Carsharing: State of the Market and Growth Potential

The carsharing market has grown from a largely subsidized, university research-driven experiment into a full-fledged for-profit enterprise, owned primarily by traditional car rental companies and auto manufacturers.

The largest carshare company, Zipcar, operates a traditional “station-based” network, though the company is beta testing a one-way program in Boston.

Photo courtesy of Zipcar.

Though aspects of carsharing have existed since 1948 in Switzerland, it was only in the last 15 years that the concept has evolved into a mobility solution in the United States.

In that time, the carsharing market has grown from a largely subsidized, university research-driven experiment into a full-fledged for-profit enterprise, owned primarily by traditional car rental companies and auto manufacturers. Today, Zipcar (owned by Avis Budget Group), car2go (owned by Daimler), Enterprise CarShare and Hertz 24/7 control about 95% of the carsharing market in the U.S.

Compared to car rental, total fleet size and revenues for carsharing remain relatively small. The “Fall 2014 Carsharing Outlook,” produced by the Transportation Sustainability Research Center at the University of California, Berkeley, reports 19,115 carsharing cars in the U.S., shared by about 996,000 members. Total annual revenue for carsharing in the U.S. is about $400 million, compared to the $24 billion in revenue for the traditional car rental market.

Those carshare numbers have roughly doubled in five or six years, demonstrating steady growth but not an explosion. Yet technology, new transportation models, shifting demographics and changing attitudes on mobility present new opportunities. Is carsharing poised to take advantage?

Driving Market Growth

As carsharing in the U.S. is essentially consolidated under those four market leaders, they will inevitably be the drivers of much of that growth.

Market watchers see one-way — or point-to-point carsharing — as a growth accelerator. Pioneered by car2go, the second largest carsharing company in the world, point-to-point carsharing allows users to pick up and drop off cars in any legal parking space within the company’s coverage area.

“Point-to-point can quickly attract three to four times the number of members of a traditional round-trip service,” says Dave Brook, managing partner of Team Red U.S., international transportation consultants. “But they cost a lot of money to launch since you need several hundred vehicles to start with.”

The largest carshare company, Zipcar, operates a traditional “station-based” network, though the company is beta testing a one-way program in Boston. Zipcar One>Way isn’t free-floating; rather, it allows the user to drop the vehicle off in any of Zipcar’s “pods” (garages, generally), provided the drop-off pod is reserved by the user in advance.

“There are a number of local governments amending parking policies to allow for free-floating, one-way carsharing,” says Dr. Susan Shaheen, co-director of the Berkeley Transportation Sustainability Research Center, including Boston and Seattle.

Pioneered by car2go, the second largest carsharing company in the world, point-to-point carsharing allows users to pick up and drop off cars in any legal parking space within the company’s coverage area.

Photo by Chris Brown.

However, “Not all cities can accommodate a free-floating system, especially if parking is limited or difficult,” Brook says.

Enterprise Holdings started its carsharing program as WeCar in 2008, focusing initially on universities. Enterprise rebranded as Enterprise CarShare in 2013. Entering 30 new North American markets last year, Enterprise CarShare has grown organically and through acquisition of independent carsharing companies such as IGO in Chicago, AutoShare Carsharing Network in Toronto and PhillyCarShare.

Ryan Johnson, assistant vice president in charge of Enterprise’s carsharing and vanpool operations, points out that carsharing is the technological evolution of Enterprise’s growth in the neighborhood market. “Carsharing takes that to the next level,” he says.

Hertz’s carshare service — started as Connect by Hertz in 2008, rebranded as Hertz on Demand in 2011 and then as Hertz 24/7 in 2013 — operates in 18 states and nine countries.

While it has been quiet of late regarding announcements of new fleet and locations, Hertz is piloting video kiosks in conjunction with its carsharing service in New York City. The kiosks allow customers to perform fully-automated rental transactions and also interact directly with live customer service agents.

BMW’s DriveNow carsharing program, in conjunction with Sixt, operates 2,400 vehicles in Germany, Austria and the United Kingdom. While DriveNow’s U.S. footprint is small — 70 electric BMW ActiveE models in San Francisco — Seattle is scheduled to come online this year using the point-to-point model.

Emerging Carsharing Companies

Does the market dominance of four companies allow room for the growth of independents?

“Prior to the acquisition of Zipcar by Avis Budget Group, there was a significant amount of growth in the [carshare] industry,” says Julian Espiritu, managing director of Abrams Carsharing Advisors. “Since car rental companies have gotten into carsharing, it’s been hard in North America for independents to launch a carshare operation.”

Two of those independents have connections to non-major auto rental companies. Carpingo, owned by AllCar Rent-A-Car, serves New York’s boroughs and competes directly with major carshare companies. Student CarShare serves 16 universities in the province of Ontario. The company has partnered with Discount Car and Truck Rentals on fleet in exchange for a percentage of profits.

Espiritu points to much greater opportunity for traditional carsharing in overseas markets, particularly Latin America and developing countries, where only a handful of carsharing companies operate. Car2go recently announced an initiative in China.

A handful of early stakeholders, such as Communauto in Quebec province and City CarShare in San Francisco, a nonprofit, have managed to stave off consolidation. Since 1994, 80 carsharing programs have been deployed in the Americas; 45 are operational and 35 defunct, according to the Fall 2014 Carsharing Outlook.

Other high-profile survivors, along with new entrants, have deep pockets.

In the peer-to-peer space, growth has come in fits and starts for Getaround and RelayRides, yet both have recently secured eight-figure funding. RelayRides has moved away from hourly rentals and now operates as a traditional daily rental company using personally-owned vehicles. Legislation in California, Oregon and Washington mandates that insurance carriers can’t drop their coverage of personal use policyholders who rent their cars.

BMW’s DriveNow carsharing program, in conjunction with Sixt, operates 2,400 vehicles in Germany, Austria and the United Kingdom.

Photo courtesy of DriveNow.

FlightCar has carved out a peer-to-peer niche at 11 major airports. FlightCar members drop their cars off in designated parking and get paid to allow others to use their vehicles while they travel.

BlueIndy, an offshoot of Paris-based conglomerate Bolloré Group, is expected to launch soon in Indianapolis. The service, in conjunction with Indianapolis Power & Light, features plug-in electric cars and public charging stations. Bolloré also oversees AutoLib, Paris’ largest carsharing network. AutoLib exclusively runs the Bolloré manufactured all-electric Bluecar.

Electric vehicle (EV) carsharing is a favorite of city governments for environmental reasons, Shaheen says. Most carshare trips fall within an EV’s limited range, operators can get federal tax credits and subsidies for implementation, and auto manufacturers are keen to use carsharing as a way to drive EV adoption.

Shift, a soon-to-open carshare network in Las Vegas that rents only electric vehicles, will also include a valet service for pickups and drop-offs. Zappos CEO Tony Hsieh invested $10 million in this startup.

New Markets

Carsharing has traditionally found its niche in urban environments, especially those with strong public transportation networks, as well as universities. While these areas continue to grow, new ones are being exploited.

In various cities, new housing mega-complexes — such as Brooklyn’s high-profile Greenpoint Landing — are adding carsharing as an amenity for residents.

Areas not traditionally thought of as ideal for carsharing are now being considered. “Our neighborhood is the worst for public transportation, but we have seven Zipcars,” says Gil Cygler, owner of Carpingo and AllCar Rent-A-Car. “I would’ve never considered my neighborhood [for carsharing] five years ago.”

Tony Simopoulos, CEO of Metavera, a carsharing technology provider, says that independent entrants would have a hard time penetrating big cities such as New York, Philadelphia, Chicago or Washington D.C.; however, underpenetrated second-tier cities have potential for new blood.

Michael Lende, founder and CEO of Student CarShare, thinks there is still room for carsharing in the university markets. Lende says his surveys reveal that as many as 90% of new students and their parents don’t know that carsharing exists.

In various cities, new housing mega-complexes — such as Brooklyn’s high-profile Greenpoint Landing — are adding carsharing as an amenity for residents.

Photo courtesy of Communauto.

Each of the major carsharing programs runs a business program. For businesses, moving from an owned fleet to a shared fleet allows them to trim fleet expense. For those same reasons, municipalities such as Washington, D.C., Sacramento, Calif., and Vancouver have implemented carsharing programs. Several fleet management companies are considering partnering with carsharing companies.

Ride Sourcing and Other Factors

Local governments with friendly public policies would promote carsharing growth — yet government entities could just as easily curtail carsharing parking space allocation, which would essentially shut new entrants from a market.

Public parking spaces are increasingly viewed as battlegrounds. The patchwork quilts of parking regulations are a constant challenge for carshare operators. “It took us almost three years to get our first permit,” says Diego Solórzano, founder of Carrot, the first and only carsharing company in Mexico. “Parking in Mexico City is controlled by 10 different agencies, so each of those agencies must approve a project.”

Fleet is expensive for newcomers without traditional fleet funding lines, and insurance carriers have tightened their reins on car rentals in general. “If you’re going to start a carsharing company, you really need at minimum 25 to 30 vehicles,” Espiritu says.

Each of the major carsharing programs runs a business program. For businesses, moving from an owned fleet to a shared fleet allows them to trim fleet expense. For those same reasons, municipalities such as Washington, D.C., Sacramento, Calif., and Vancouver have implemented carsharing programs.

Photo courtesy of City CarShare.

“For me, the big carsharing news of 2014 didn’t happen in the carsharing industry at all — it was the incredible growth of Uber, Lyft and Sidecar, demonstrating an unserved demand for taxi-like services far greater than any could have even imagined,” Brook says.

Called “ridesharing,” or more accurately, “ride sourcing” or “ride hailing,” these transportation network companies (TNCs) have exploded worldwide in the past few years. Uber and Lyft’s valuations now top Avis Budget Group’s and Hertz’s combined.

Is ride sourcing helping or hurting carsharing’s penetration?

In one sense, ride sourcing and other shared-use modes — including bikesharing services — are potential competition for the same short-distance trips that carsharing specializes in. “One-way services and ride sourcing have increased competition for point-to-point mobility,” Shaheen says.

Ride sourcing and carsharing compete in cities with limited taxi services. Ride-sourced trips replicate taxi trips, so they’re usually one way, with similar usage patterns to point-to-point carsharing services.

From Brook’s point of view, “Anything that gets people to take a trip in someone else’s vehicle will contribute to the long-term reduction in car ownership, which makes carsharing more attractive,” he says. “Whether we’re at a ‘tipping point’ in urban mobility patterns, it’s too early to tell.”

Convergence of Carshing

“We have been seeing the convergence of the carsharing and rental car markets for some time,” Shaheen says. She points to cashier-less and cashless transactions and “virtual storefronts” from which renters can choose a specific car — with rental lengths from hourly to weekly — while trips are reserved or spontaneous, one-way or round trip.

The convergence is logical, says Michael Youssef, CEO and president of Rent Centric, a provider of car rental and carsharing software and hardware.

“The early adopters in the carshare market didn’t initially have experience in the car rental market, so when they began to formulate their solutions, they did so on a blank paper,” he says. “But when they started realizing that carsharing is car rental but using an ‘on-demand’ method, that business model has to inherently include all the business processes that car rental is used to,” especially fleet buying, selling, maintenance and utilization.

Johnson sees the market maturing in two ways: “The core carshare customer will grow because we’re providing a bigger and better network, with better technology, and this traditional niche will become more mainstream,” he says. “At the same time, we’re putting carshare technology into all phases of car rental, so that picking up a car in an unattended way is not just for someone who has made the predisposed decision to become a carshare member — anyone can access the car.”

This foretells a new trend altogether — on-demand, or self-service car rental — that uses carsharing technology to automate the traditional rental process. “With no rental counter and attendant, unattended rental allows a rental company to operate at much lower margins,” says Nittin Duggal, vice president of JustShareIt, a carsharing technology provider.

At least initially, the technology may only be used to automate parts of a rental, such as expediting paperwork or qualifying the customer. “There’s a lot of opportunity for those things to eventually meld into the daily rental process,” Johnson says.

Studies reveal that the millennial generation is eschewing car ownership in this new era of social media, and auto manufacturers have taken note.

Photo courtesy of Carrot.

Johnson adds that proper customer orientation is essential to move the new model forward. While carsharing members understand the group responsibility to maintain the unattended car for the next renter, non-members may not. “You’ve got a combination of the early adopters and new technologies,” he says. “Those have to grow and mature in a very conscientious manner to get to this future.”

Changing Attitudes, Demographics

From hotel rooms and home grocery delivery to downloading movies to a tablet, consumers expect to be able to transact anything at their fingertips, on the fly. “Consumers are looking for more and more services that meet their on-demand needs using a mobile device,” Duggal says. “With a couple of taps on your mobile phone, you should be able to conduct anything you want.”

On-demand car rental is an extension of this trend.

Other external factors would seem to promote the expansion of the on-demand model: The World Health Organization estimates that 70% of the global population will live in cities and towns by 2050, up from just 50% today. This move back to cities is exacerbating already alarming congestion levels.

Studies reveal that the millennial generation is eschewing car ownership in this new era of social media, and auto manufacturers have taken note. Audi is piloting a program in Stockholm that allows four people to share an Audi for up to two years. In Germany, Ford researchers are testing a smartphone app that lets commuters order shuttle transportation for trips around town. Automakers are increasingly seeing their roles as providing mobility rather than just selling vehicles.

The need for mobility will always exist, though it is continually morphing into new, more efficient realms. The automobile is not going away, but the idea of sharing them is gaining more ground.

More Rental Operations

The Desk Upsell Is Costing Operators More Than it Earns

Counter upsells generate revenue, but they can also slow transactions, erode trust, and cost repeat business. Fully inclusive pricing may offer operators a better path to long-term value.

Read More →

U-Save Expands Indian Ocean Presence with New Master Franchise for Mauritius

The franchise has been acquired by Mauritian travel entrepreneur Umarfarooq Omarjee, an established figure in the island's tourism and mobility sector.

Read More →

Global Carsharing Fleet Projected to Reach 768,000 Vehicles By 2030

A new Berg Insight forecast outlines several business models driving the projected growth in public carsharing worldwide through 2029.

Read More →

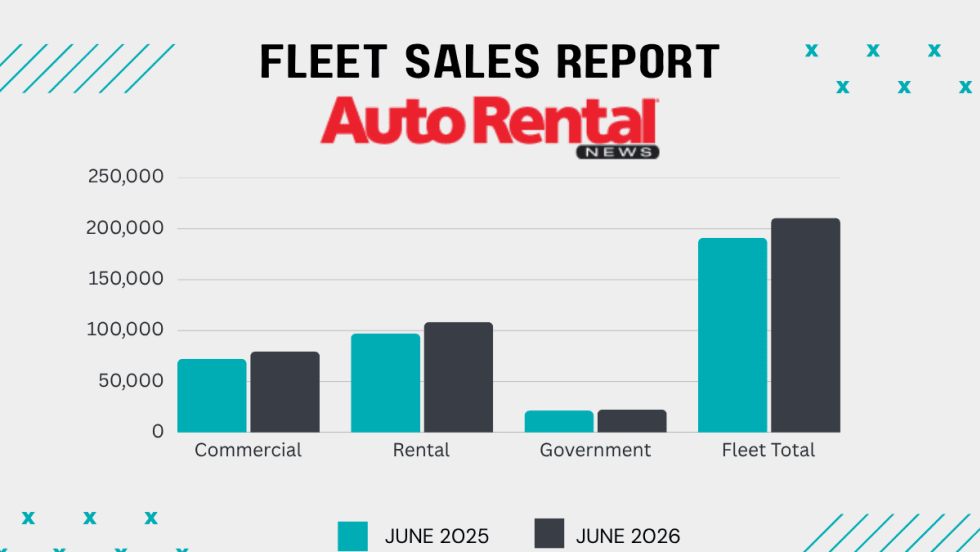

Rental Car Fleet Sales Show Mid-Year Strength

June gains ensured rental fleets closed out the first half of 2026 in positive territory.

Read More →

Surprice Mobility Opens Corporate Rental Station at Milan Malpensa Airport

The Milan opening is part of Surprice Mobility's broader strategy to expand its corporate operations while increasing the use of technology across its network.

Read More →

Brazilian Executive MBA Targets Growing Domestic Rental Car Industry

Rental car companies face a unique combination of challenges that are rarely addressed in traditional programs.

Read More →

Green Motion Expands Into Japan With Master Franchise Agreement

Japan's tourism industry, business travel market, and demand for vehicle rental services are reasons the country represents an important market for the company.

Read More →

ACRA Carrying Fuller Industry Load As AI and EVs Lurk In Future

The leading car rental professional business group details an active legislative, regulatory, and macro-trends agenda affecting car rental operators.

Read More →

World Cup Travel Data Shows Longer Car Rentals and More One-Ways

A recent analysis of FIFA bookings found varied demand patterns that influenced rental car pricing.

Read More →

A Leveling Force: AI Morphs Into A Rental Car Profit-Seeker

Revenue managers can’t match the emerging AI tools gobbling lots of data that could counter the competitive race to the rate bottom.

Read More →