authorization is declined, UniBul recommends settling only the amount that was originally authorized and asking the customer for an alternative payment method on the remainder.

Then there's the 15% rule. If the final bill is at least 15% larger than the previously authorized transaction amount, rental companies will need an additional authorization for the difference.

Risk Reduction

Remember, the fewer unpleasant surprises for the customer, the less likely they are to initiate a chargeback.

Communication and transparency are vital. When customers are clear from the start about potential extra charges, they are less likely to get upset when they see the final bill, and consequently, less likely to file a dispute, according to Dakshina.

Email the contract terms and other information to customers so they know what to expect. Also make sure customers have your website address and telephone number. If they have any kind of issue, you want to make it easier for them to contact you than to dial the number on the back of their credit card, says Dakshina.

Make sure you are giving vehicles a thorough inspection before and after each rental. A determined scammer will try tricks if they don't think you are paying attention.

“An example is where a customer complained that the Mercedes-Benz AMG he had rented was performing like a Toyota Camry,” said Dakshina. “When a mechanic popped the hood of the car to check, he saw that a previous customer had stolen the high performance engine and swapped it for a cheaper one.”

Red Flags

Knight Insurance Group has identified a few red flags to watch for that can help avoid getting swindled. They include paying attention to someone with a local address but an out-of-state license or someone using a foreign driver's license without presenting a passport. Also, give extra scrutiny to one-day rentals, offers of cash payment, and walk-ins who don't own a vehicle.

If you suspect a customer is trying to take unfair advantage of the system, check out what he or she is saying on social media. Some people will boast online about their behavior.

According to Dakshina, here’s an example of a social media post: “I have probably done three or four credit card chargebacks against various rental car companies. If I have a charge, I don’t even bother calling them. I go immediately to my credit card company. I always win.”

Don't hesitate to keep a "do not rent" list of blacklisted customers who have won credit card disputes.

With so much at stake, it's important to run a comprehensive risk and vulnerability assessment to see where your business could be susceptible to fraud risk, according to Dakshina. If you don't have the extra resources, consider outsourcing fraud prevention to reliable specialists.

More Rental Operations

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

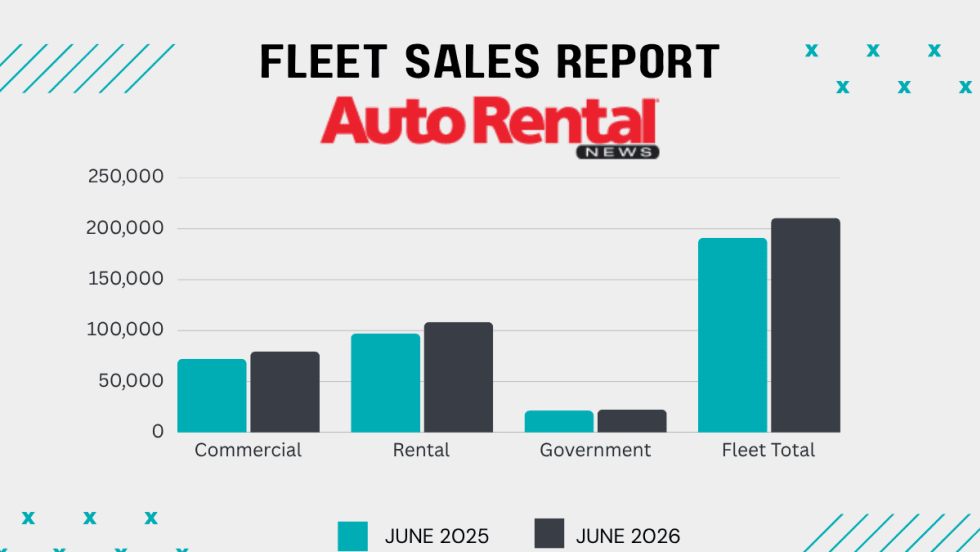

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →